Fino payments bank has a unique business model that uses merchants to convert transaction customers to CASA customers. In future, they hope to cross sell loans and other financial products to their CASA customers to earn fee income.

Since the bank has very few branches, these merchants and the CASA franchise are the 2 pillars on which their business will develop. In view of this, I did a deep dive into their merchant network and CASA franchise to answer a few questions like:

-

How well are the merchants fairing when they work with Fino? How is their commission income changing? What is the review from merchants of the bank?

-

How much value is the CASA customer deriving from their Fino account? Is the value worth an upfront payment of 300-400/year? Is the fino account customers’ primary account?

-

How does the CASA behaviour of the bank’s customers compare with other payments banks and SFBs?

-

What are the key monitorables that investors need to watch as the traditional metrics for banks are not fully applicable to Fino?

Merchants:

-

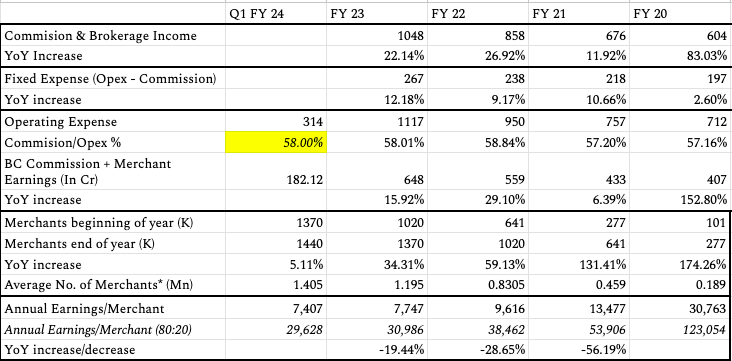

The bank has been able to increase its merchant network (own + partner) to 1.37 Mn points by FY 23 from 0.27 Mn in FY 20. A lot of the increase in merchant network has come as the company expands geographically into south and west. This represents a 5x increase in merchant network in 3 years.

-

During the same time period (FY 20 end to FY 23 end), commissions paid out to merchants has increased by a mere 17% CAGR from 407 Cr to 648 Cr. So, the average earning/merchant declined from ~30K/year to ~7.5K/year (assuming a 70% active ratio – Q2 22 con-call). Pending – Compare merchant earnings with Airtel/Paytm/Others in the same line – members feel free to contribute

-

This decrease in average earning for the merchant can be mainly due to newer merchants created in last 2-3 years not being been able to generate enough business and thus earning quite less. Older merchants should be earning similar to before with may be a little decrease because of cannibalisation – Although we should get clarification from management on the extent of cannibalisation of merchant earnings due to new merchant additions.

- So, there might be quite a lot of merchants (~2L) who are making 25K-30K/year with Fino, especially considering that 20% of merchants bring in 80% of the business.

-

The management is also quite focussed on helping the merchants earn more by providing incentives to bring in more business just as Ola, Uber, Zomato etc do. Merchant retention is crucial as a network of lakhs of merchants each of whom depend on Fino for 20%-30% of their total income may be quite a competitive advantage.

-

I also found a few interactions of Fino with merchant base (link 1, link 2) in rural areas of Bihar which is quite interesting. One concern from merchants is that Fino charges 400 Rs upfront because of which merchants are often not able to convert customers – this is actually good for investors as it maintains quality CASA franchise as long as the CASA customers keep renewing

Also there are many youtube videos on joining as merchant with fino that often have ~20K-50K views and mostly favourable comments. Seems like Fino is already quite decently known in its target demographic in rural regions.

CASA Franchise:

-

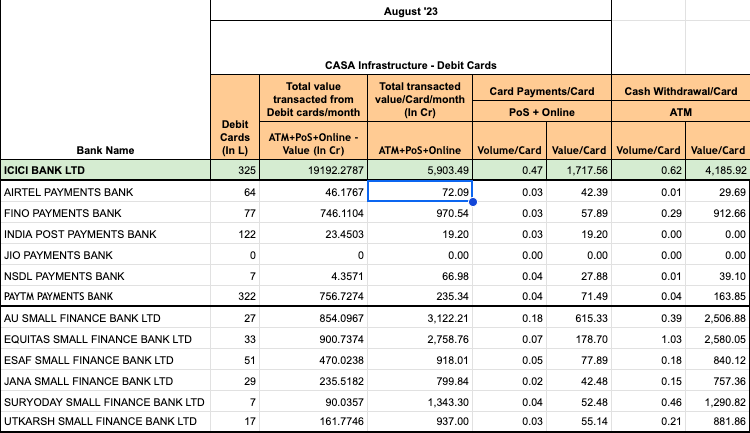

To understand the CASA franchise, I have looked at the debit card transaction figures for the last 4.5 years as most CASA customers at the bank have a debit card. Fino has increased its debit card count by 18.5x between June ’19 and August ’23.

-

Distributing cards is not a big deal, but remember almost all debit cards have been given after an upfront payment – so no lag to recover costs. Also, the total transaction value & volume have both grown by 7x over the same 4 year period. It means CASA customers are indeed using the Fino cards to transact.

-

So, the customers are using the card but are they getting enough value that they will renew? – Well, each card is used 0.3x-0.4x monthly, so 4x-5x in a year for ATM withdrawal + PoS payment. Each transaction is on average worth ~1000.

- So, an average CASA customer transacts 4K-5K in a year out of his Fino account for a total of 4-5 withdrawals. Assuming similar number of deposits and other administrative needs, an average CASA customer can interact with the bank or its merchant 8-12 times a year. I would consider Fino an important if not primary account for the average CASA customer and worth the annual fee.

- I also compared the debit card behaviour of Fino debit card customer with its peers and found the utilisation of Fino cards (per card transaction value) is much higher than all the payments bank and many small finance banks. Also, in terms of total transacted value (ATM + PoS + Online), Fino has 3x the number of Paytm Payments bank despite having only 1/4th number of cards. So, the debit cards and hence the CASA franchise of Fino is indeed robust in comparison to its peers.

Monitorables for the future:

- Per merchant earning

- Spend/Average deposit per CASA customer

- Cross-sell per CASA customer

- Renewal rate for the CASA franchise

Requesting members to share their inputs/feedbacks/comments/criticism. Excel sheet with above analysis is here.

Source – ARs, RBI Debit card data, Con-call, Investor presentation

Invested since 6 months, Biased

| Subscribe To Our Free Newsletter |