Hi @Chins , Great write up on this company.

I have few questions on the numbers: If anyone can help here:

Design led sourcing segment:

Should One think it has happened because of JV turnaround of margins from negative to 4 – 5% margins ? 80 – 300cr pat in last 3 years ? Design led sourcing PBT are sustainable that means this 300cr PAT will be sustainable going forward ?

Coming to Brand Management and SAAS:

Brand Management → As you said it is 250-300CR EBITDA Opportunity.

SAAS → 200 cr PAT Annually.

How this numbers are achievable ?

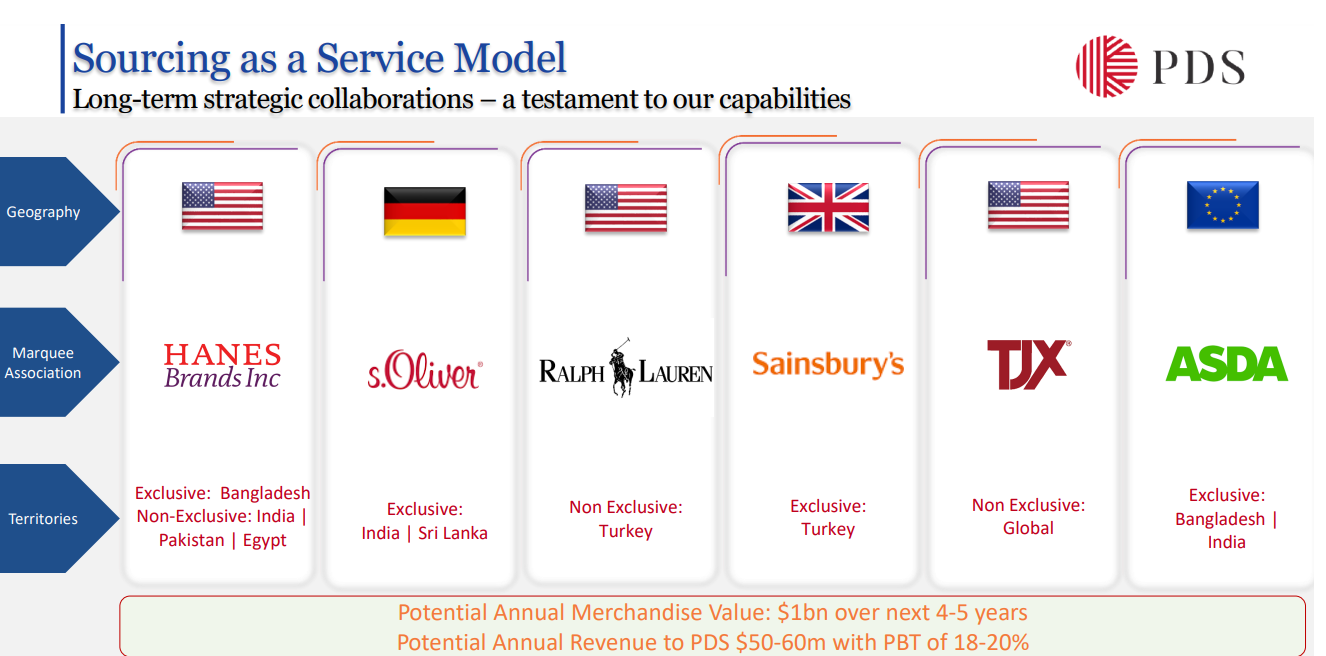

For example: Attaching the below screenshot:

It says potential revenue of 350 – 450cr annually and PBT of 18-20% i.e 70 – 100 CR PBT.

Likewise, on Ted Baker monthly revenue is shown below:

Roughly if I take up monthly 50-60cr so annually it comes around: 350-400cr.

and PBT as – 35cr.

Based on current deals: SAAS and Ted baker deal ~ New offerings it is on annualised basis PBT of => 35 + 70cr => 100cr – 120cr PBT Annually.

Above are for Fy24/25/26 annually for current order wins.

For long term horizon: (Not looking on QoQ)

On 500cr-1000cr PAT in next 3 to 5 years.

According to me, this can be achieved with more deals. Current deals won’t make them achieve 1000cr PAT and their top 10 verticals needs to be scaled up. That needs to be seen. (More revenue from poetic gem etc…)

Huge respect for Pallak to create PDS like platform. His journey has been inspiring. Looking forward as Pallak said, company is at inflection point.

Below snapshot:

Thanks for writing the thread @Chins Your work on this has been amazing !!!

Anywhere my understanding needs to be corrected. Do correct me.

Thanks.

| Subscribe To Our Free Newsletter |