Its been almost a month since my last two bearish sounding posts. All I hear in the news these days are yields, crude and dollar strength. Unfortunately, nothing in life is so black and white.

I am still bearish enough to be 40% cash and bullish enough to have moved from 60% cash to 40% cash since 10 days. There are still value bets with fundamental tailwinds and/or triggers to be found in this overheated market and that’s where our focus should be.

There are odds that we might undo 40 years of globalisation going forward. What that might do to interest rates, inflation, valuations is downright scary but that’s not the only possible outcome.

There are some stocks which are showing significant strength above 12th Sept Open/Close – this is the pool of strength to fish from, if you are a trader. As market breath narrows, this pool generally gains significantly.

Some new bets / adds to old bets –

Shilchar, Daily – Was consolidating in a channel. Has broken out since

This is an old bet I had reduced but have scaled it back up post the AGM. The management is guiding for 350 Cr sales in FY24 and getting to 800-1000 Crs in 3-4 yrs with margins maintained at FY23 levels. Still quite cheap as compared to TRIL which is primarily a power transformer play (much lower per MVA realisation) and also doesn’t have UL certification like Shilchar that allows Shilchar to export a lot to US markets. Given the margin profile, I dont see why Shilchar shouldn’t trade at higher valuations against TRIL (same thesis as last time). The energy transition theme will continue to play out irrespective of what else happens in the world. Should however see if funding continues in a high-rate environment with the same zest as current

Garware Hi-Tech, Weekly – Discussed earlier in this thread here. Was showing significant strength after the AGM. Management is showing signs of being fairer to shareholders. Business also is doing very well with PPF exports picking up a lot. One of the earlier ones to gain from the Sept 12 lows. Still considerably undervalued compared to rest of the market

