Indo Count Industries Limited: Record-Breaking Q2 FY24 Performance

Key Financial Highlights:

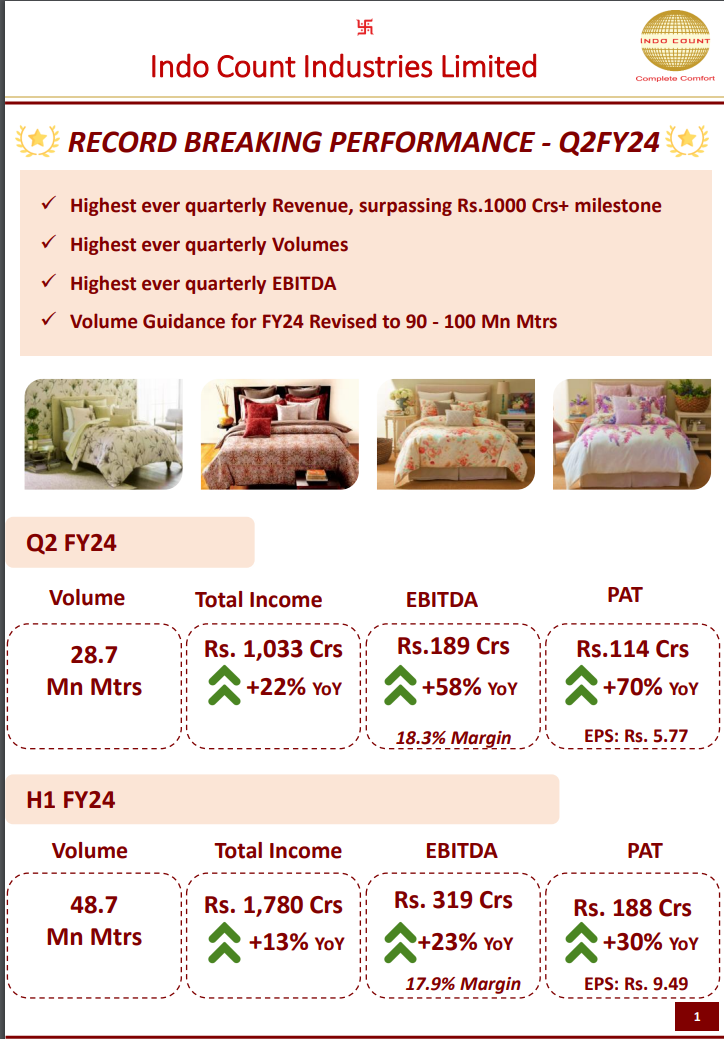

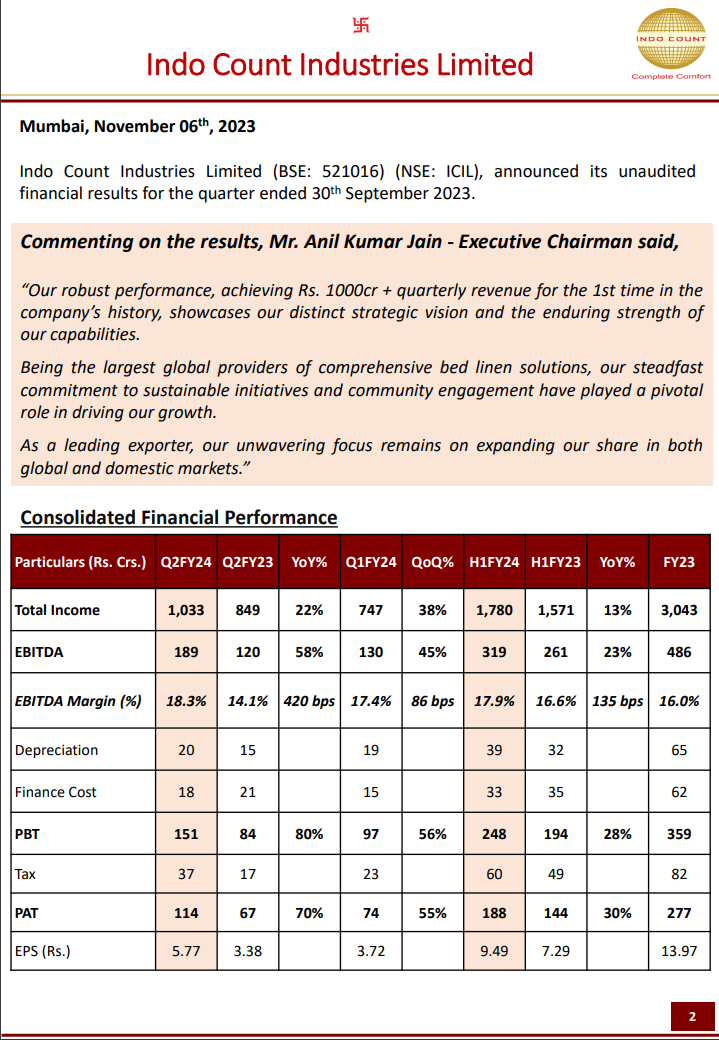

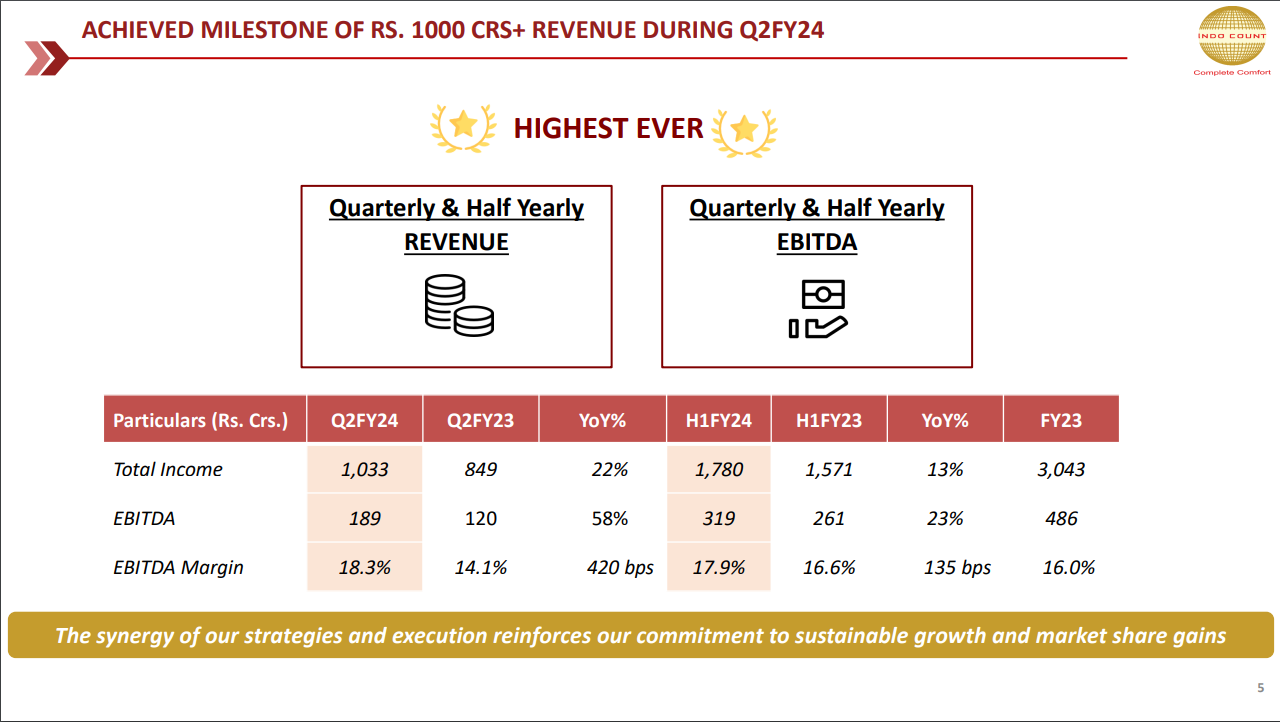

- Total Income (Q2 FY24): Rs. 1,780 Crs, +13% YoY; (H1 FY24): Rs. 1,033 Crs, +22% YoY.

- EBITDA (Q2 FY24): Rs. 319 Crs, +23% YoY; (H1 FY24): Rs. 114 Crs, +58% YoY.

- PAT (Q2 FY24): Rs. 188 Crs, +30% YoY; (H1 FY24): Rs. 74 Crs, +70% YoY.

