I attended earning call for Embassy REIT Q2FY24. After long time, management sound positive about prospect. They also increased leasing guideance for FY24.

Key positive factors:

Higher operating leverage from hotel business

Increased under construction area coming for completion during FY24 and FY24, signficant portion being pre leased and hence contibuting to cashflow of the company

Expected MTM gain realisation on renewal

Expeced policy decision on SEZ, which would result in higher occupancy for the trust in medium term.

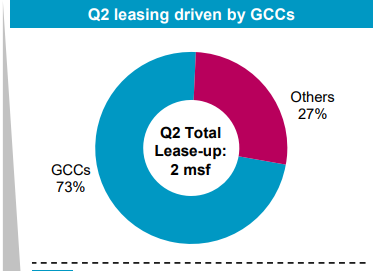

Most important, GCC now being main class of tenants, with nearly 70% of leasing in Q2FY being to GCC clients.

Negatives:

Interest rate increase

Selling by sponsors

While there was no increase in guieance for FY24 distribution, I found management being confident to increase distribution in FY25 onwards. Based on my understnading, I have sold nearly 1/3 of my investment in IndiaGrid and invested in Embassy REIT in last 7 days.

Disclosure: I am not suggesting any investment action. I am not SEBI registered advisor. I have very great track record of being wrong, I was very optimistic about investment during April 2021 period. Embassy price decline from Rs 340 to Rs 300 since then. My view may be positively biased. I may change my investment (increase/decrease/exit) from Embassy REIT without informing members.

| Subscribe To Our Free Newsletter |