I couldn’t ask some follow up questions in yesterday’s concall as they had run out of time. Mr. Nath had asked me to write to IR or take it offline.

I have sent the following list of follow up and additional questions: (My comments for VP in brackets)

-

I think RBI has capped FLDG at 5% for each FinTech. Your presentation still states 5 – 15% FLDG cover. So how much does this impact your growth and existing partnerships which are >5%, have they been changed to 5% FLDG?

-

How do you ensure FLDG is 5% at the FinTech level and not for each partnership that the FinTech has?

-

We seem to be the preferred player for secured MSME co-lending among PSU Banks. When do you think PSU Banks will open the flood gates for unsecured lending? Is any other NBFC doing co-lending for unsecured loans for PSU Banks?

-

Is 100% of our collection digital? Or do we still have some cash transactions? When will we become 100% digital in terms of collections?

-

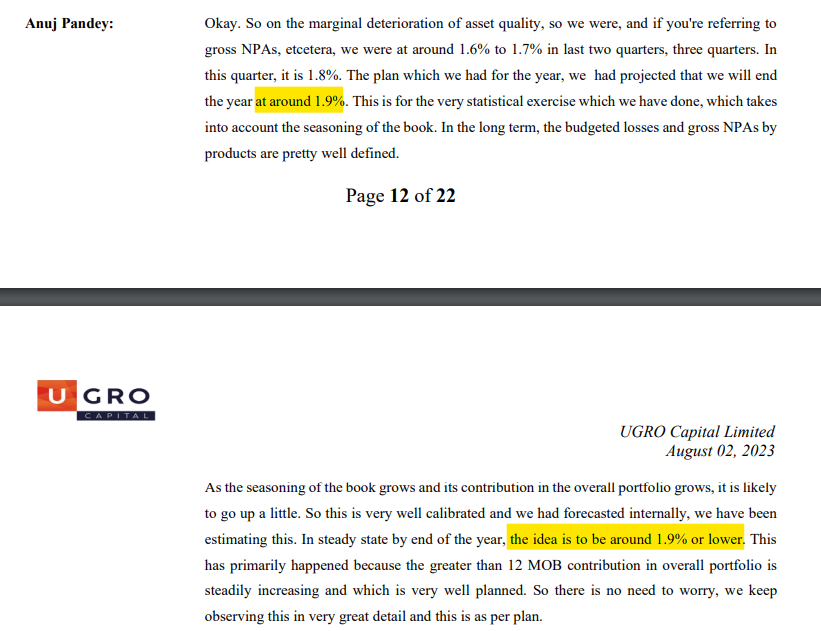

You said the GNPA in prime unsecured to stabilise at 4.0%. Previously you had stated 3.0% – 3.5%. What is the normalised GNPA in this segment?

(The GNPA goal post for unsecured seems to be trending higher with every quarter. Looks like the Mgmt themselves aren’t sure?)

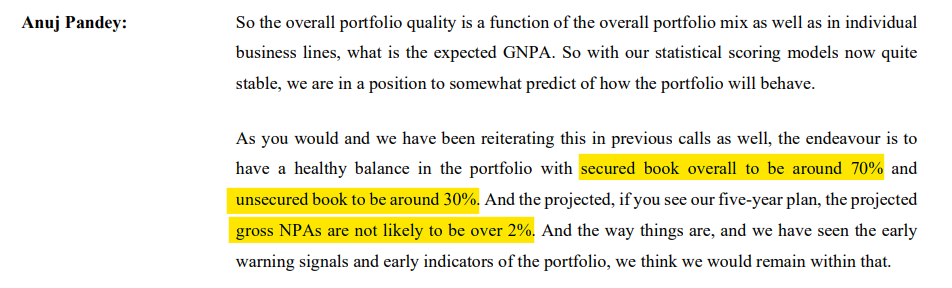

- Say, Unsecured is 30% of mix with GNPA of 4%, and Secured is 70% with GNPA of 1%, is the overall GNPA of ~2% (1.2% + 0.9%) a decent assumption?

(But currently, the secured itself is trending higher than 1% and increasing. So, 0.31.2% + 0.71.5% = 2.25% is where GNPAs will settle at?)

