We will have more clarity from the management at the AGM later this week. The merger valuation is a complicated exercise in terms of valuation, tax impact, NCLT, BSE and NSE approval etc. so it will take about a year. The terms will come in due course but the management. I don’t expect them to be unreasonable to Minority shareholders as I always say that the majority shareholder (i.e. Oaktree) wouldn’t want to ruin its reputation over a $10 mn transaction.

The interesting thing is that they don’t want to wait and plan to use the cash (via an inter-co loan) to develop offshore assets in Antelopus which would have been concerning if the merger wasn’t on the cards.

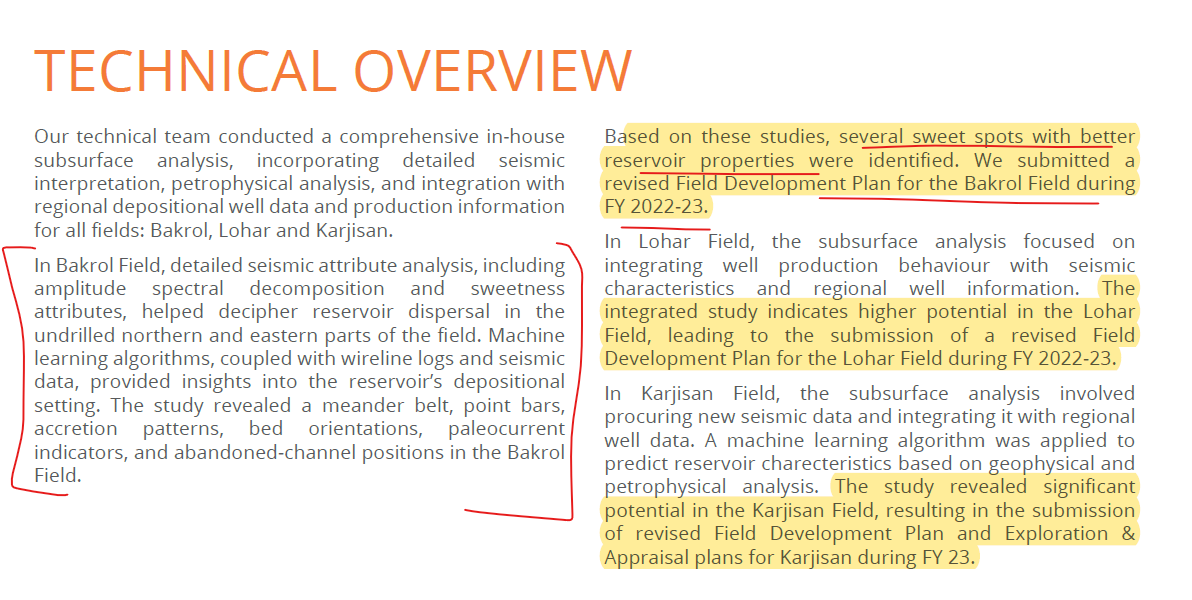

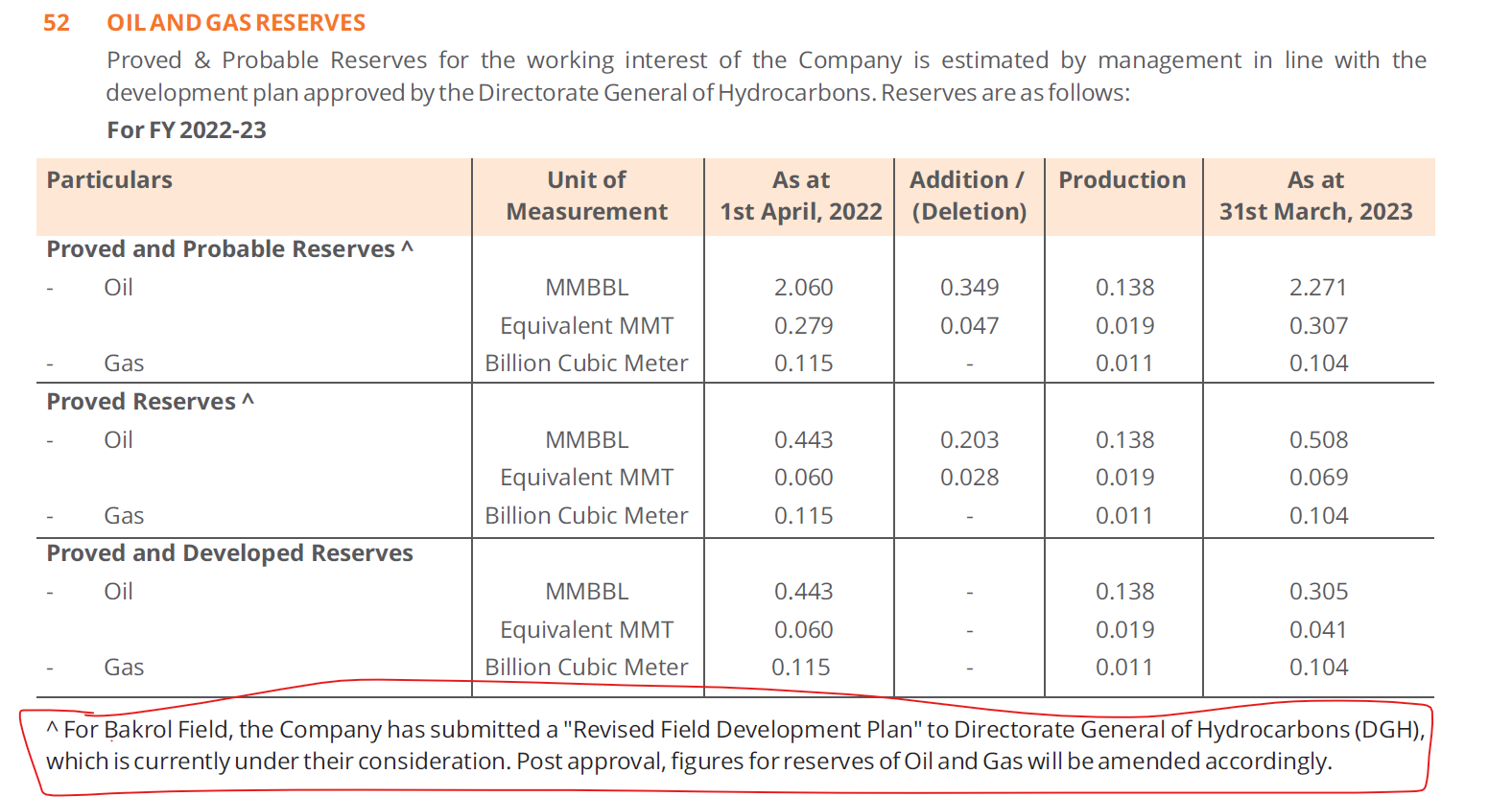

As an aside, I don’t think anyone noticed a particular disclosure in their current annual report under Technical Overview section followed by Note 52 where they disclose the oil and gas reserves. My reading is that they have found a higher reserve than expected. Hopefully, management clarifies during the AGM. Lots of optionality still in the asset. ![]()

Disclosure: invested and biased.

| Subscribe To Our Free Newsletter |