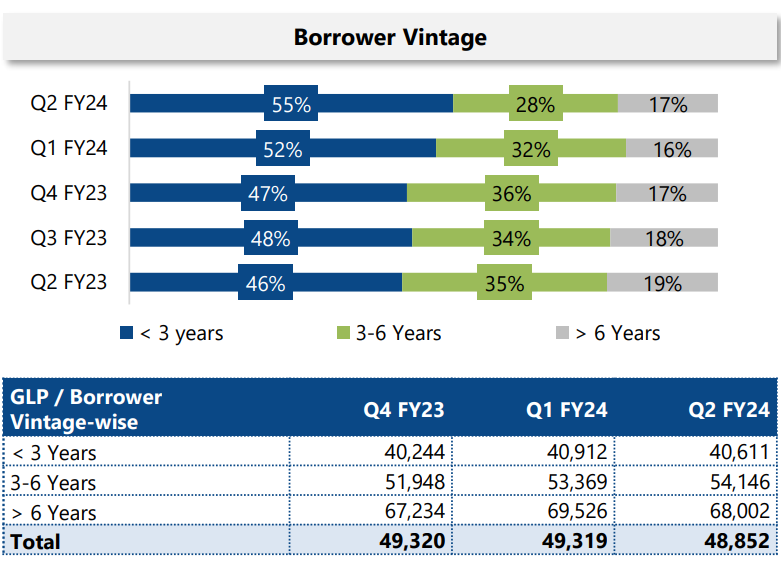

Wanted to focus on the borrower profile and how the company is scaling up to see if it is sustainable.

Some observations:

- New borrowers are being added with entry into new markets

- Some existing borrowers (3-6 years) migrate to > 6 years, which results in maintaining the ratio of > 6 years pie

- Some of existing borrowers (3-6 years) stop borrowing and churn

The GLP ratio per vintage profile shows a slightly different picture.

- The quantum of GLP for new borrowers is roughly constant in last 3 quarters

- More loans are given to existing borrowers

- GLP ratio of > 6 years is also fairly constant compared to Q4FY23.

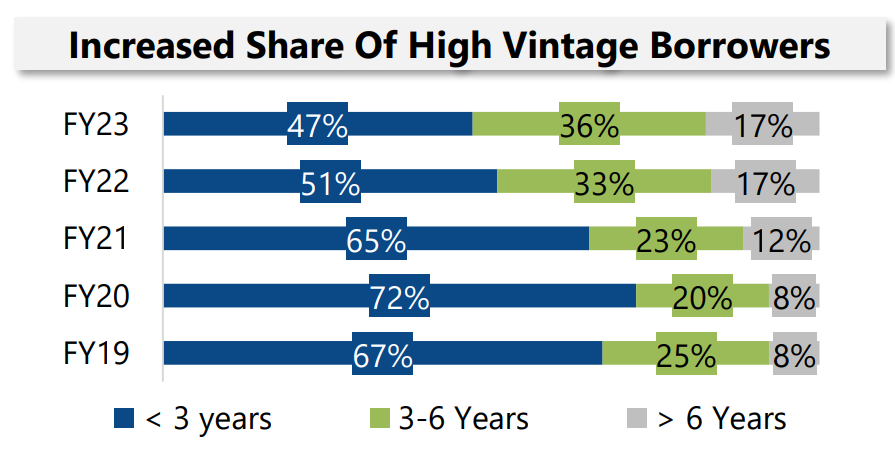

This means that the company is issuing smaller ticket sizes compared to last year. May be because they are scaling up their home improvement loan, which has almost doubled since last year. This is also reflected in their loan ticket size, which is much smaller for home improvement compared to income generating loan (IGL).

So, all the three checks out well: Borrower vintage, GLP distribution and Loan ticket size.

The good points are:

- They are not adding risk by scaling their new customer base and associated GLP. So, seems like a sustainable growth with a tight control on NPAs (GNPA is 0.77%).

- They are also able to retain their customers better which establishes a strong & stable base

- They are scaling up home improvement, which is good as this sector is expected to grow

- Retail finance is growing fast, but has a smaller base. But this is another growth area.

Disc: Invested

| Subscribe To Our Free Newsletter |