Hi,

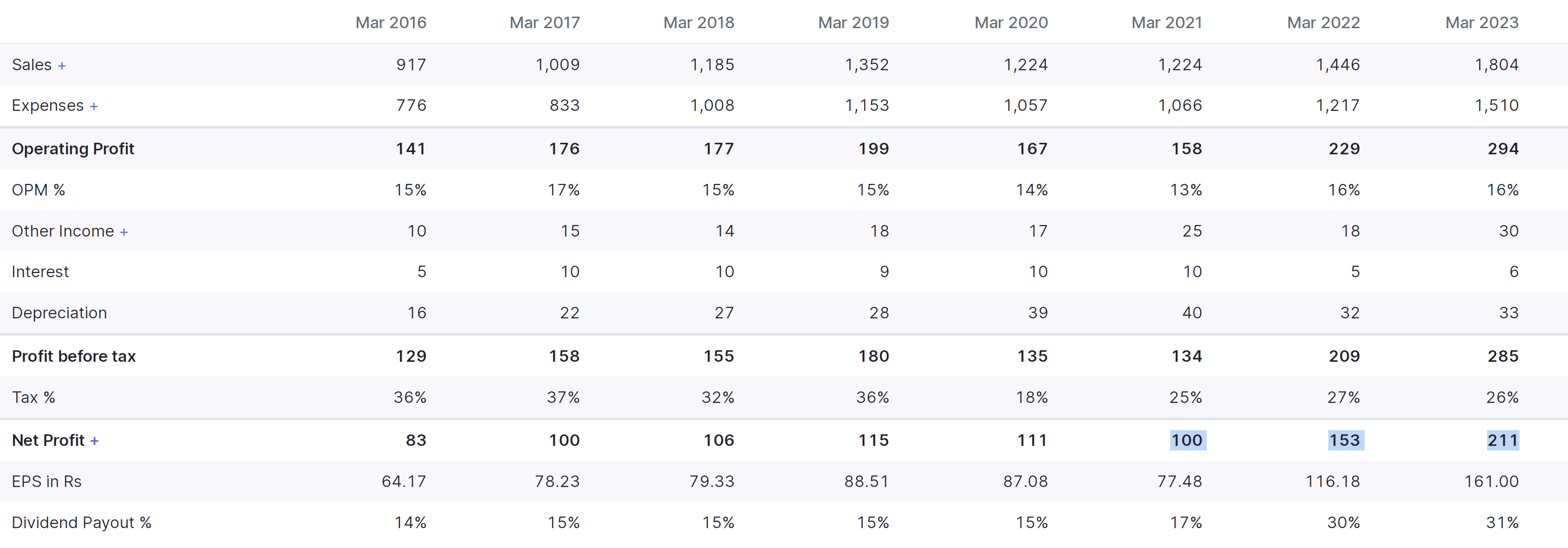

Thank you for seeking my views, I first bought Cera in 2019 because I had a view that residential real estate had bottomed out in India, and Cera was (and is still) one the most well managed building materials company. At that point, it was trading around 28x PE, which optically wasn’t cheap but they were one of the few companies which had grown sales and profits during the downturn.

I ended up selling in 2021 because I was not comfortable with the valuations at which it was trading (~58x trailing PE).

After selling, Cera’s profits more than doubled which suggests that in 2021, there were smarter participants than me who could foresee such a strong growth in profits, which is why it was trading at such multiples in the first place.

The most interesting thing which happened in Cera was they reported increasing margins during the commodity upturn in 2022, when most building material companies suffered. This was because Cera’s price increase was easily accepted by the market, and growth came back in their more profitable segments (sanitaryware, faucetware). Management had guided doubling sales (from FY22 levels) by 2025, which is probably why company continues enjoying higher valuations. However for me, I prefer buying real estate companies (or other building material cos like Stylam) which are exposed to similar tailwinds but are available at much much cheaper valuations. Apart from valuations, I don’t have any other concern w.r.t Cera. I have also attached my notes from FY23 below.