-

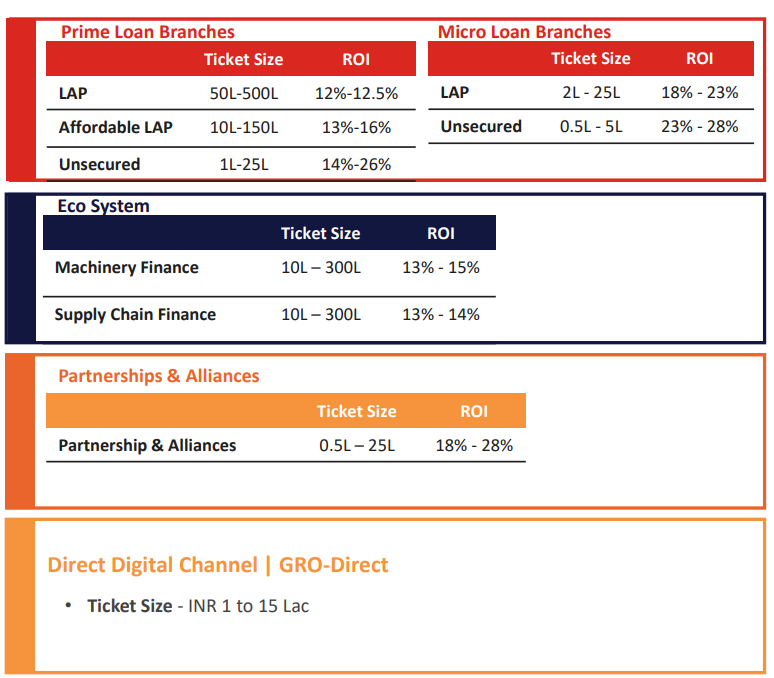

How much of micro enterprise is unsecured? Do you want to start giving the breakup of the micro enterprise as well similar to Prime?

-

In Supply Chain Finance, what is the proportion of loans to Anchor Customers vs total supply chain finance AUM?

-

Asset quality deterioration in supply chain finance is basically default by large anchor customers but scale is achievable ONLY by onboarding more anchor customers with risks cascading. How do we see the risks in this business going forward? Do we have anchor level caps? Or anything else?

-

You said in call that you want to keep the Supply Chain book granular and hence dropped ticket size from 1 Cr to 50 Lakhs. But if I check Q4 FY22 ppt, the ticket size is only 42 Lakhs. Q4 FY23 PPT, the ticket size is 95 Lakhs, Q1 FY24, the ticket size is 103 Lakhs, Q2 FY24 it is 49 Lakhs. Why this volatility? Even the tenure dropped from 0.5 years to 0.25 years. What is the existing book ticket size and what is the ticket size going to be for new loans? Looks like we are learning lending on the job which is not the right way. Either that, or we wanted higher growth and hence we started disbursing higher ticket size. We should be learning from other lenders and their past track record. Say someone like CUB.

(Was Mgmt chasing growth at the cost of risk and now course correcting? In one slide in H1 FY23, they have even mentioned 5 Crs for LAP and 3 Crs for Supply Chain. Now they have removed these slides.)

-

How does our ticket size compare with SG Finserv? What do we do differently than SG Finserv, CSL Finance and other MSME or supply chain lenders?

-

How many anchors do we have currently? How many are we planning to add in H2 FY24 and FY25?

-

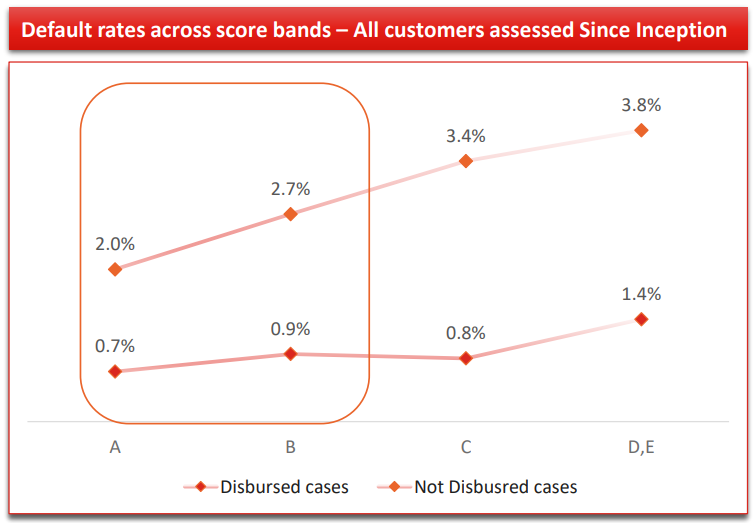

A dumb question. In Q4 FY23 PPT, Slide 10 where you talk about Default rates across score bands – the disbursed default rate of D & E is higher than not-disbursed A and B. So why even disburse to D and E? You can disburse to only A, B and C?

And in 6 months, Q2 FY24 PPT, Slide 11, now the disbursed default rates for D and E are much lower than not-disbursed B and C. What changed in 6 months since this data is “all customers since inception”? Does it mean significant deterioration of not-disbursed customers and that the UGro score is working to tee?

More importantly, why has C’s disbursed default rate declined from 1.2% to 0.8% and D&E from 1.7% to 1.4%? Is this being skewed by new customers who don’t have any default at least for first 3 months?

Please give cohort level data.

Q4 FY23:

Q2 FY24:

-

What are the approval rates in each of your products and score bands?

-

D and E score, which loan product is the major contributor? Unsecured or Secured?

| Subscribe To Our Free Newsletter |