Notes from HBL’s AGM on 29th Sep

Chairman speech

-

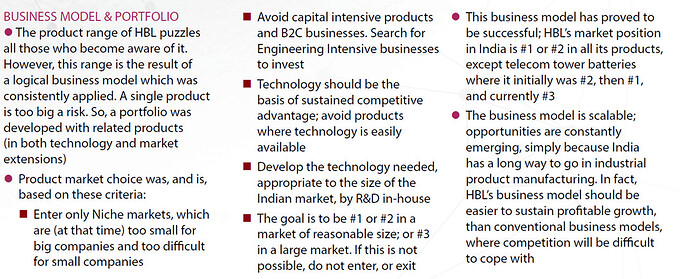

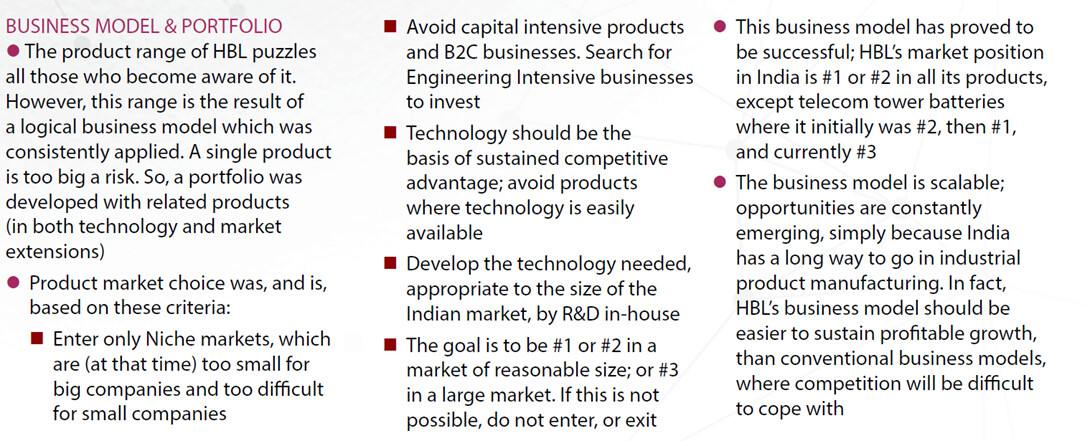

We are not only a Railways or defence or batteries company. We have a portfolio of niche products – Business model elaborated on Page 17 of Annual report – niche markets, technology advantage etc.

-

We are not a R&D company. We do lot of development and engineering, but not research. We focus on developing technology across engineering intensive products.

-

Are we going to spend as much money and time in development as in the past? Many products we developed had a long gestation of 7-15 years. But we are not going to spend as much time and money in future as in the past, and it won’t be required too. It is time to start recovering the investments and focus on high growth areas.

-

For HBL, imports of raw material as % of sales is between 7-10% for FY 22 and 23. Compared to this, HAL has 92% of bill of materials as imports. HBL Exports c. Rs 214 crs

- Import content for HBL is low

- HBL’s ambition is driven by a German term called Mittlestand (mid-sized cos responsible for Germany industrial revolution) – characterized by – target global position in niche products – and compete through technology and quality and taking care of employees – low debt, stay away from large volume price driven businesses.

-

Do we need working capital for growth we expecting? Not an issue as credit rating strong, and low outstanding debt – also we do not invest in capital intensive products – hence capital is not a constraint

-

Child welfare activities elaborated in Page 36 of AR – started way before CSR became mandatory – expand the program as Company performances further improves.

-

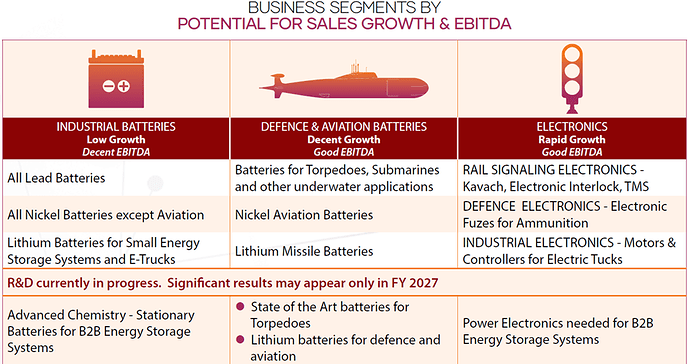

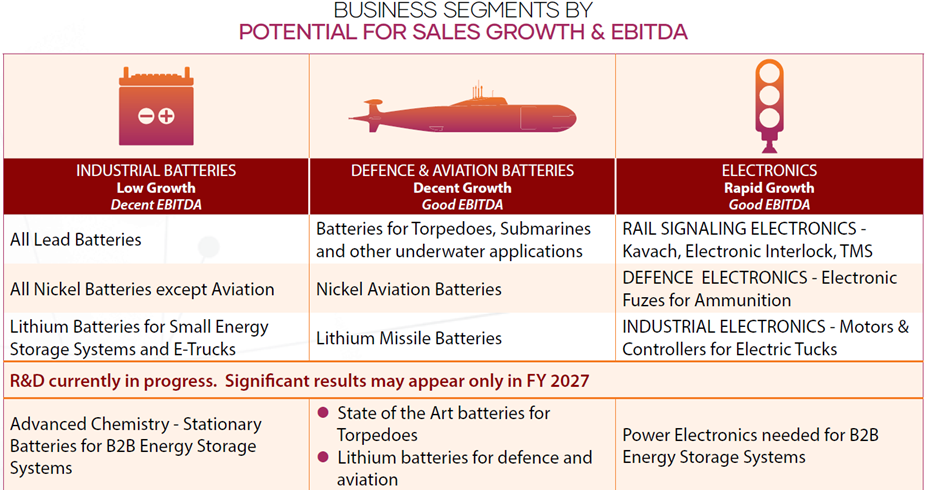

Business segments- Segmentation altered starting Q1 FY 24

-

Industrial batteries

- This segment is doing well – driven by better product prices, lower RM cost, better efficiencies and increase in productivity – may not improve further from here, may not fluctuate much – we are prepared though for a lightly lower performance in this segment