FY23Q1

- Hope to double topline in 40 months

- Cash has increased to 566 cr

- Volume growth ~ 10-15%

- Annual EBITDA margin should be 17-19%

FY23Q2

- H2 generally is 55% of annual revenues, confident of growing over 1600 cr. in FY23

- EBITDA margin guidance is for 15%+

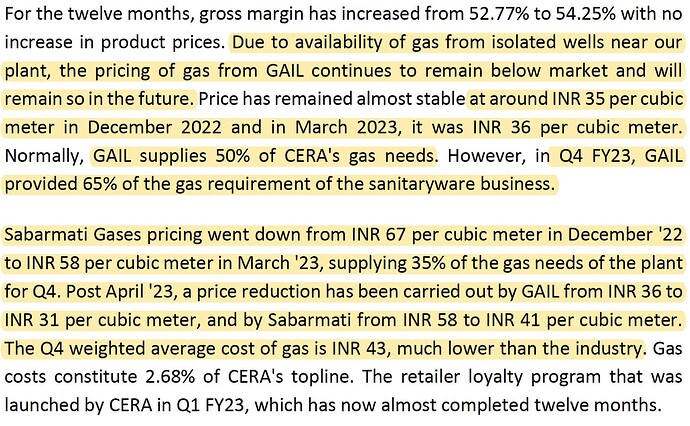

- Gail gas cost price has gone to 33/m3 in October 2022. Average cost in Q2 was 25.7/m3 from GAIL (54% of requirement) and 74.87/m3 for the remainder (Sabarmati gas)

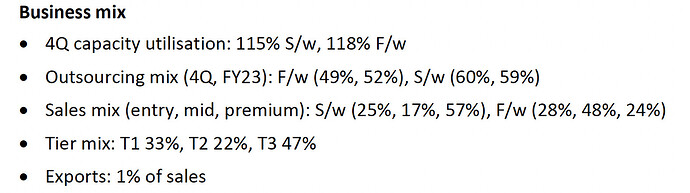

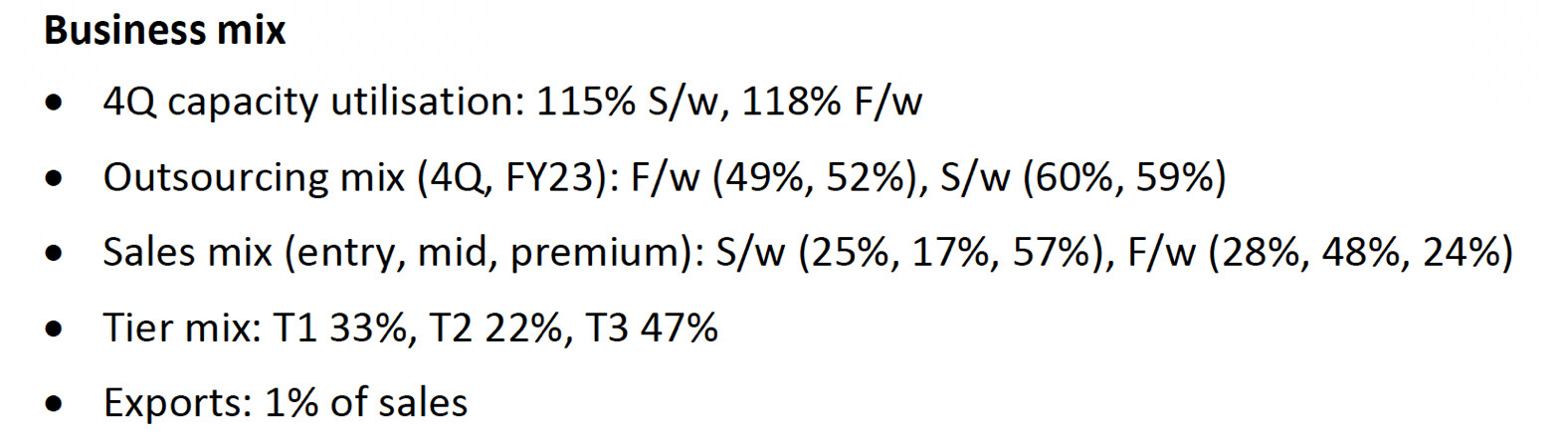

FY23Q4

- Industry grew at 6-7% vs Cera’s growth of 22% (both in sanitaryware and faucetware)

- Target: 2900 cr. revenues by September 2025

- Didn’t have to take price increase since May 2022 because of better cost efficiencies

- Rolled out new ad campaign (increased from 34-35 cr. To 57 cr.). Ad spends will remain at 4-4.5% of sales

- Largest co in sanitaryware and second largest in faucetware

- Dealers in March ’22 were 4,260 which in March’23 had become 5,462. And the retailers were around 11,300, which are now around 14,600.

