ITC Q2FY24 results announced yesterday.

Positives:

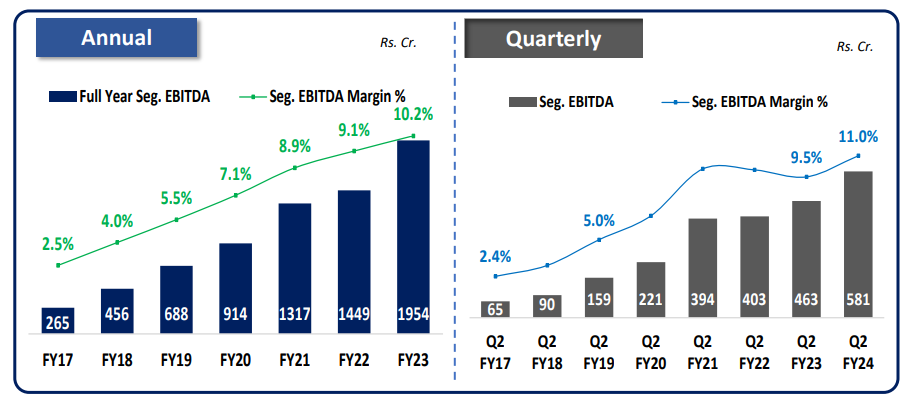

Cigarette and other FMCG continue to grow (although growth rate decline to single digit due to high base of Q2FY23). FMCG others EBITDA continue to remain in double digit.

Hotel and IT business continue remain in strong growth path.

Negative:

Paper segment sales and growth decline due to lower export demand and increased supply from China.

Agri Segment adversely afffected due to ban on exports of Wheat and Rice.

Overall, the company continue to remain in path of asset light growth. If it continue to show double digit revenue growth for next 3-5 years, ITC FMCG others may become eligible business for seperate company in my view. Hotel demerger continue to remain on course.

Dsicl: Among my Top 2 holding. My view may be positively biased. I may exit/add my position without informing forum. Not a SEBI registrered advisor. Not recommending any investment action. No trading in last 90 days.

| Subscribe To Our Free Newsletter |