KPI Green posted a good set of Q2FY24 numbers. The order book looks decent in terms of future growth.

-

Revenue grew 34% YoY and 14% QoQ

-

PAT grew 67% YoY and 6% QoQ

-

PAT margin declined a bit QoQ but is stabilizing in the range of 15%-17%

-

346+ MW projects executed so far till H1FY24

- 313+ MW cumulative projects executed till FY23

- 33+ MW projects executed in H1FY24 alone (10% of total execution till FY23)

-

541+ MW total orders in hand (1.56x of total orders executed so far, )

- 385+ MW new orders received in H1FY24 (1.1x of orders executed till H1FY24)

- Consists of two big orders: 240 MW under GUVNL tender and 145 MW from Ayana Renewable Power Four Pvt Ltd

- 156+ MW backlog until H1FY24

- 385+ MW new orders received in H1FY24 (1.1x of orders executed till H1FY24)

-

887+ MW orders already secured out of 1000 MW target by 2025

- Only need 110+ MW additional orders to hit the target (looks very much possible!)

-

ICRA reaffirmed A- (Stable) credit rating for long term at an enhanced rated amount

-

Segments:

- 18% revenue share of IPP (vs 22% in Q1FY24)

- 82% revenue share of CPP (vs 78% in Q1FY24)

-

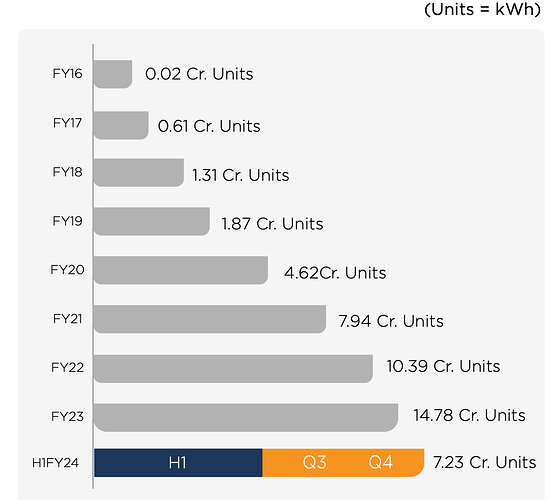

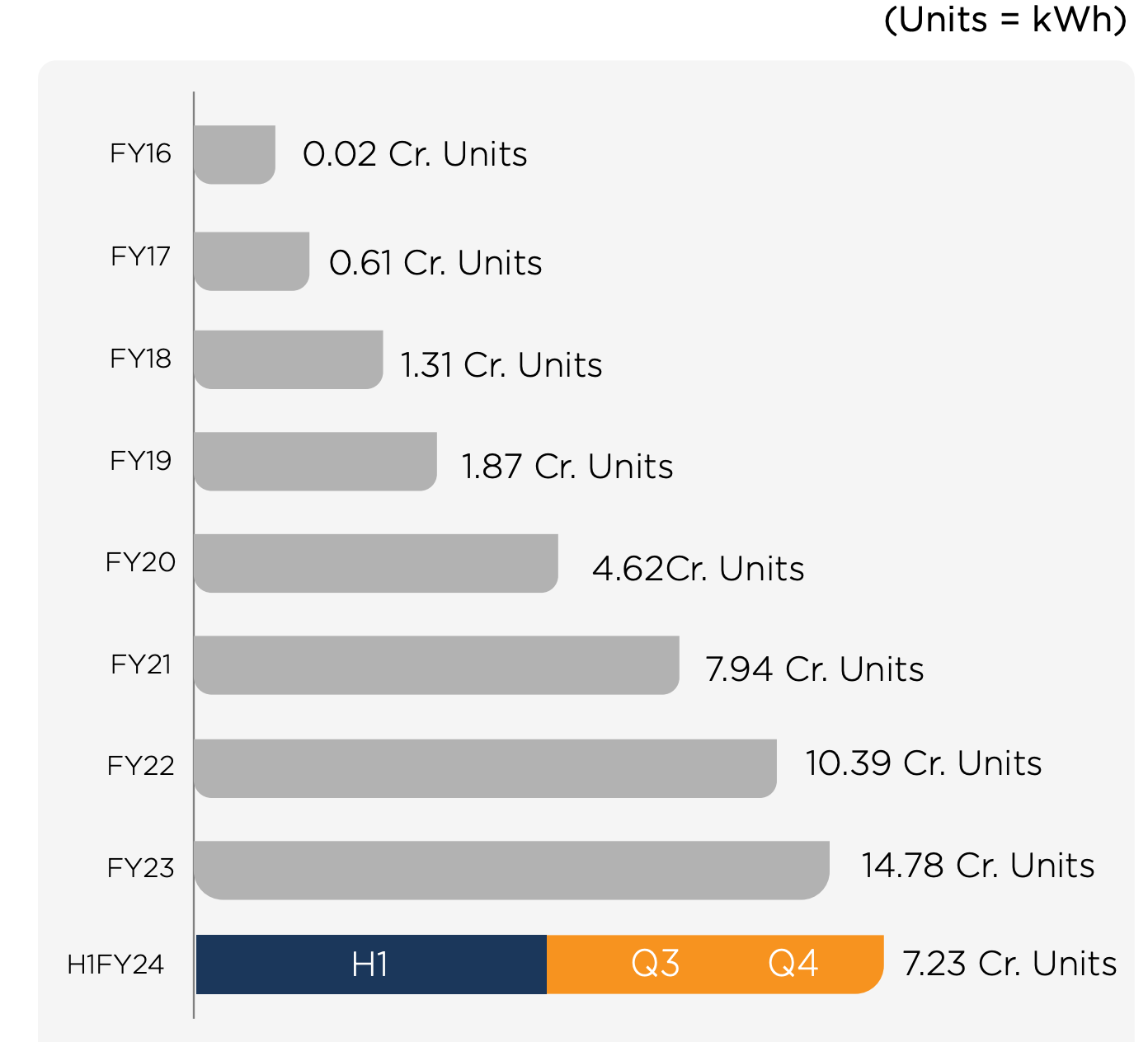

Unit generation growth under IPP is steadily increasing

-

Increasing moving towards hybrid model (solar + wind energy) which help grid stability due to reliable, efficient and sustainable approach to energy generation. It enables commercial optimization of transmission charges and the effective utilization of grid capacity.

- 145+ MW hybrid CPP orders received during Q2FY24

- 185+ MW hybrid CPP orders as on H1FY24

| Subscribe To Our Free Newsletter |