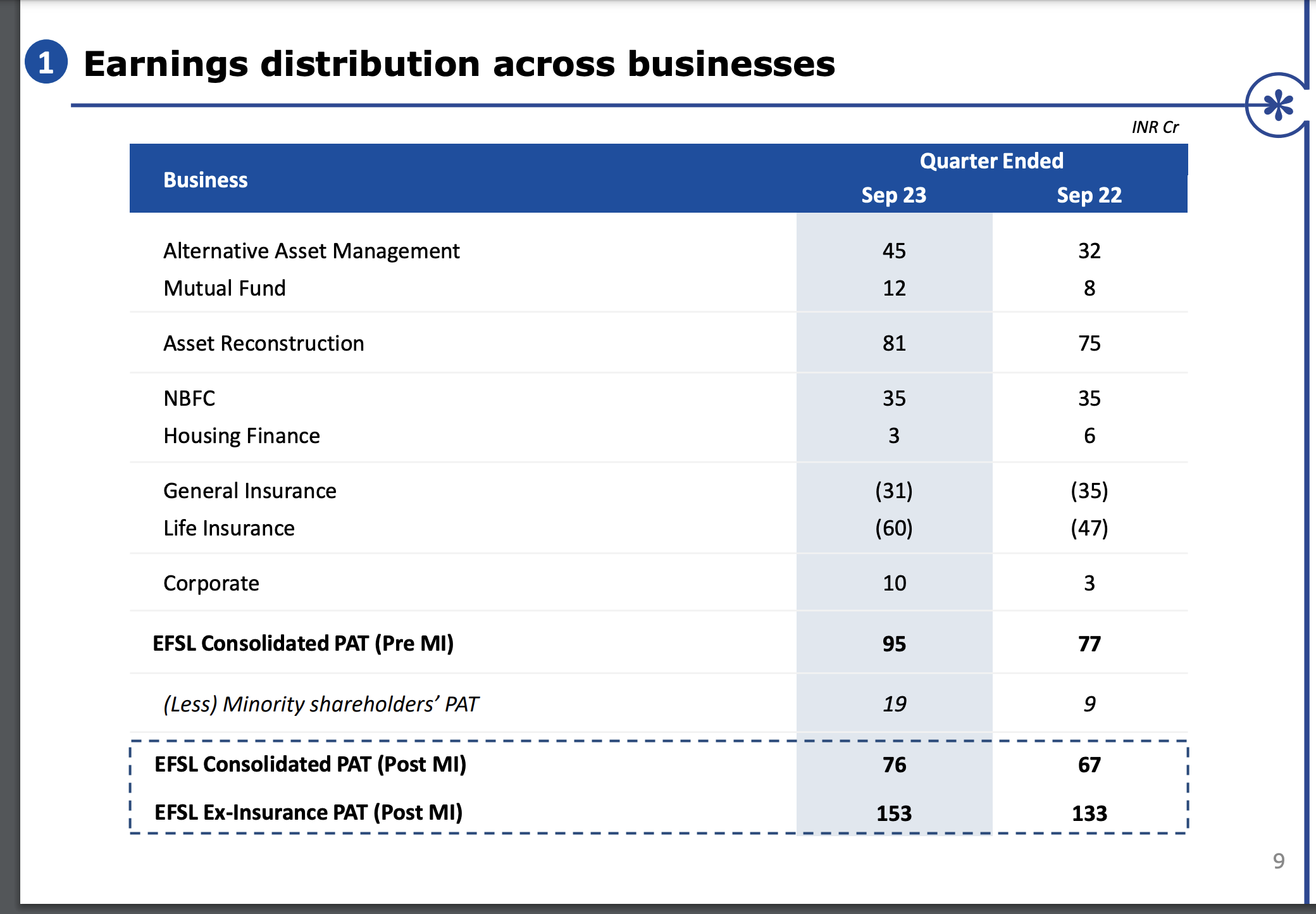

Edel reported decent Q2. Although the reported numbers does not seems different, but things are falling into place for Edelweiss after a long and brutal few years.

