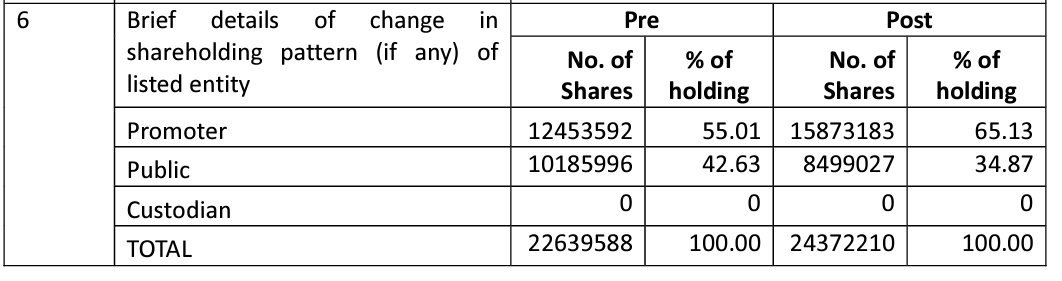

I am still trying to understand the transaction but here are my two cents. The Net worth is not representing ‘Market cap’ but the ‘Book value’ of the company. But I don’t think it makes any difference in this deal. Important point to note is the change in equity holding-

While Promoter holding has gone up by 33 lakh shares, interesting thing is that Public shareholding has gone down by 17 lakh shares too. As per my limited understanding, it should only happen if ‘Transferor’ company already had some shares of Praveg and they are now moved under ‘Promoter’ fold.

In addition, another 17 lakh shares are issued (2.43 cr post against 2.26 cr pre) which translate to an equity dilution worth roughly 90 crores at CMP of 550 INR per share. Based on remarks made by other members, I believe this is the amount Praveg is paying to the ‘Transferor’ company for buying the two properties that they own.

I don’t know yet if it bad corporate governance case, but it looks like company has not explained the deal in detail and that raises some doubts. But as we know with most small caps, they are not very good in explaining things to shareholders so I am willing to wait for more clarity to emerge.

Disc: Invested

| Subscribe To Our Free Newsletter |