Post Q2FY2024 results of Jagran Prakashan, I find that the company performance has not improved. As per presentation of the company, performance continue to be adversely affected by limited growth in advertisement revenue and higher newsprint cost. While it expect improvement on both these factors and report improved performance during next H2FY24, I find something specific to the company which has adversely affected the performance then industry wise issue.

The rival to company in Hindi newspaper, DB Corp also reported number for Q2FY24. DB Corp continue to show superior performance due to higher advertisement revenue growth in lower newsprint cost.

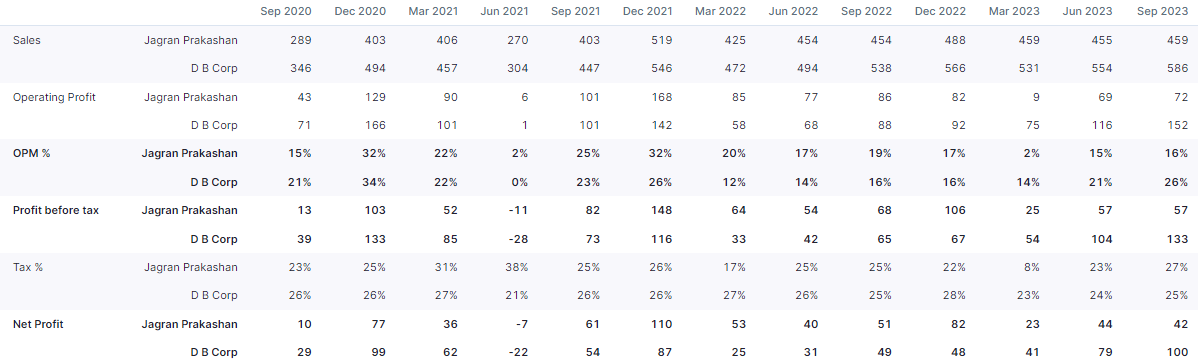

Find enclosed quarterwise performance of both the companies.

In September 2022, Both DBCorp and Jagaran operating profit comparable Rs 88 cr and Rs 86 Cr respectively. In next 12 months, DB Corp Operating profit almost doubled to Rs 152 Cr same, for Jagaran declined during the period.

So, in my understanding, while the industry is doing reasonably, Jagarna Prakashan has lost market share to the peers in last 12 months. I would contribute to promoter family conflict as main factor for lackluster performance. Since, Jagaran Prakashan, was short to medium term trade (with expectation of benefit from higher ad spend in election year and lower newsprint price), I would have to exit at appropriate price. Given the family conflict situation, it is difficult for me to visualise benefit of better prospect being reflected in company performance. Hence, I have decided to exit from my holding in the company.

Disclosure: My view may be negatively biased due to my exit from the company. I am not SEBI registered advsior. I am not recommeding any investment action.

| Subscribe To Our Free Newsletter |