My Take on Q2 Results:

Not so WoW Results, but justified a deep look ![]()

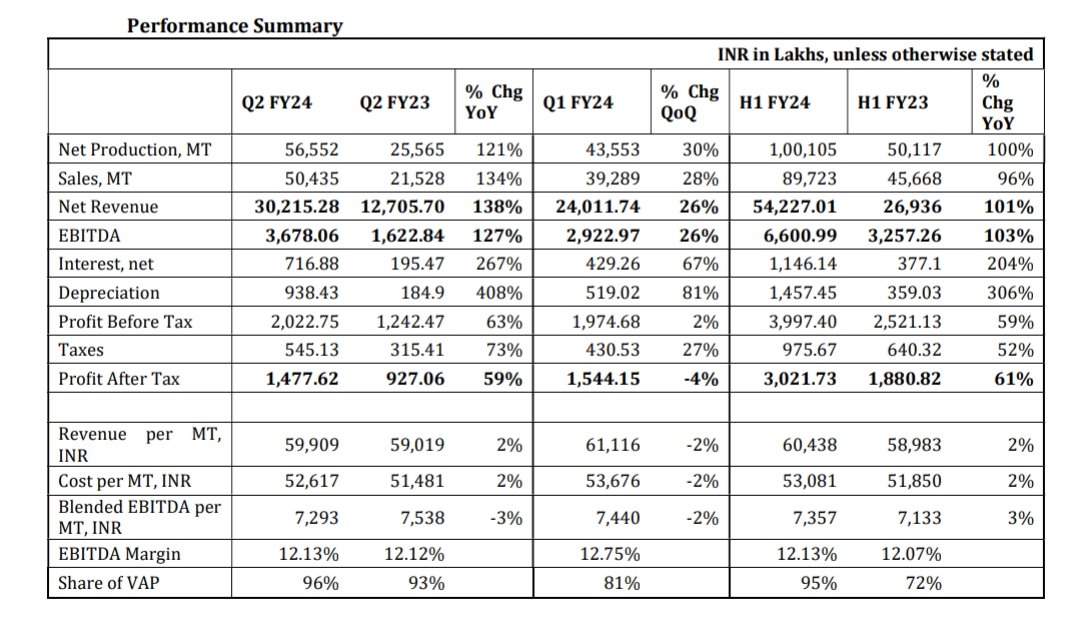

-Revenue up 138% YoY n 26% QoQ

-EBITDA up 127% YoY n 26% QoQ

-EBITDA Margin at 12.17% vs 12.78% YoY vs 12.17% QoQ

-PAT up 59% YoY n -4% QoQ

-OCF weak -60.8 Cr vs -23.8 Cr

Looking weak,

But a deeper look ![]()