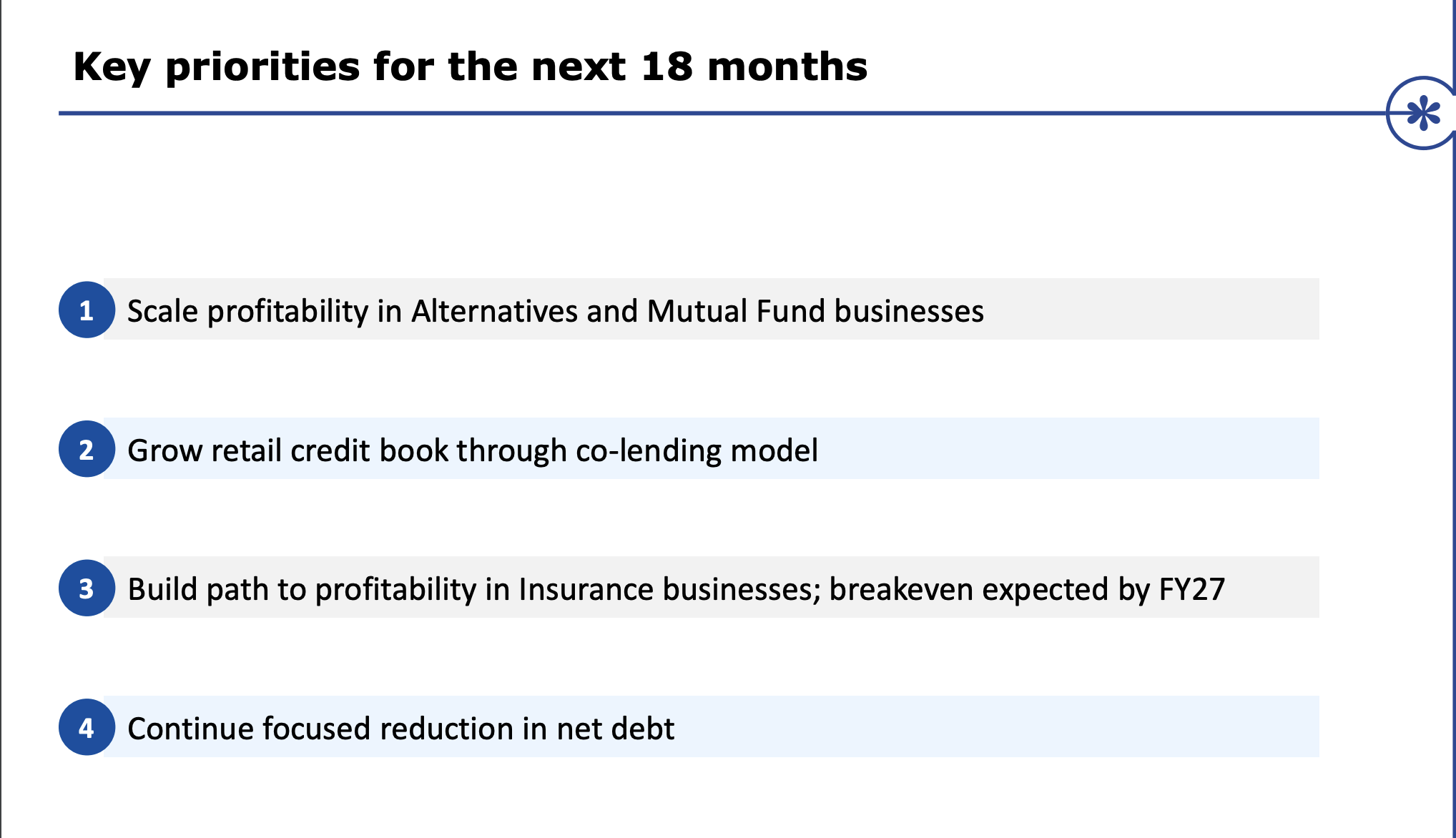

They have listed down key priorities and finally wholesale reduction is becoming less of a priority and other factors they will drive profitability seems to become more priority.

