I was reviewing my small holding in Metro Brands.

Metro posted 14.68 % growth in sales in the June quarter, lower than past quarters but better than most other peers. For example, Relaxo grew 11 %, Bata 2 %, Campus 5 %. I think 14 – 15 % is what its natural long run organic growth rate should be, though market growth estimates appear to be much higher. Gross margins have remained close to 58 – 60 % range in recent times. Operating margins around 30 %. Excluding Cravatex, operating margin was almost 35 % in the latest quarter. This is where Metro’s efficient outsourcing model makes a difference. Peers like Campus, Relaxo and Bata have margins in the range of 15 to 20 % but not higher. Metro’s return ratios like ROE & ROCE also continue to look good, in the 25 % range. Balance Sheet remains debt free, other than lease liabilities. Promoter salary is reasonable, at around half a percent of sales. Dividend payouts are in the range of 25 to 30% of PAT.

In FY23, store addition was the highest, and the pace has continued in Q1 FY24 as well with 27 stores added for the 3 months. This will support sales growth going ahead. Average sales per store is now more than Rs.3 crore per store, its highest on record.

The main operating cost in retail businesses is inventories. Not only inventories can be high, one does not know what they are really worth. But Metro has controlled inventories well. I understand for most of the Third-Party brands, Metro pays for the products only when they are sold, inventories are not on Metro’s account. This is such a good thing, given Third Party brands constitute a quarter of the company’s sales. New BIS Norms coming into play from 1st Jan 2024 will increase inventories, the company has said. Need to see how much this goes to.

Last year, June sales were around 25 % of the full year sales. If the same ratio holds for this year as well, the company will post a full year sales of Rs.2400 core for FY24. This is excluding new additions such as Fila. Overall, Metro leaves little to complain other than valuation. The stock has always been expensive and has become even more so in the last one year.

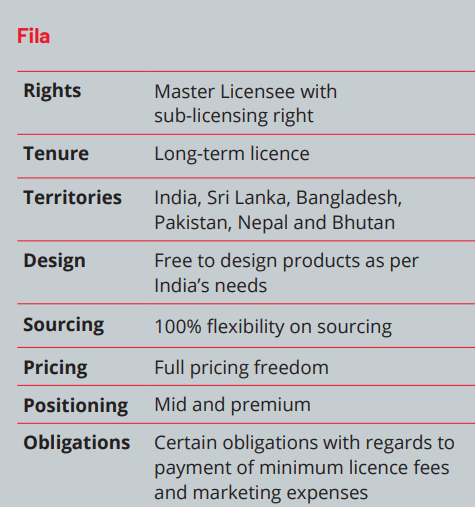

So there is a lot riding on Fila, clearly. The Cravatex acquisition cost Rs.200 crore, consuming a large part of the Rs.300 crore raised through the IPO. The biggest brands in this space are Adidas, Reebok and Puma. As per reports, Adidas and Puma have been selling more than a Rs.1,000 crore per year each. Adidas makes around 17 % ROCE and Reebok 27 %. Metro has not announced its store opening plans for Fila yet, but when fully rolled out, Fila will clearly make a big impact on Metro’s numbers.

Metro is planning to position Fila in the Rs.4,000-plus segment, which is significantly premium than at present, with 300-400 stores for Fila alone in the long run. Besides this, Fila will also be available through 500-odd Metro & Mochi stores. The company will also sell Fila accessories and apparels, besides footwear, besides the Proline range. Fila rollout will also see a sharp spike in costs I think, both for branding & promotion as well as operating costs. Fila will be sold entirely on COCO model. And then there will be license fees, about which the company has not revealed anything so far. For the long term, the sports footwear category is growing at 25 % per annum, faster than all others. The full Fila impact will come in FY26, not before. Even the analyst estimates for FY25 do not justify current valuations.

(Source: Trendlyne)

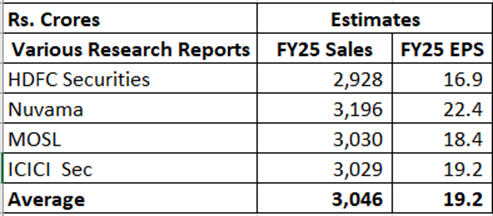

I think market is pricing in a Rs.1,000 crore revenue from Fila in FY26 probably.

| Subscribe To Our Free Newsletter |