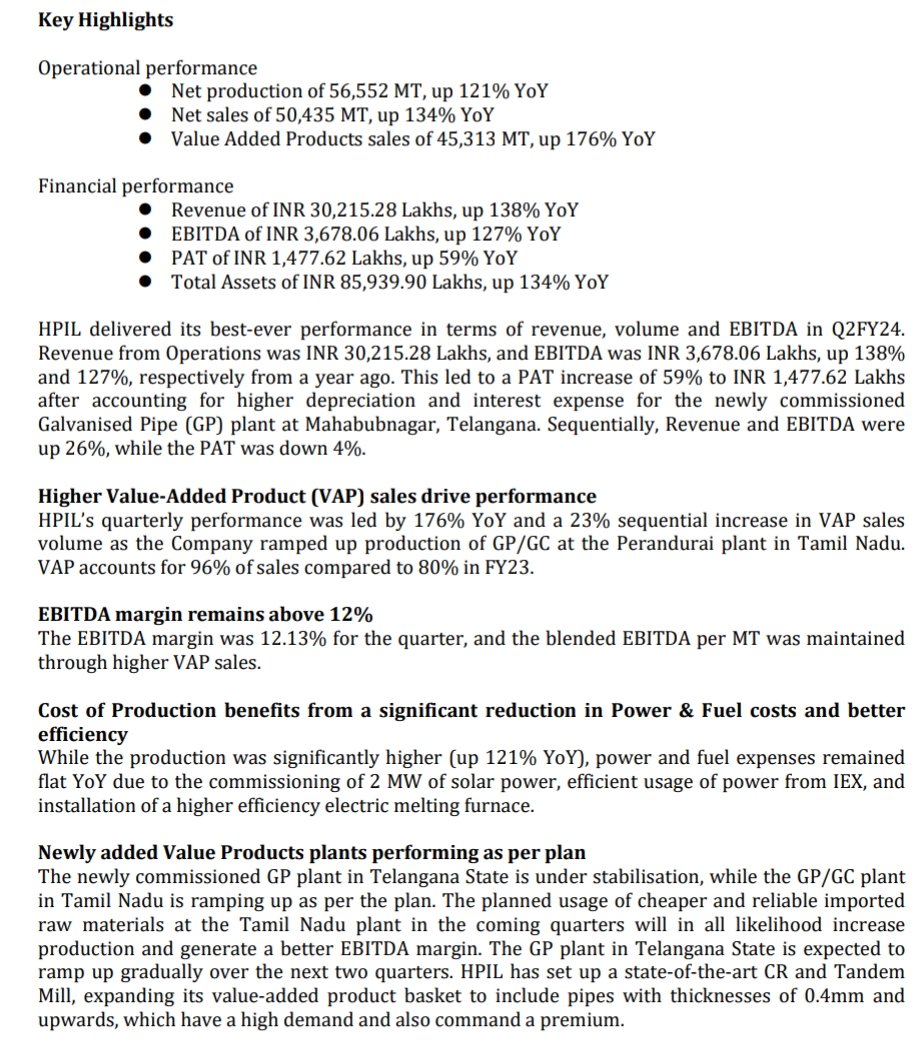

Why PAT Growth lower?

-High Int & Dep Exp (Cauz of Capex)

Why Int Higher?

-Weak OCF (last 1 year -ve CFO)

Interesting things:

-Volume Growth is much higher 134% YoY n 28% QoQ🔥

-Value added share increased to 96% from 93% YoY

-VAP Volume increase by 176% YoY n 23% QoQ

-Realisation Growth is flat (Not selling product at depress price, to show good Revenue Growth)

-Highest ever volume & sales number

-Power & Fuel cost flat, even though FA doubled (cauz of Solar)

-Capex is ramping as per plan

-Will import cheaper RM to expand EBITDA Margin

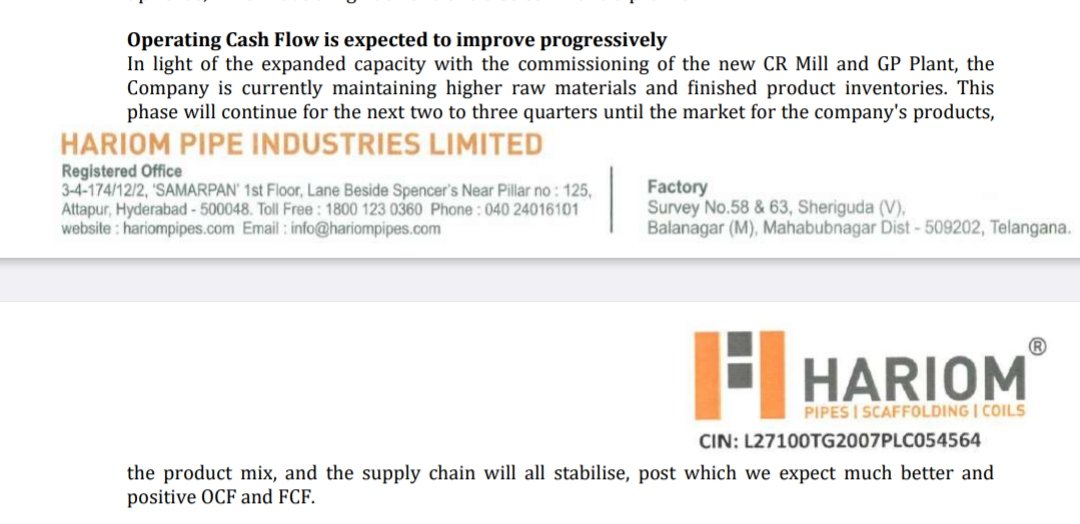

About Weak OCF?

-Hariom is telling us that we need 2-3 Quarters time to improve CFO because of too much Capex, they need to maintain product, product mix & supply chain to stabilize

Weak CFO has led to high borrowings in B/S & high interest exp. impacting PAT

First ever presentation released:

Let’s analyse it:

