Hariom Pipe Industries Ltd. (HPIL) has reported its financial performance for the quarter ending September 30, 2023. Here are the key highlights:

Operational Performance:

- HPIL produced 56,552 metric tons (MT) of pipes, which is a 121% increase compared to the previous year.

- Sales amounted to 50,435 MT, a 134% increase year-on-year.

- Notably, sales of Value Added Products (VAP) reached 45,313 MT, marking a substantial 176% YoY growth.

Financial Performance:

- The company generated revenue of INR 30,215.28 lakhs, showing a strong 138% YoY growth.

- Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) stood at INR 3,678.06 lakhs, increasing by 127% YoY.

- The Profit After Tax (PAT) was INR 1,477.62 lakhs, a growth of 59% YoY.

- Total Assets reached INR 85,939.90 lakhs, reflecting a 134% YoY increase.

Details:

- HPIL’s Q2FY24 performance was marked by its highest-ever revenue, volume, and EBITDA figures. The company reported INR 30,215.28 lakhs in revenue, and an EBITDA of INR 3,678.06 lakhs, both indicating substantial YoY growth.

- This improved performance was attributed to the significant increase in sales of Value Added Products (VAP), particularly galvanized pipes (GP/GC) produced at the Perandurai plant in Tamil Nadu.

- VAP sales volume witnessed a remarkable 176% YoY growth and contributed to 96% of total sales.

- Despite the substantial increase in production, HPIL managed to maintain stable power and fuel expenses due to the commissioning of solar power, efficient energy usage, and the installation of a more efficient electric melting furnace.

- The newly commissioned GP plant in Telangana is gradually stabilizing, while the GP/GC plant in Tamil Nadu is progressing according to plan.

- The company is working on expanding its product range by including pipes with thicknesses of 0.4mm and higher, which have strong demand and can command higher prices.

- The company expects its operating cash flow to improve as it continues to stabilize its market, product mix, and supply chain.

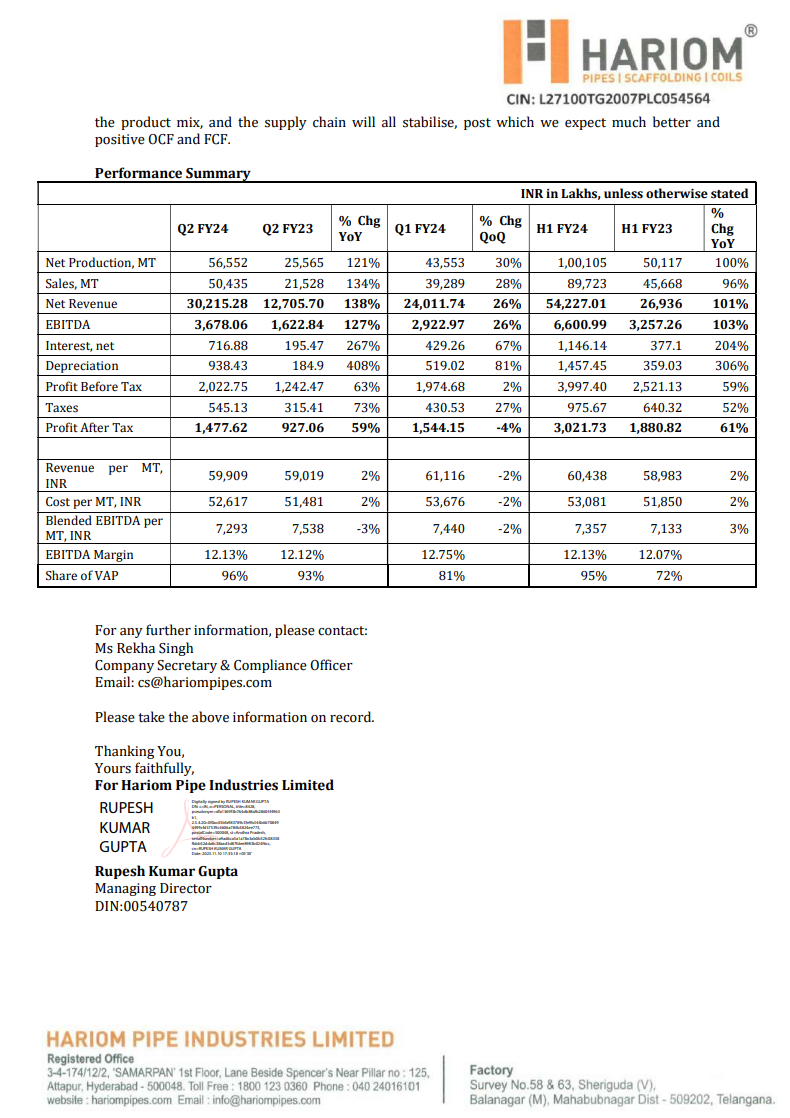

Performance Summary (Q2 FY24):

- Net production increased by 121% YoY to 56,552 MT.

- Sales grew by 134% YoY to 50,435 MT.

- Revenue reached INR 30,215.28 lakhs, up 138% YoY.

- EBITDA was INR 3,678.06 lakhs, reflecting a 127% YoY increase.

- Interest expenses increased by 267%, and depreciation expenses grew by 408%.

- Profit Before Tax (PBT) saw a 63% YoY increase to INR 2,022.75 lakhs.

- The Profit After Tax (PAT) increased by 59% YoY to INR 1,477.62 lakhs.

- EBITDA margin for the quarter was 12.13%.

- The majority of sales (96%) came from Value Added Products.

| Subscribe To Our Free Newsletter |