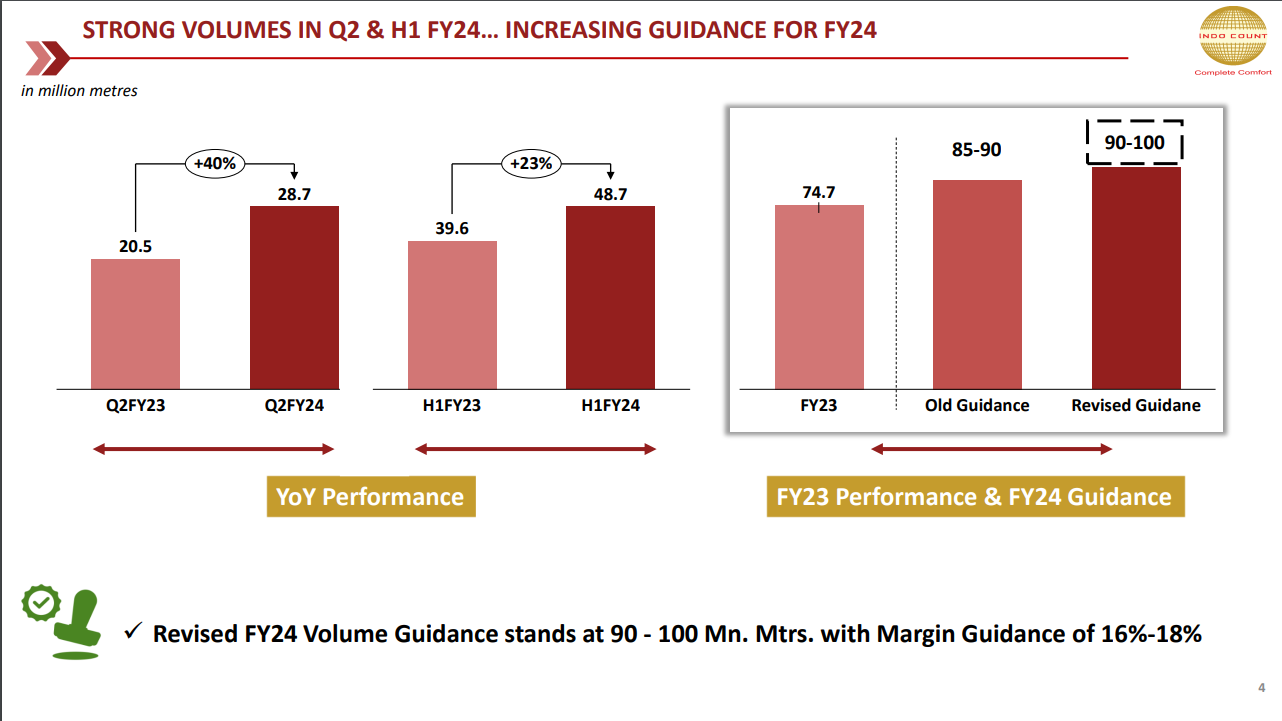

- Volume (Q2 FY24): 28.7 Mn Mtrs; (H1 FY24): 48.7 Mn Mtrs.

- EBITDA Margin (Q2 FY24): 18.3%, +420 bps YoY; (H1 FY24): 17.9%, +135 bps YoY.

- EPS (Q2 FY24): Rs. 5.77; (H1 FY24): Rs. 9.49.

Consolidated Balance Sheet (as of 30th Sept 23):

