Hello friends,

Wanted to highlight below points on Rainbow Children’s Medicare –

-

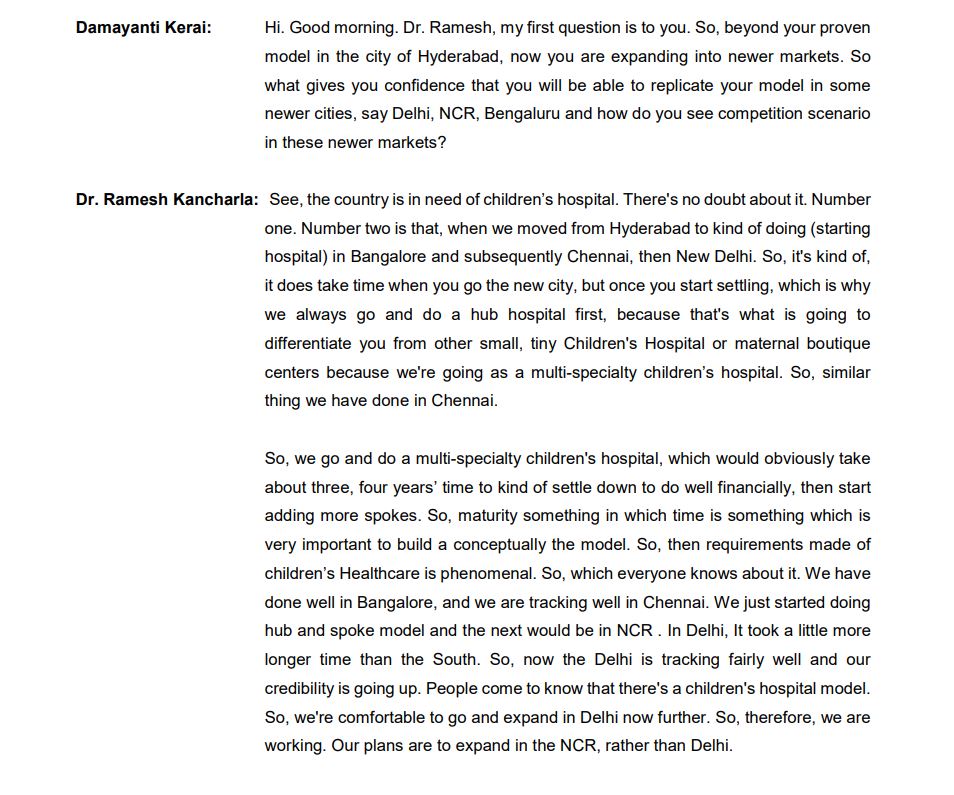

Initially started in Hyderabad and achieved phenomenal success. Management was able to replicate their proven model in other cities – Bangalore and Chennai. Now, even Delhi is tracking well and that gave them the confidence to plan hub in Gurugram (Hub – 400 beds – 450cr greenfield capex)

-

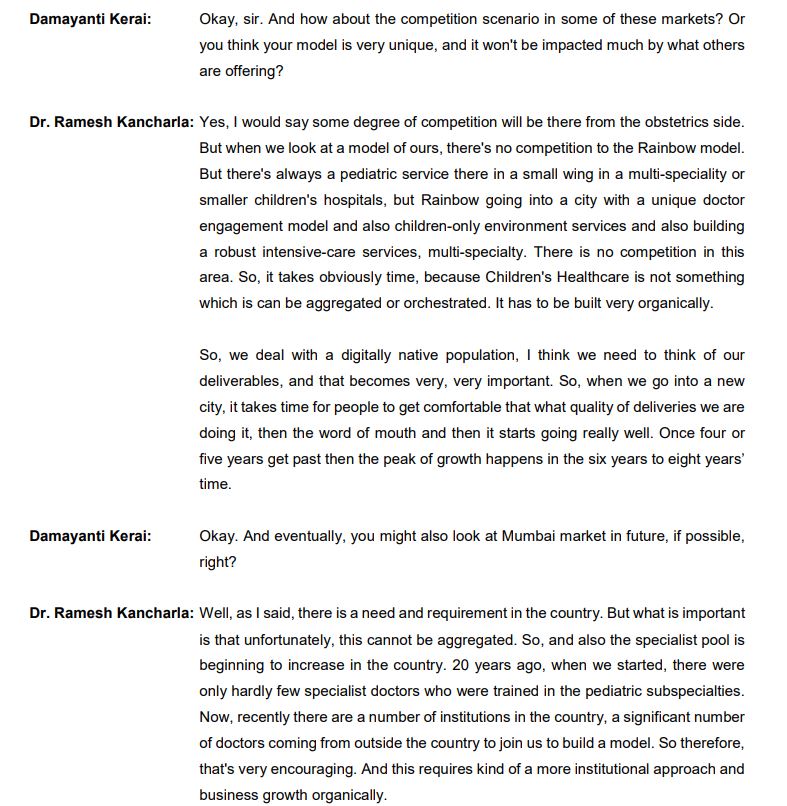

Rainbow’s hidden moat is their doctor engagement model, children-friendly environment and robust tertiary level services. No competition w.r.t these factors and it is not easy for new entrant as children’s healthcare needs to be built very organically.