- Looking to improve EBITDA margins by 75 bps in FY24

- Brownfield faucetware expansion ~ 69 cr. (capacity will increase to 48 lakh units by FY24)

- Greenfield sanitaryware expansion ~ 129 cr. (land purchase is 25 cr.)

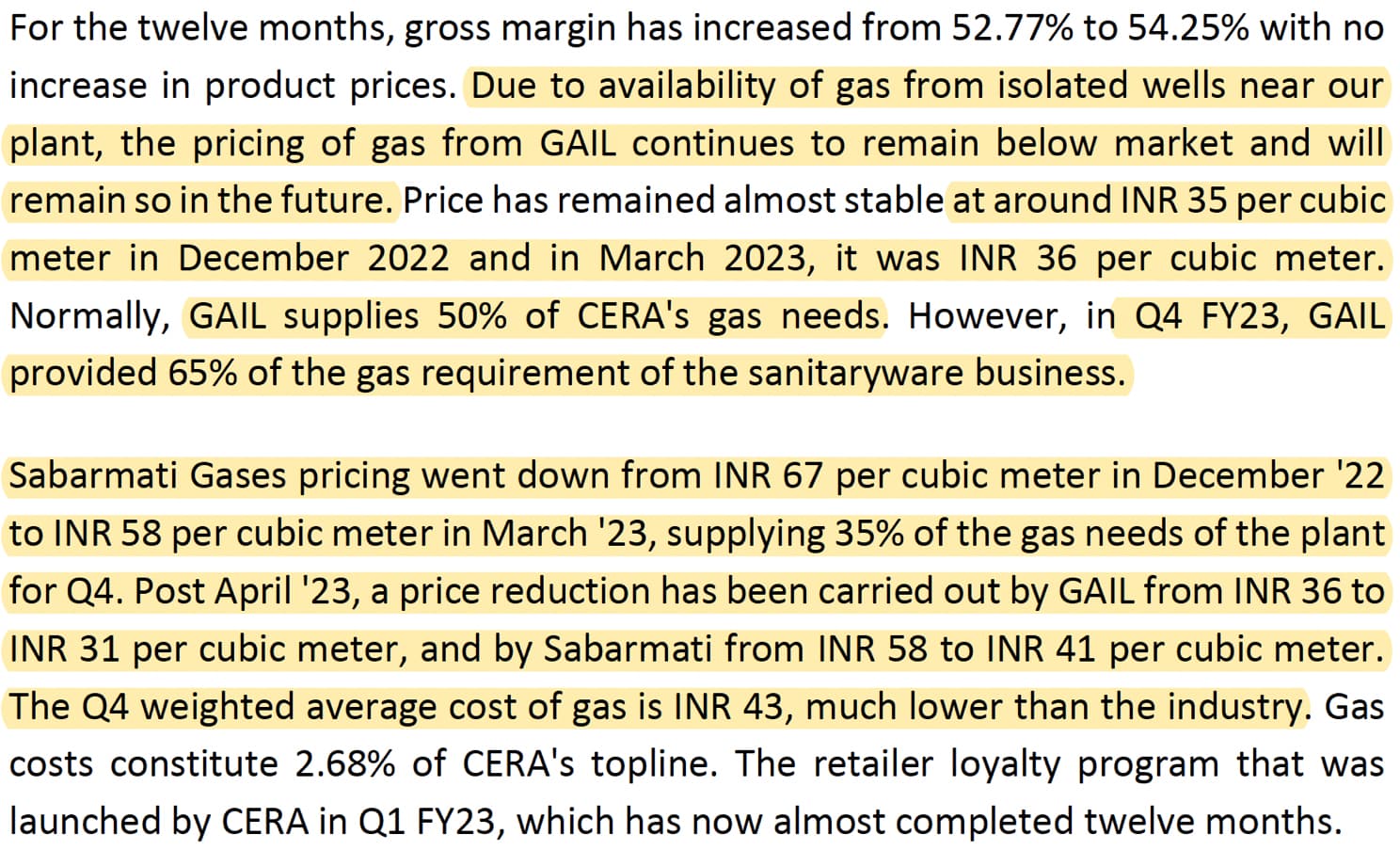

- Gas costs

Disclosure: Not invested in Cera (no transactions in last-30 days)

| Subscribe To Our Free Newsletter |