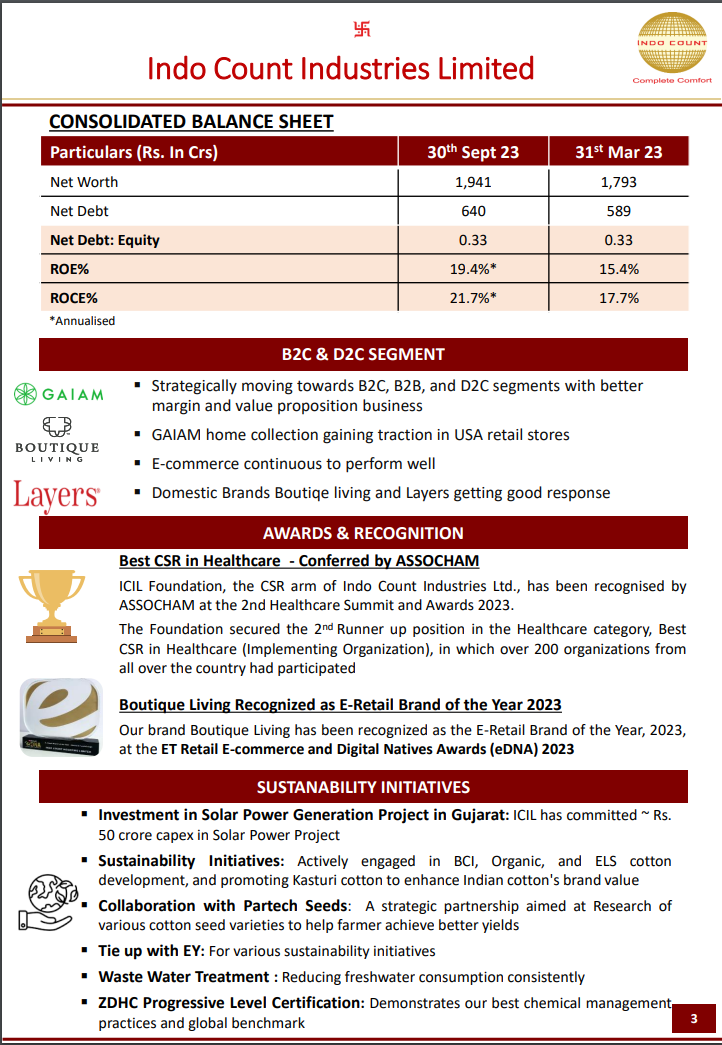

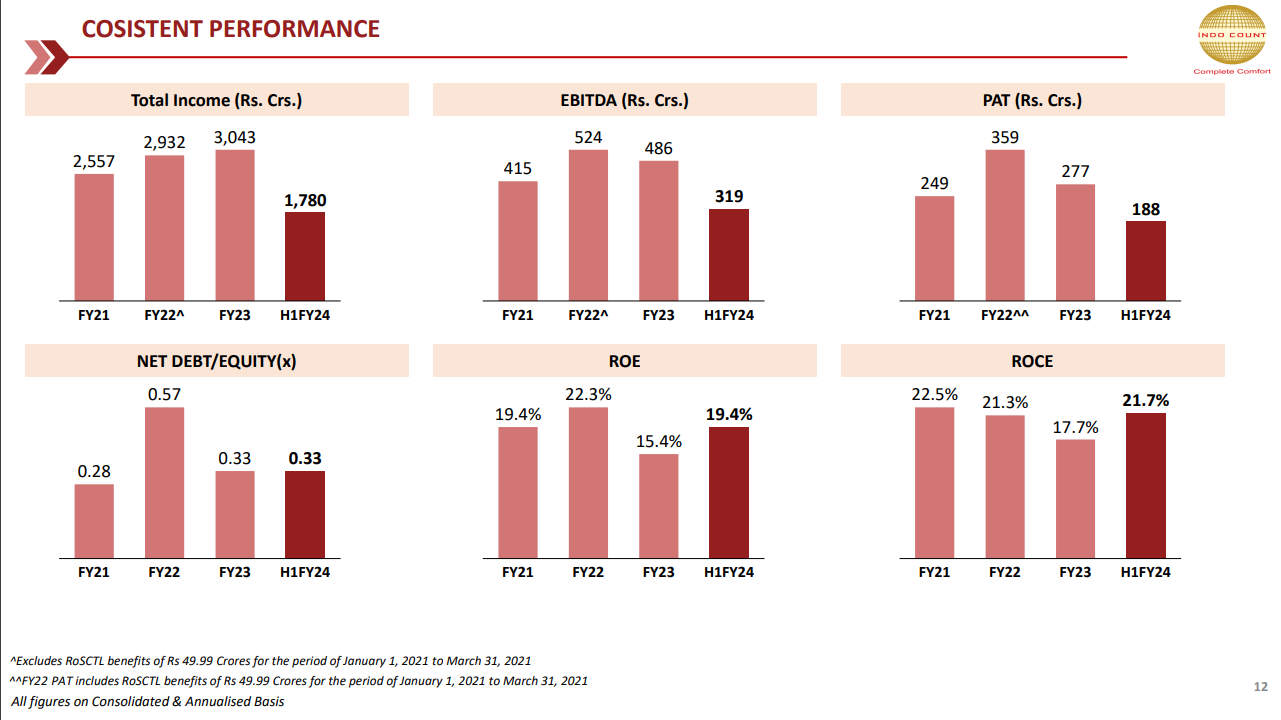

- Net Worth: Rs. 1,941 Crs.

