As we end Q2, i think it would be interesting to have a relook at how some of the key verticals has performed during the quarter:

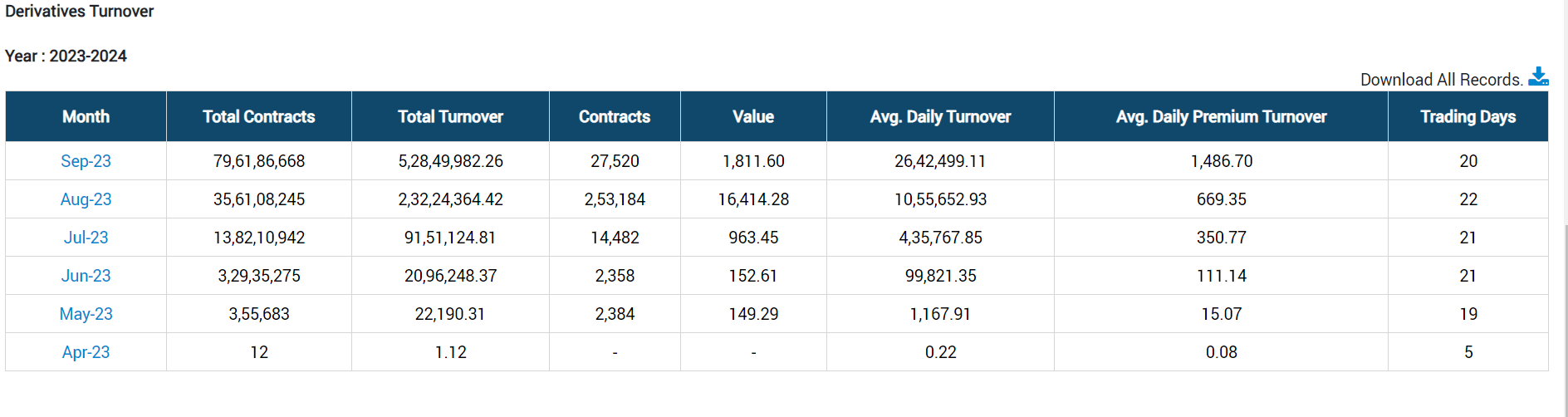

Derivatives: The numbers are roughly doubling month over month. I expect the revenue to be >2.5 Crore based on the existing pricing model of Rs. 500 per premium turnover of 1 Crore.

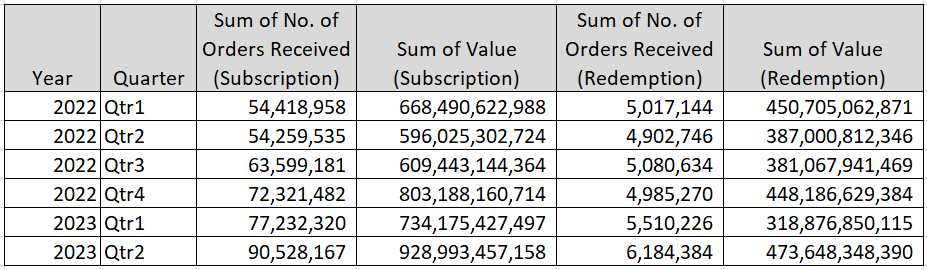

Star Mutual fund update:

The subscription orders have roughly grown by about 17% as compared to Q1 2023 and 66% compared to Q2 2022. Expect the revenue growth to be roughly in line with volume growth.

The IPO market being as robust as it is and significant growth in derivatives and Star Mutual fund, we are most likely going to see the best quarterly results(after removing one offs) since listing.

For the coming quarter we should continue to look out for the growth in Sensex derivatives and see if the Bankex can get any traction post the change in expiry date effective mid October.

It would also be interesting to see the fate of the buy back announced.

Thanks,

AJ

Disclaimer: Remain invested. Have a positive outlook.

| Subscribe To Our Free Newsletter |