I don’t think the reach or network strength is a problem. It’s actually the execution piece, which is still underway to bring maturity in the states where they are currently present.

To highlight, they have recently entered into new two states (Delhi & UP with five branches), making the state count as 14 from the earlier reported 12. They have been good in tier 3-4 cities (smaller cities as per their IP), and when the states remain similar, the retailers and selling executive count have not grown much, mainly for these smaller cities/town. But if you check the numbers for operating branches (for bigger cities) has grown from 20 to 35 in that period. Even if you take growth from 20 to 30 (reducing the five new branches), this seems to be one of the drivers of topline growth.

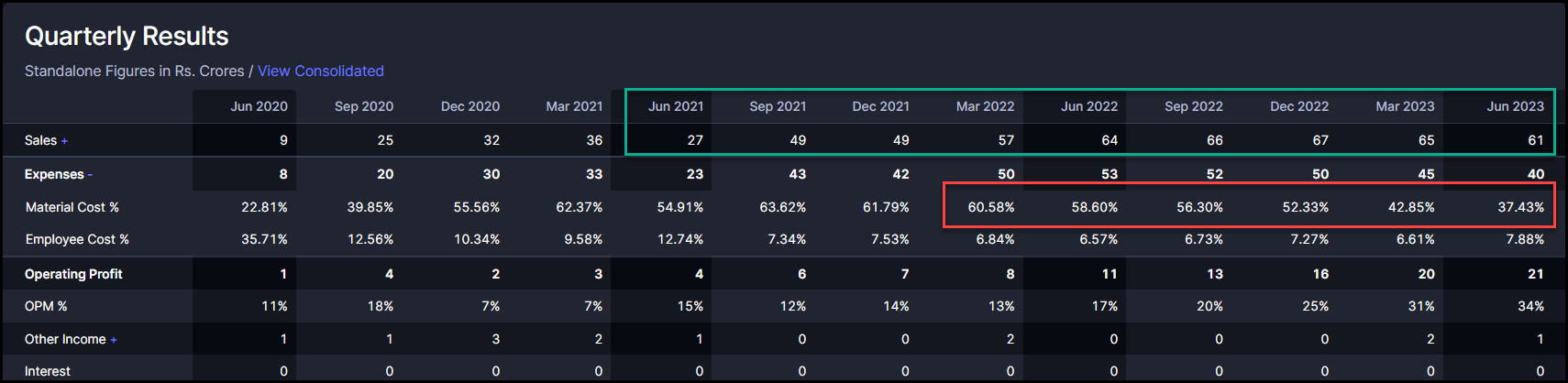

Between the June 2021-2023 period, the topline growth & EBITDA Margin expansion, in my view, is a degree of three factors:-

- Increase in companies’ operated branches, resulting in better working cycle metrics

-

Increasing brand awareness and the demand outlook in matured states, mainly – Gujarat (the company claims 30% Market share), Maharastra, MP, Rajasthan, and Karnataka.

-

Favorable crude prices were reducing the RM Cost (which is changing now).

The other thing, that is making me sweat is the Margins (from 15% to 34%). The company said the ideal range should be somewhere between 22-23% which I earlier assumed to be 18%. 3 things that you should be aware of:

- Rising Crude prices are bad for the company’s RM cost.

- Their volume growth may not be reflected in their topline due to the accounting related to their carpenter reward policy. (this also answers the question raised by someone previously and is available in the concall for more details @ 20:30 – https://youtu.be/zbwvNoa4Gus?feature=shared) Once the carpenter starts claiming the rewards (I think in Diwali and the ongoing season) the company will book it both as Revenue and same time in expense) inflating the topline but affecting the EBITDA margins.

- Increasing the maturity and penetration in states or increasing brand awareness in newer states will have positive benefits on the EBITDA. This is also the reason why I think, the company margin profile is a bit superior to the previous range of 15-18% the company used to operate in.

However, at this point, a better judgment would be to expect the margins to revert back to the 20-23% range and some topline growth incoming. The million-dollar question if you’re investing currently… is it already built into the price?

Disc: Fully Invested

| Subscribe To Our Free Newsletter |