- Net Debt: Rs. 640 Crs.

- Net Debt: Equity: 0.33.

- ROE: 19.4% (Annualized).

- ROCE: 21.7% (Annualized).

Strategic Initiatives:

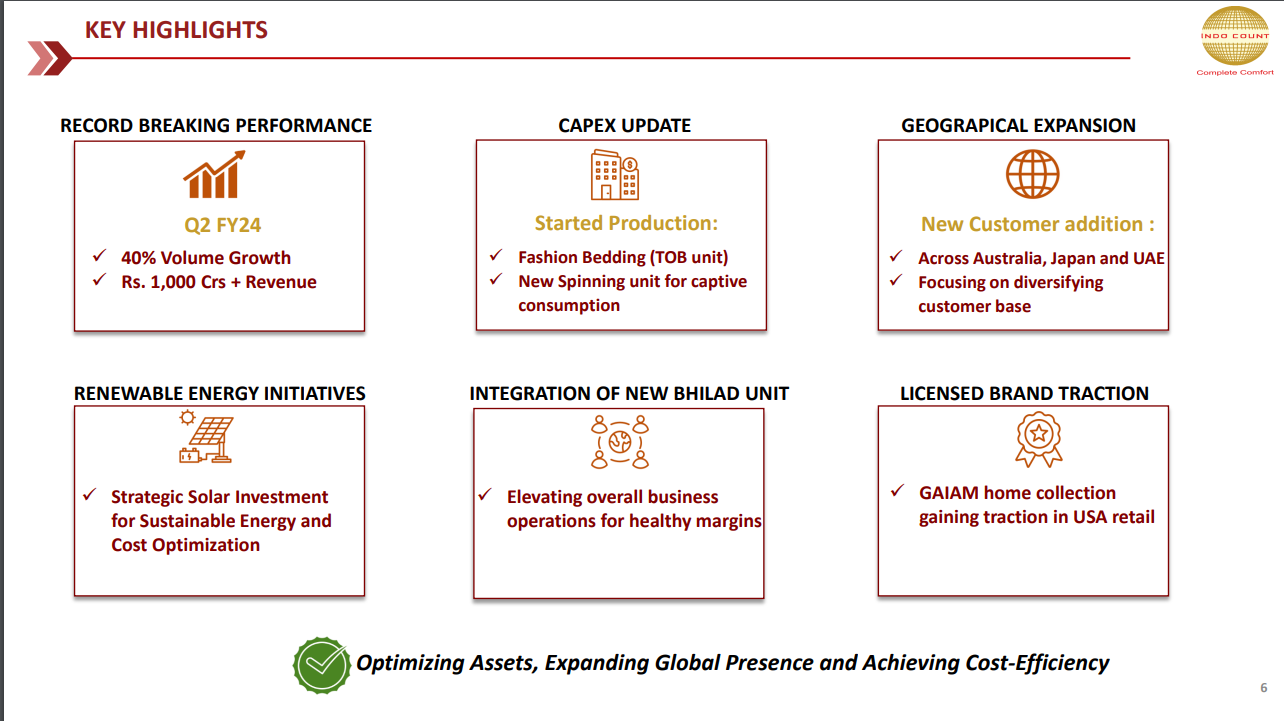

- Record-Breaking Performance: Achieved highest-ever quarterly Revenue, Volumes, and EBITDA, surpassing Rs.1000 Crs+ milestone.

- Volume Guidance for FY24: Revised to 90 – 100 Mn Mtrs.

- Strategic Vision: Mr. Anil Kumar Jain, Executive Chairman, highlights the distinct strategic vision and enduring strength of capabilities, achieving Rs. 1000 Cr+ quarterly revenue for the first time in the company’s history.

- Global Leadership: Being the largest global providers of comprehensive bed linen solutions, with a focus on sustainable initiatives and community engagement.

- Market Expansion: Unwavering focus on expanding market share in both global and domestic markets.

Segmental Highlights:

- B2C & D2C Segments: Strategically moving towards B2C, B2B, and D2C segments with a focus on better margin and value proposition business.

- Global Recognition: GAIAM home collection gaining traction in USA retail stores. Recognition of Domestic Brands Boutique Living and Layers.

| Subscribe To Our Free Newsletter |