From All time high to 16% down.

Kotyark has a wild day.

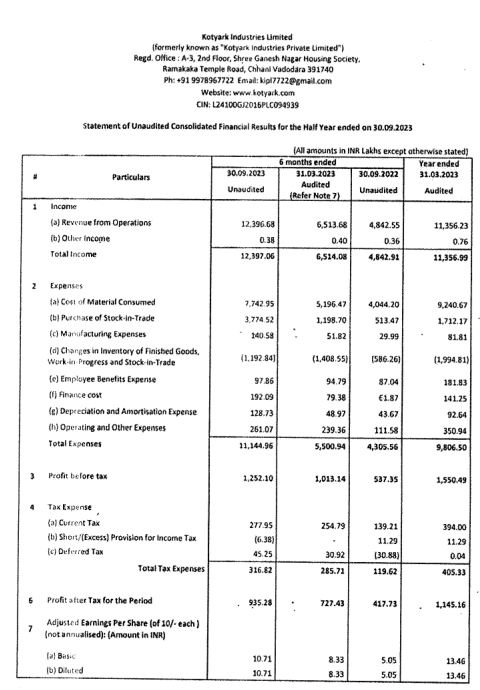

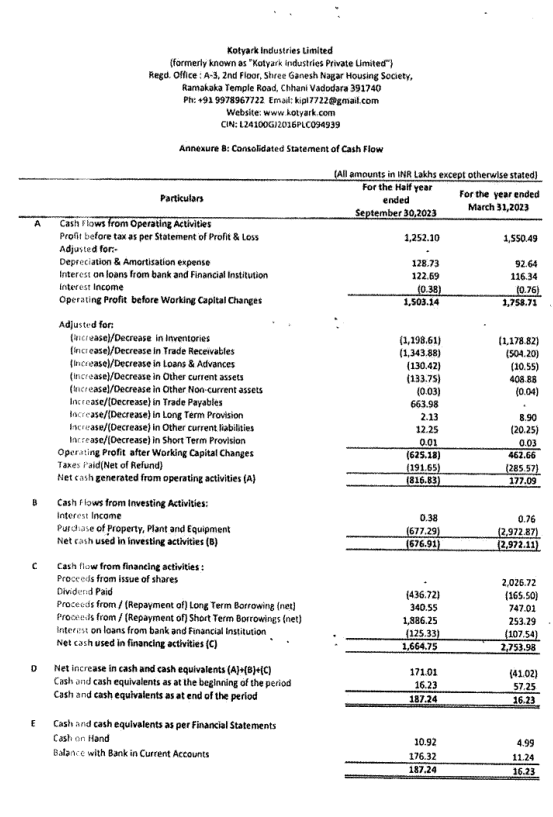

Profit & Loss looks good but Cash flow doesn’t look good.

Sales in current Half is more than PY whole year.

Reg_30_outcome_of_BM_30_oct_30102023134804.pdf (nseindia.com)

Capex is completed as per Balance Sheet.

Working cycle is absolutely stretched and funded by ST borrowings resulting in the increased Finance Cost.

NP ratio is lower.

Net Profit Ratio:

| H1 FY24 | H2 FY23 | H1 FY23 |

|---|---|---|

| 7.54% | 11.17% | 8.66% |

On Another Thought, the consolidation with Yamuna might be the reason.

Yamuna had high sales with very low margins.

I don’t know whether the related party approvals in AGM have already impacted the P&L in H1, but they shall definitely impact margins of H2.

| Subscribe To Our Free Newsletter |