- Nickel & lead batteries co-existed for years, with lithium being a recent advancement. Arrival of new chemistry does not mean old one is dead. Telecom (4G and 5G) towers still use lead acid batteries and will still continue for few years. Lithium is used more in rail coaches in Vande Bharat (we will supply) and defence etc.

- PLT batteries (where we are the only Indian company and one of the few in the world) – Sales are growing rapidly – both from defence and data centres- niche product – superior product with limited competition – competitive strength came from technology

- Nickel cadmium batteries – we are no 2 in this segment globally – gaining market share steadily – Sales will go up, nickel prices have been reducing – increasing margins

- Lithium batteries – We manufacture lithium ion cells at a small scale (spent capex Rs 70 crs – and may add Rs 70 crs capex in next 2 years – niche market – not significant capex) – strong position in defence – navy, air force.

- We do not intend to manufacture lithium-ion cells for industrial use – as China is way ahead of India in this space and it will be tough to compete with them – Indian govt planning a PLI scheme 50Gwh capacity – of this 30Gwh allotted and will take 2+ years for production. In China, in last year alone, 240 Gwh capacity has been brought on stream.

-

Rapid growth opportunities with Good EBITDA elaborated on Page 18 of Annual report

| o | Kavach under Rail signaling electronics – |

|---|---|

| | Encouraged by RDSO to develop train protection system indigenously in 2007 – Product was developed and trails conducted successfully in Oct’12 – but was not pursued by Indian Railways as HBL was a monopoly – It took another 10 years for competition to come and orders to be rolled out in 2022 – In all, 15 years gestation |

| | TCAS roll outs are complicated (not like telecom) – There will be many hurdles for new competition – and hence competition is not a concern. |

| | Track length of Indian Railways has to be increased – added 10,000 kms in last 70 years – Government plan to add another 20,000 kms in next few years – long headroom before TCAS gets fully implemented. |

| o | TMS & Interlocking under Rail signaling electronics |

| | Sales magnitude much smaller than TCAS |

| | Interlocking – We are safest amongst other safe brands in this space, TMS has slowly started progressing. |

| o | Electronic fuzes for ammunition |

| | MHA confirmed that HBL grenades are satisfactory and imports will now be stopped |

| | Capex in progress to develop large scale facility for electronic fuzes by March 24 – sales should begin by FY 25 |

| o | Industrial electronics |

| | Convert trucks already in operation from diesel to electric – 3 other cos are working on it but their solution is not viable for truck operator |

| | HBL develops motors and motor controllers in-house for electric trucks – solution seems economically viable – Created 100% subsidiary Torquedrive Technologies Pvt Ltd (TTL) for marketing of e-trucks and its step-down subsidiary TTL electric Fuel Private Limited (60% held by TTL) for setting up battery charging facilities. The step-down subsidiary is the largest charger of 3-wheelers in the country. |

Q&A session

• Electronic fuzes

o Fuze capex is mostly infra, buildings, utilities related – Equipment capex is low – c. Rs 2000 crs fuzes can be produced with c. Rs 40 crs of equipment

o Opportunity size – MHA is not allowed to import grenade anymore; Can’t comment on size

o EBITDA margins will be higher than Kavach

o Exports opportunities after few years of selling in India

• TCAS

o Moving to version 4.0 in next round of tenders’ for FY 25

o Start with 5000kms in 1 year (last year 3000 kms) and if these get delivered, then increase tender size

o Apart from HBL, other 2 cos are not on delivery schedule

• TMS

o Every zone requires 4-5 TMS systems – Total 17 zones – c. total 80 TMS, each costing c. Rs 60 crs– much smaller than Kavach

• Tonbo status – One bid made to MoD – technical evaluation on. Other bids to come soon.

• Data Centres – requirement for batteries to be more compact, efficient – largest customer is STT. Also exporting PLT batteries to Russian helicopters, Battle tanks, and Missile launch etc.

• Torpedoes –

o HBL batteries are only approved source of Varunastra

o Cost of battery is c. Rs 3 crs depending upon silver price, of c. Rs 10 crs torpedo cost so c. 30%

o We are making 3 key sub-systems in torpedo – motors (currently development is WIP), batteries and hominghead (at customer’s request, started developing 6 months ago – will take 3 years atleast) – this will be 60-65% of cost of torpedo

o Q1 dip in defence – always lumpy – there was a requirement from BDL to speed up production of Varunastra batteries – but is difficult at our end as we are currently having lot of export orders.

• EV retro-fits

o Gave up on making e-buses the day FAME incentive was announced – do not want to pursue businesses with government incentives

o Looking at bigger trucks which has larger market size – Truck size is 35 tonnes

• Succession plan

o Separate ownership and management

o German system of ‘Supervisory board’ akin to BoD and ‘Operations board’ akin to Management – trying to separate ownership and management on these lines

o Working on succession of key executives also

Regards

Yachna

Disclosure: Invested

| Subscribe To Our Free Newsletter |