Apart from what @aceinvestor_75 already shared, here are other noteworthy things from consolidated Q2 FY24 results:

- Cost of materials consumed was significantly down from 41% to 26% YoY

- Overall expenses down from 83% to 60% YoY

- Revenue up 50% YoY and down 21% QoQ

- PAT up 161% YoY and 100% QoQ

- PAT margin at 29.6% vs 27% YoY and 11.6% QoQ

- Current assets show Trade Recievables of 78.72Cr (44% more than this Q2 sales) which should hopefully materialize in the upcoming quarters for this FY.

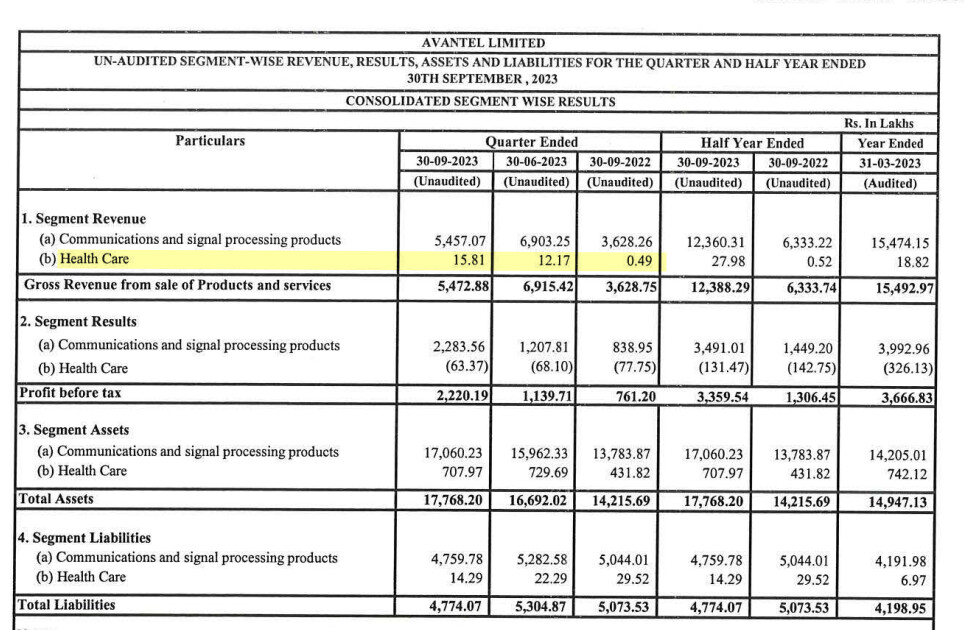

- Revenue from Imeds Global was miniscule (~16 Lakhs).

My takeaways

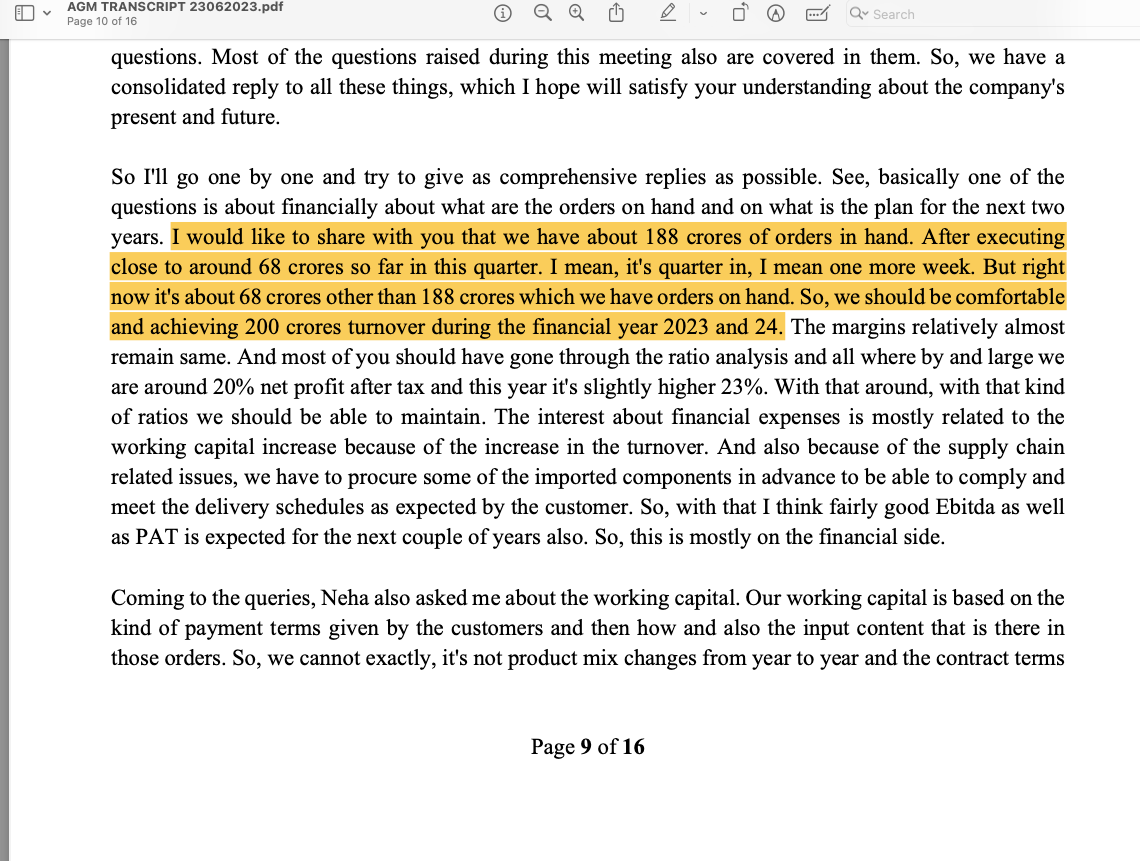

- The TTM revenue for FY24 seems on the path to achieve the guidance of 200Cr (+). Here’s what management had said in AGM held in June 2023.

- On the Imeds Global front, since it is still in a nascent stage and they’re working on getting necessary approvals, certifications, etc. think that biz would hopefully start contributing in a meaningful manner only from the next financial year as per management’s commentary in June 2023 AGM.

| Subscribe To Our Free Newsletter |