-

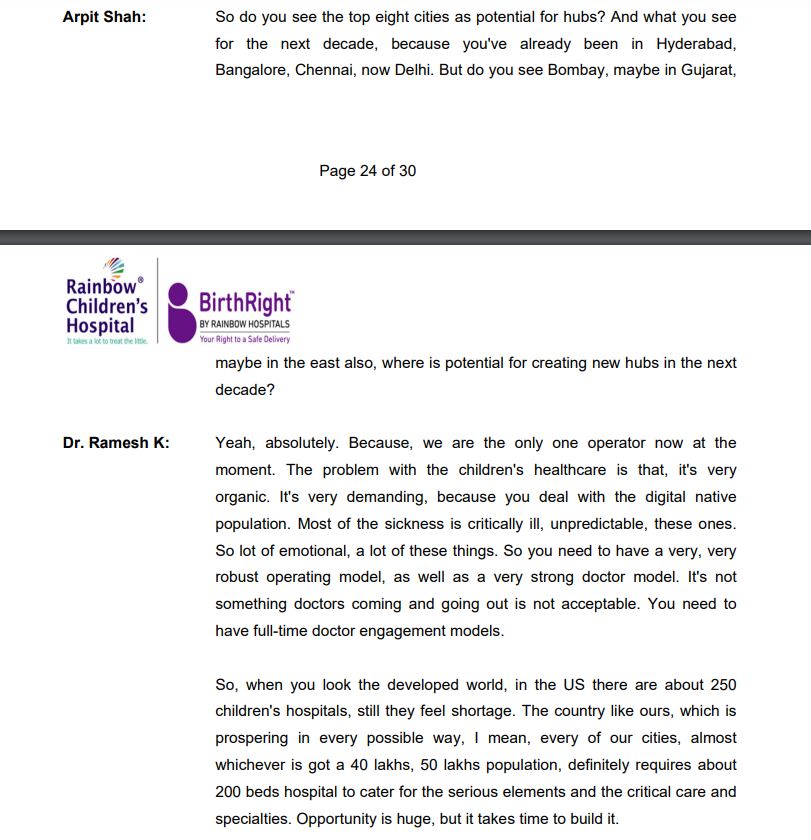

Any city with a 40-50 lakh population definitely requires min. 200 beds hospital to cater to critical care and specialties. Opportunity is huge, but it takes time to build it as children’s healthcare is organic.(In a way entry barrier)

-

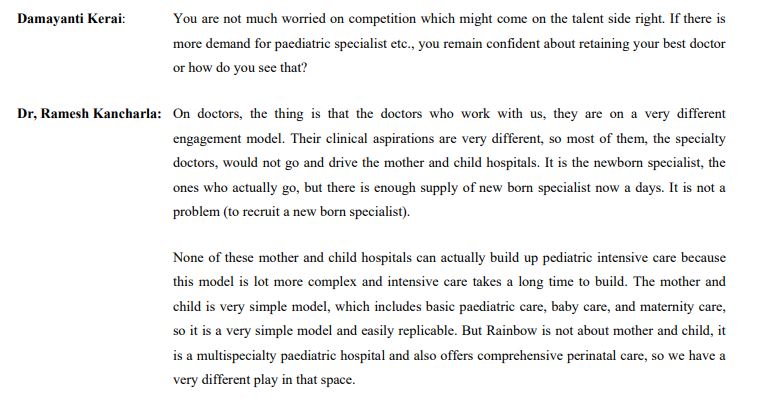

Rainbow’s target base is critically ill children or complex problems where there is miniscule competition. Small children’s hospitals won’t be their competition. In fact they will refer to rainbow for complex cases.

-

None of these mother and child hospitals can actually build pediatric intensive care because this model is lot more complex and intensive care takes time to build. Rainbow has a very different play in this space.

-

Breakeven in children’s multispecialty at 30% occupancy (This is much better compared to general multispecialty).

-

Q2 and Q3 are generally peak season for pediatric business.

-

TAM to double at 14% cagr to 1,78,400cr by 2026

-

I believe Rainbow has best in class metrics compared to listed hospitals (capex per bed, ARPOB, ALOS etc). Eventually market might reward it with premium EV/EBITDA multiple.

Disclosure: Invested, and Not a Reco.

| Subscribe To Our Free Newsletter |