Shivalik Bimetals AGM Questions Sep 2023

Thanks to Collated questions from @spatel @sahil_vi @Dev_S @Donald

Those attending the AGM, let’s try and get all these answers from Management. Hoping the standards set in AGM 2022 will be upheld, and looking forward to another great interaction today.

- Competition/Customers – ambiguity

In the Mumbai Analyst meet, we were informed that

-

Shivalik defined its addressable Market as EBW Automotive Shunts for EV BMS [non EV BMS shunts % is as low as 5% already]. Can you please elaborate on that/confirm for everyone’s understanding.

-

Shivalik saw itself as the 4th or 5th biggest player globally in EBW Automotive Shunts after Vishay, Hella, Continental. Also that Isabellen Huette was NOT a competitor [within that segment], as they are primarily in Shunt Resistors. Can you please again elaborate on the Competitive situation and inform us on specific competition players that we as shareholders could also track – to understand the Market/Industry/Supply Chain/Inventory situation much better.

[IsHu supplies to Merc] -

Need some clarification here. We understand that both Hella and Continental are Tier1 BMS Suppliers to OEMs and both are Shivalik Customers (NOT competitors). Who are the other big Tier1 BMS suppliers to OEMs – Marquardt, Bosch, and Rohm?

-

If that is correct, then after Vishay who are the other Top EBW Shunts suppliers/Tier2 suppliers, and thus effective competitors for Shivalik.

- Global Markets 2022 vs 2023 (Total EV 13.8 Mn in 2022) and Shivalik Positioning

ngths- China accounted for 60% of all new EV registrations in 2023. Now? Is this an addressable market for Shivalik? Some addressal must be happening through Vishay? Is it like 10% ?

-

EU accounted for the next big chunk of 25% of global EV Sales. Early 2023 EV Sales growth of 30%? Has this remain unchanged? Fit for 55 package impetus? Shivalik business model/partners for EU Market?

-

US accounts for 10%? Cumulative post-IRA(Inflation Reduction Act) investments of USD 52 billion in North American EV supply chains, of which 50% is for battery manufacturing, and about 20% each for battery components and EV manufacturing? New Plants will be coming online in 2024. Is it a fair assessment that Shivalik is very well placed here strategically because of Vishay relationship/New capex in New Mexico

- Domestic Customers and Market Update

- Proportion of EBW Shunts sales to 4W/2W and 3W domestically

- Update on Mahindra XUV EV platform (co-design) – where are we, what is the scale visibility we have here?

- Tata Platforms -any co-designs or all built to customer specs? Visibility?

- 2W – how do we see this market scaling? What kind of timeframes are we talking about?

- Inventory/Destocking/Lead Times

-A year back Competition supply lead time ~50 weeks; Shivalik <20 weeks.

Has anything changed here? Why, or why not? Please elaborate

-We have seen volumes tapering off progressively quarter on quarter on Shunt strips?

- Acquisition Prospects/Fund Raising Needs

Shunt and Disconnect Relay both have an important role in smart-meter. Are we seeing integrated Relay-with-Shunt gaining traction in the market? If yes, is Shivalik exploring an option to acquire, build or partner with Disconnect Relay product co and enhance it with its own shunts? Something like Johnson Electric ZRP. Basically, to increase our wallet share in the real boom of smart-meter.

Source: https://www.youtube.com/watch?v=7j_QQAXWmIA

- Market Outlook

China and the EU are seeing a jolting drop in EV sales in 2023 (from EV touching 50% market share to now 15-25%). Consumer enthusiasm for EV is dampened as subsidies are reduced or set to disappear. The road ahead for the EV portion of our shunt business segment looks bumpy just in the near future or a bit longer?

Automakers across the globe have announced huge investments in EV and a relatively rapid transition to an all-electric fleet. Could you throw light on our cumulative Design-ins or Design-wins that could result in sizable sales in years to come?

How does the Opportunity Pipeline look today compared to a year ago? For the Shunt and Bi-metal/tripmetal business segment.

“The third and fourth quarter for us should be much stronger than what it has been in this quarter” was said in Q1FY24 concall. Any new encouraging/ discouraging development or the statement still holds true? Is this statement based on smart-meter deployment push in India and/or based on shunt exports order book visibility?

-

Raw Material – Margins stability: Is it correct to say that in the Vishay relationship, Shivalik is insulated from RM sourcing volatility thereby providing predictable and sustainable margins. A fantastic business relationship and long-term secured relationship

