Technocraft Industries has reported its financial results for the second quarter of the fiscal year 2023-24 (FY24)

Financial Performance (Consolidated) for Q2 FY24:

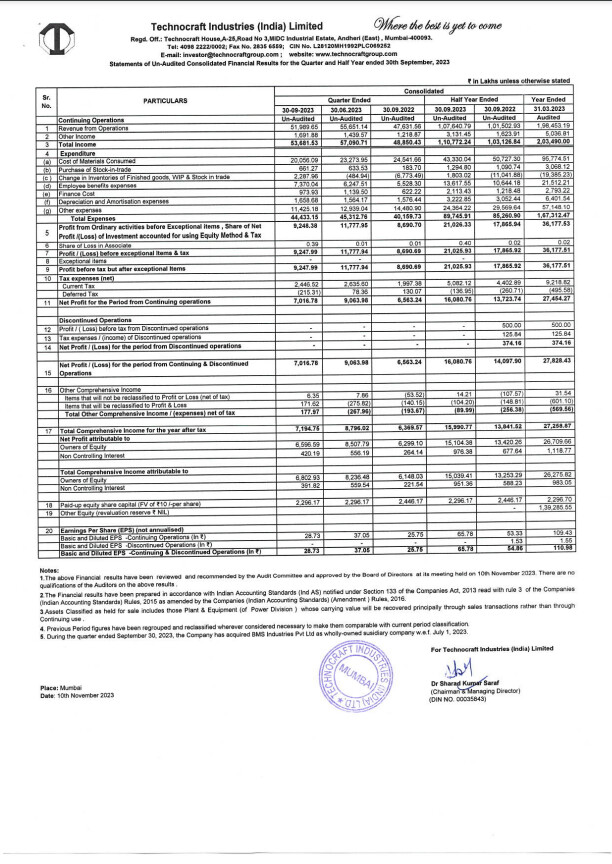

- Revenue from Operations: The company achieved consolidated revenue of ₹520 Crores for Q2 FY24, representing a 9% year-on-year (YoY) increase from ₹476 Crores in the previous year.

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): The consolidated EBITDA for the quarter reached ₹119 Crores, reflecting a 9% YoY growth from ₹109 Crores in the corresponding period of the previous year.

- Profit After Tax (PAT): The consolidated profit after tax stood at ₹70 Crores, indicating a 7% YoY increase from ₹66 Crores in Q2 FY23.

Segmental Highlights (Consolidated) for Q2 FY24:

1. Drum Closure Division:

- Revenue from Operations: This division’s revenue slightly decreased from ₹140 Crores to ₹137 Crores in Q2 FY24, a 2% decline.

- Profit Before Tax and Finance Cost: However, the profit before tax and finance cost, but after depreciation, increased by 18% from ₹41 Crores to ₹48 Crores YoY due to margin improvement.

2. Scaffolding Division:

- Revenue from Operations: The Scaffolding Division experienced a substantial 17% YoY increase in revenue, rising from ₹201 Crores to ₹235 Crores.

- Profit Before Tax and Finance Cost: In contrast, profit before tax and finance cost, but after depreciation, decreased from ₹50 Crores to ₹45 Crores on a YoY basis.

3. Textiles:

- Revenue from Operations: The Textile Division reported a decrease in revenue from ₹133 Crores to ₹120 Crores, primarily due to challenging market conditions.

- Loss Before Tax and Finance Cost: The loss before tax and finance cost, but after depreciation, reduced from ₹15 Crores to ₹9 Crores YoY in the Textile Division.

4. Engineering Services:

- Revenue from Operations: The Engineering Services Division saw a significant 59% YoY increase in revenue, rising from ₹33 Crores to ₹52 Crores.

- Profit Before Tax and Finance Cost: The profit before tax and finance cost, but after depreciation, increased by 38%, growing from ₹9 Crores to ₹13 Crores on a YoY basis.

Key Observations and Outlook:

- Technocraft Industries reported growth in consolidated revenue, EBITDA, and PAT in Q2 FY24 compared to the same period in the previous year.

- The Drum Closure Division saw a profit increase despite a marginal reduction in revenue, attributing the growth to margin improvement.

- The Scaffolding Division, while experiencing increased revenue, faced profit pressure due to geopolitical disturbances affecting volumes.

- The Textile Division witnessed revenue decline due to challenging market conditions, leading to lower profit.

- Engineering Services showed strong growth, with increased revenue and profit, driven by cost restructuring and a global delivery model.

- The company is optimistic about the growth potential in its various divisions and anticipates improved performance in the future.

- Technocraft Industries is actively focusing on expansion, as seen in the setup of a new Aluminium Extrusion and Fabrication plant, with a total project cost of ₹289 Crores.

- The company expects increasing demand for its services in the Engineering Division due to its offshore global delivery model.

| Subscribe To Our Free Newsletter |