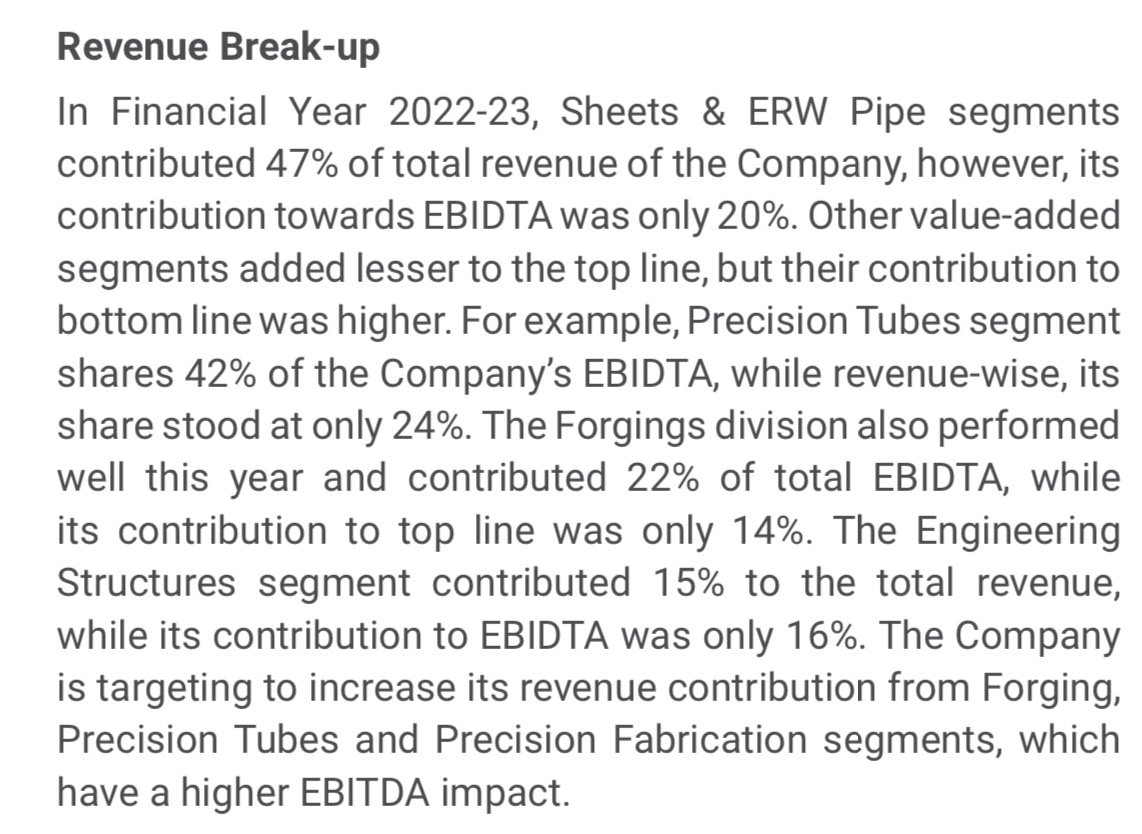

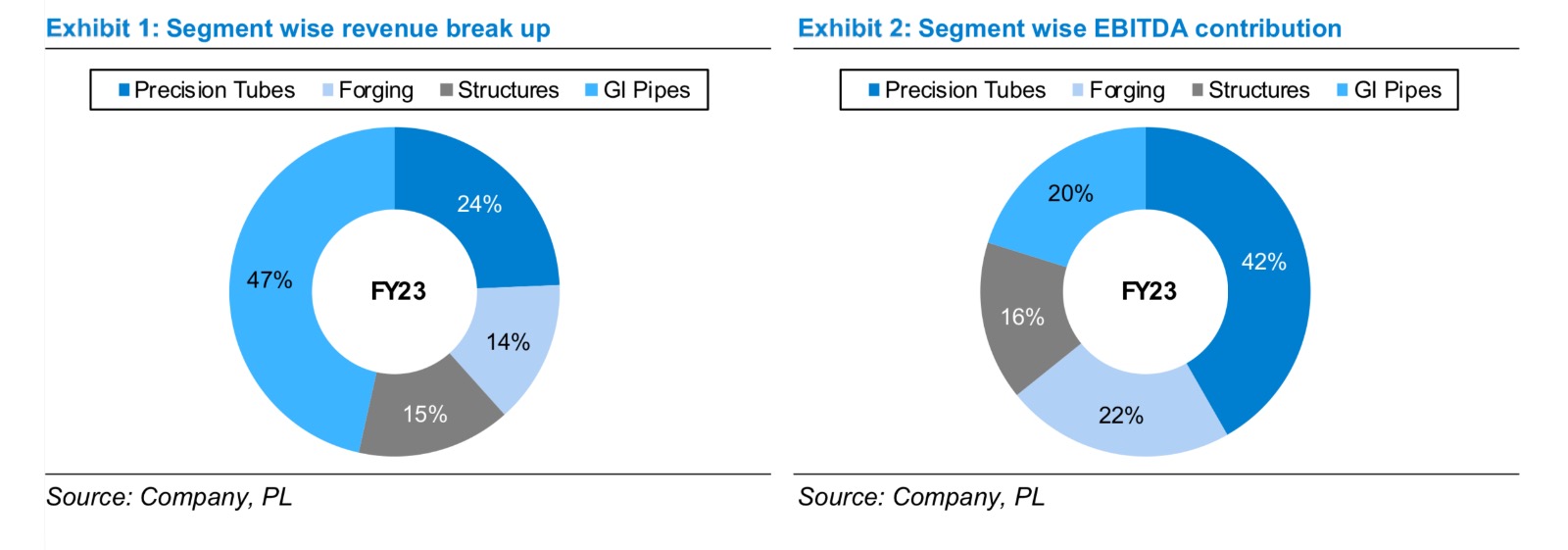

Goodluck, Daily – Came in the radar again as it passed the Sept 12 Open/Close and was trading near 52 wk highs in a very weak market

Business is undergoing a transformation from low margin ERW pipes business towards precision tubes (shocks, steering, fuel injection etc), forging and precision fabrication

The margin contribution is much higher in precision tubes amd forging and thats where the expansion currently is happening.

Incidentally, after I took a position, there was an announcement of capital raise to the tune of 96 Cr – around 30 Cr from promoters and 66 Cr from others via pref allotment and warrants (at 600 Rs. which should be bottom) towards defence and aerospace forging foray

Beekay, Monthly – Appears to be a long-term breakout.

Fundamentally as well from Q4, Maheshwari Ispat which they acquired cheaply willl start contributing. The total contribution from this plant is expected to be ~800 Cr with a 10% or so margin. The ramp-up though might take a year or two to get there. There are long-term triggers as well in FY25-FY26 from their Kalinganagar plant. Not a very liquid stock, so I could only buy a small position

Disc: 40% cash, so views might be bearish. 60% invested, so views might be bullish. Have position from Garware from 1000 levels and added around 1300. Shilchar from much lower levels, added around 1500. Goodluck between 600-620 and Beekay between 615-650. Writing for self clarity. I am very much a novice and could be wrong in my judgement

| Subscribe To Our Free Newsletter |