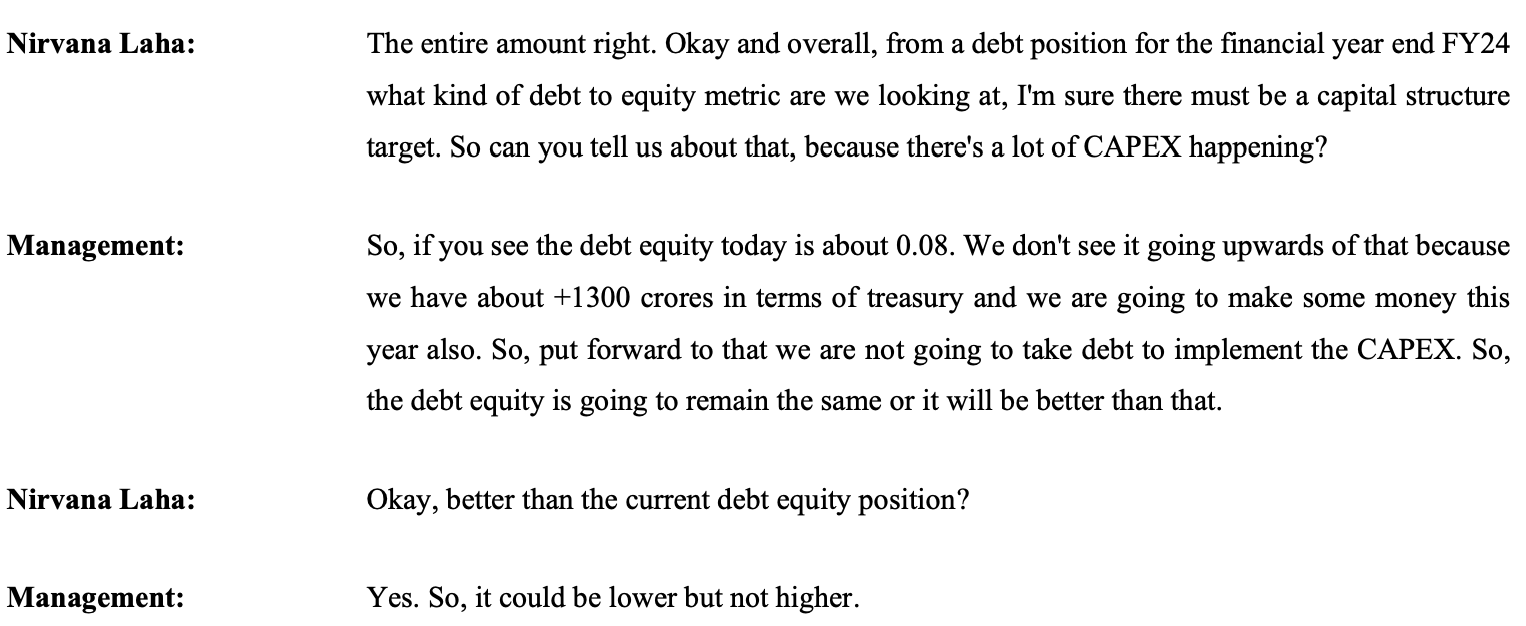

Hi @suhagpatel

The business is quite cyclical and the margins are unlikely to be consistent. My understanding is that this cyclicality should reduce over the next few years. I haven’t been able to find time to document the thesis – broadly it revolves around the following points:

Expectations

-

Capex: The company has been investing in massive capex / backward integration. I like how most of this comes through the cash generated/non-debt. Here’s what happened in FY22

Here’s what happened in FY23:

This ppt would give a better idea of where’s this capex is going. Is the management skilled enough to use this capacity? If things turn out as per my expectations, it could drive higher profitability.

I also find it interesting how the company has been trying to diversify different segments such as aluminum foils (~EV battery) – I believe they have a collaboration with Achenbach – but that’s a different story. [Source]

- Debt: High debt is something that always has made me avoid steel companies. However, Shyam doesn’t have much debt at present. Management doesn’t look like they’ll go crazy over here which makes me interested.

Valuation

I would have preferred to enter at a lower price. At these valuations, I’m okay (okay not excited):

- a) Ideally one may want to look at EV/EBITDA. However, for me, MCap to Sales has worked much better so I do prefer it.

- b) Company recently had a successful OFS at 411

(2 years since IPO – I did ask why would the company be valued at approx listing price?).

Management

Looking at the team, one might feel good about corporate governance. I have mixed opinions. However, the management broadly has been consistent with their words so I got intrigued. Here’s what the management claims/expects:

There are things I do not like about this investment:

-

Investing in companies where timing is crucial, isn’t something that I prefer. I do not think i’ll hold this stock for the long term. Management commentary proved my understanding here. Let’s see how the plan goes.

-

I still haven’t completely analyzed through their pre-IPO journey which is a serious risk on this investment.

-

A lot of unanticipated things can go wrong in such business

This is all I could write due to time constraints. In my opinion, before analyzing this business, one may want to look at GPIL.

I hope I was able to give you a direction.

Disclaimer: Invested and biased. Not a buy/sell recommendation. I am often wrong and change my views. Further, I may buy/sell stocks without informing anyone.

| Subscribe To Our Free Newsletter |