-

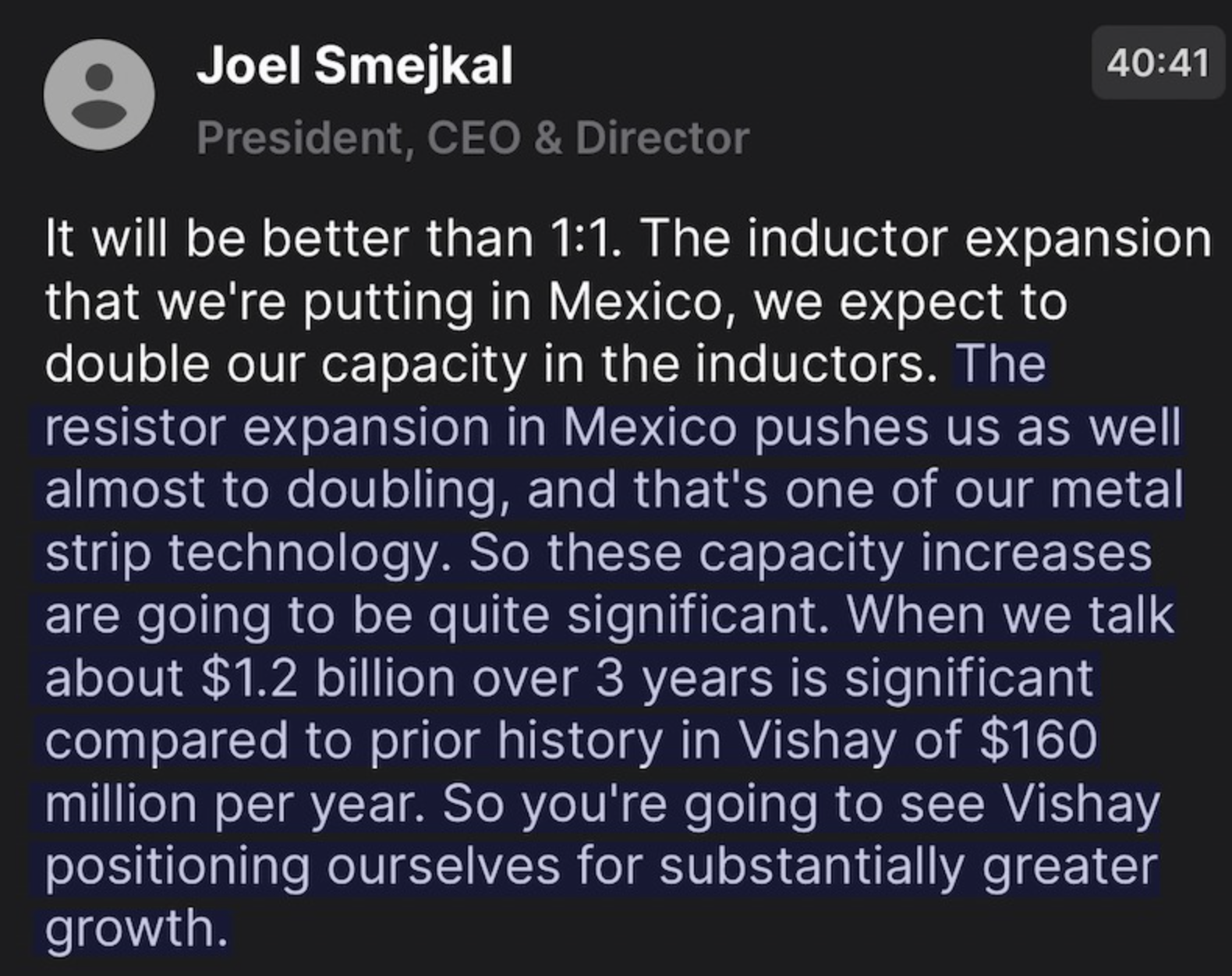

Vishay has new CEO Joel Smejkal starting early 2023. A Power Metal Strip (Shunt Resistor) specialist with many patents in this area Google Patents. Joel has been an old timer at Vishay. How has Shivalik’s relationship with Joel evolved over the years? Any change after wearing the CEO hat?

- In Vishay Q4 ’22 concall, Joel new CEO talks about capacity expansion in their Power Metal Strip business segment. Any revised expectations by Vishay from us to support this growth, from capacity and/or capabilities expansion perspective?

-

Could you share new customer contributions in FY 23 and Fy 24 in exports for shunt and bimetal – how should this trajectory play out over 1-2 years?

-

How is the global supply situation when it comes to shunt resistors? EV subsidies going away/reducing in many geographies – would this have a further setback on demand for the short term? Can bimetal compensate for any temp demand setback on global demand front for us?

-

Quarterly communications by our top client vishay talks about inventory position of their customers normalizing (inventory destocking) in post covid world. Do we have any visibility from Vishay & other clients on when we expect inventory destocking to end in the value chain & for normalized sales momentum of 20-25% growth to pick up?

-

Smart meter opportunities have been around for > 15 years now with lots of back & forth over floating & cancellation of tenders. What has changed now & why is it a large opportunity that will result in real cashflows? Genus power now has 8300 cr orderbook. Genus sources 60-65% of components locally. Since genus is largest player in industry, taking Genus as industry benchmark, what percentage of Relays going into smart meter orders which are being executed currently are being sourced locally versus imported into country?

-

What is our current market share in the relays which go into smart meters ? OEMs like schneider electric are investing 3200 cr capex including significant investment over next 3-4 years for smart meters. Are we already working with all smart meter & relays OEMs & what is the strength & longevity of these partnerships? By when can we expect significant indigenization for our components (contacts, shunts) in the country? What are the drivers for it? Are we cost competitive in smart meter shunts & contacts or would indigenisation be driven primarily by government policy requirements?

-

We have talked about both Tata & Mahindra being our customers in the EV BMS space. Currently what % of the EV BMS shunts being used in their EV are imported and what % are manufactured by us? If large commercial volumes have not yet started, when can we expect them to start?

-

We have seen supply to US in terms of shipments/ per shipment qty in recent times normalising – is this new normal with annual growth aligned to industry growth at single digits or we have levers to grow faster – at least high teens? Is there a strategy to counter this global demand context via inorganic route/ product or category expansion?

| Subscribe To Our Free Newsletter |