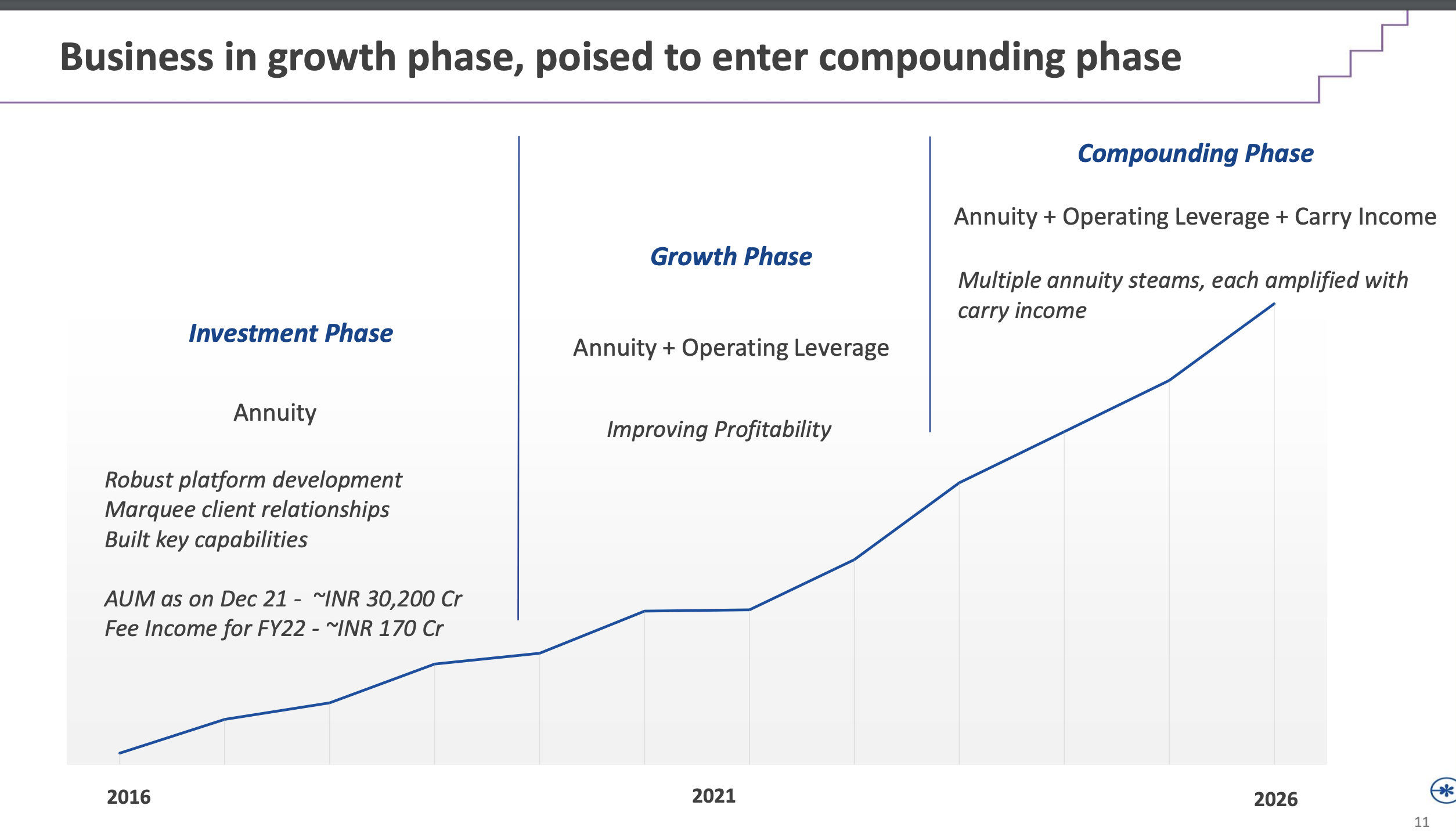

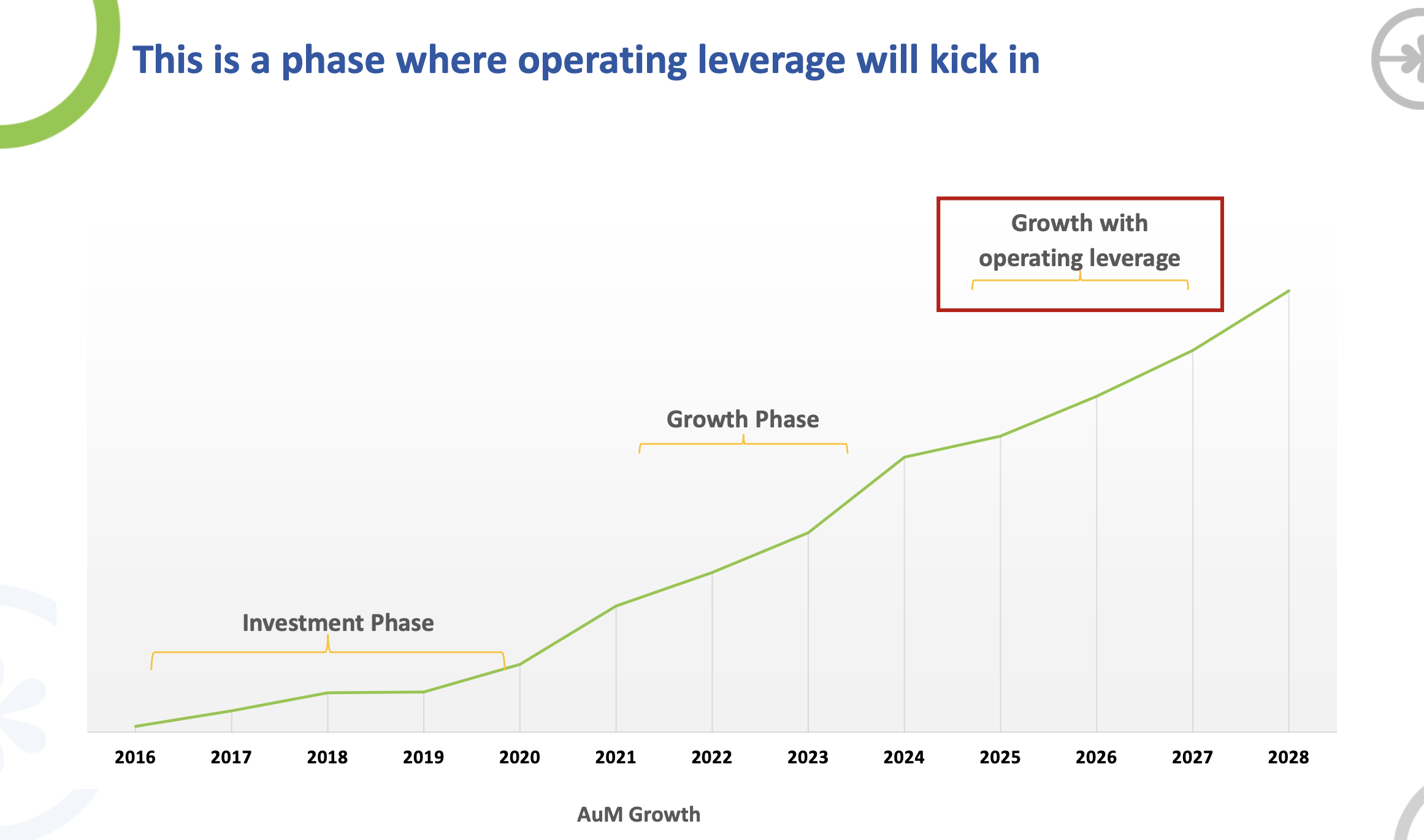

AIF is ready to take off, as they said in 2021/22.

In Q2 FY24

H1 PAT is around 70/80 cr, annualised to 150 to 170 cr PAT for Fy24. Their fee-based AUM of 27,000 cr is the same as committed capital in FY20/21.

This means they have doubled the deployed AUM (from 15 to 27,000 cr) in the last three years. Additionally, their earlier deployed funds are in good standing, boosting their carry income.

I won’t be surprised if AIF’s business profitability at least doubles in the next 3 years, and it could easily be in the range of 300-500 cr once the carry income becomes regular.

They are talking about profitable growth for MF business for the first time. This business is also sitting on operating leverage. Their SIP portfolio of 175 cr per month is quite handy. With the MF CEO joining Shark Tank as one of the investors, she will likely attract more attention to Edelweiss MF. Also, they are openly talking about improved profitability in the future, which is good.

From a PAT of 20Cr, it has the potential to improve towards 100 PAT in the next 3- 5 years.

IN Credit space, Edel is lining up it ducks after a long delay. ECL finance pioneered Co-Lending, but in the 2/3 years, they struggled to scale the business as other NBFCs forged ahead.

IN Q1, they co-lend 290 cr, and in Q2, they lend more or less the same. Co-lending is a high ROE business where the banks’s equity is not tied up fully, and they earn good revenue with less capital. Also, the lending standard is stringent as banks check/vouch for the credit before taking it on their book. It is good to see that they are talking about co-lending, as it is one of the critical factors. This is what Care published few months back.

Insurance- Looks like they pushed profitability by one more year – FY27

Note; Invested and views are biased.

| Subscribe To Our Free Newsletter |