-

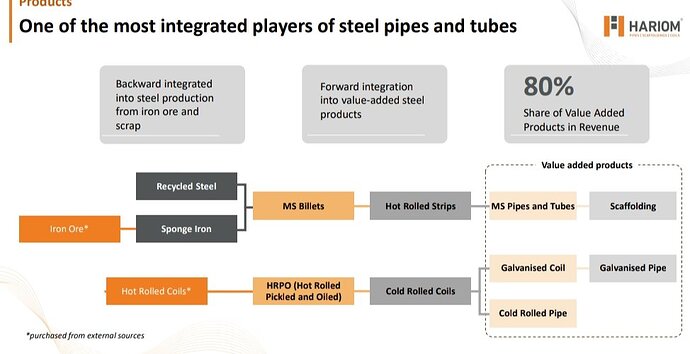

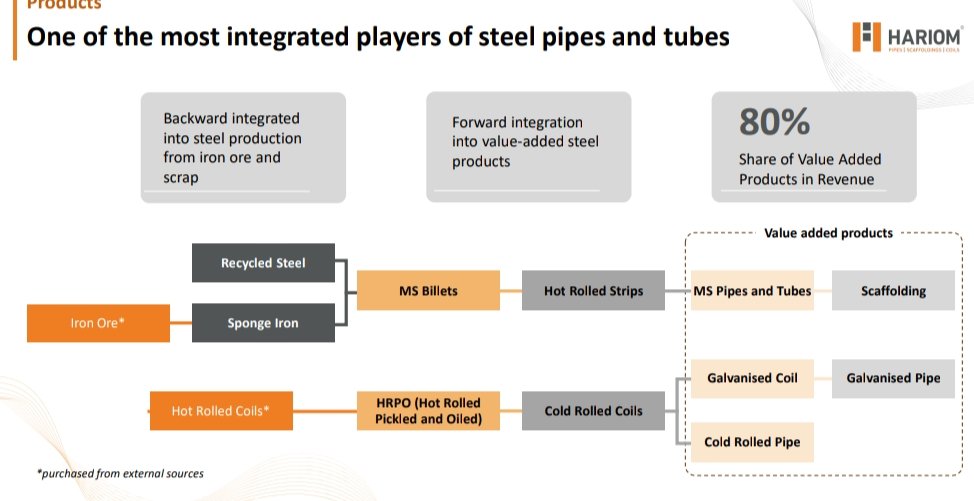

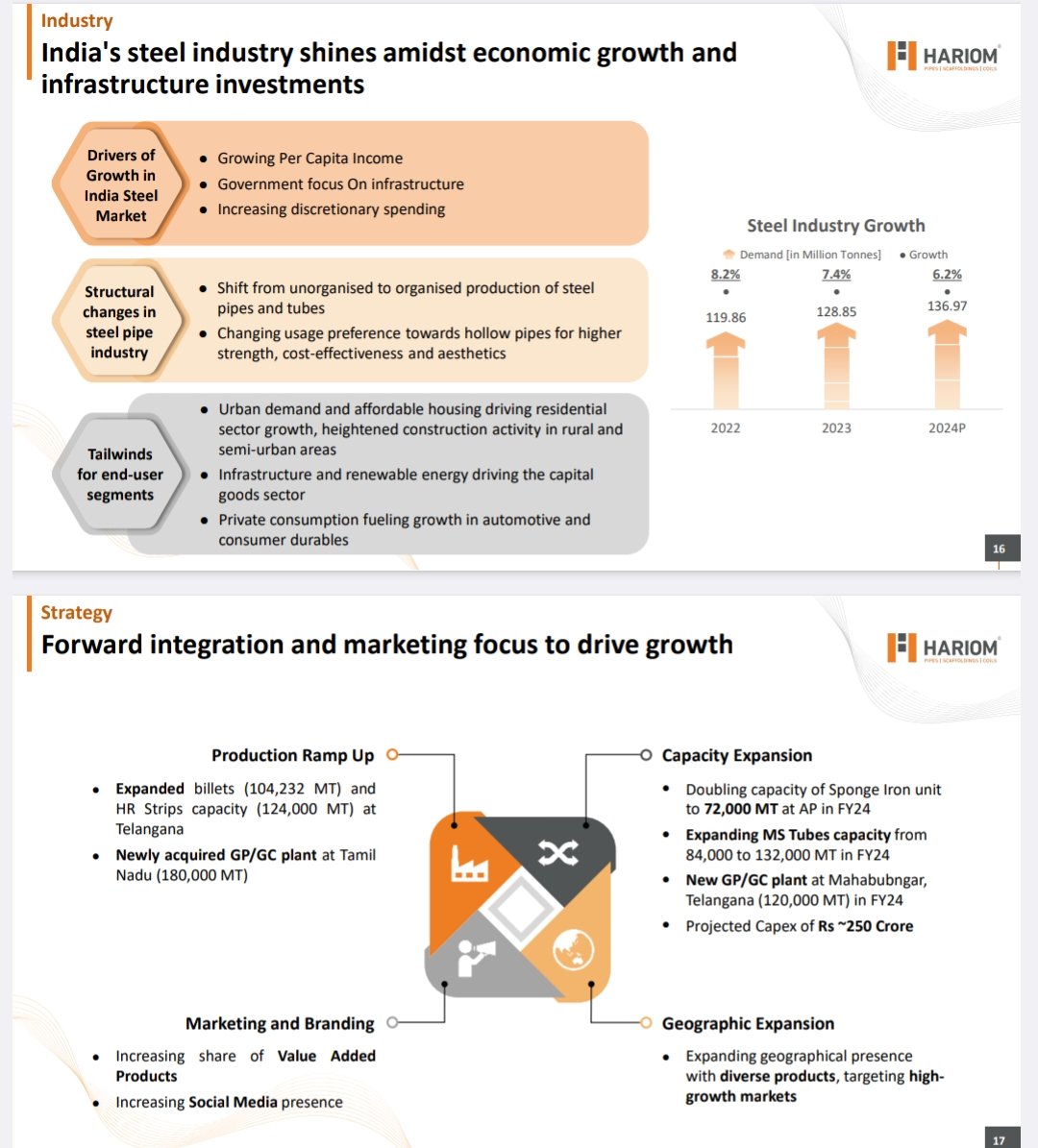

Value Chain

-Backward integrated steel production

-Forward integrated into VAP steel products

-More than 95% VAP sales

-Reason behind high EBITDA Margin compared to other players

-

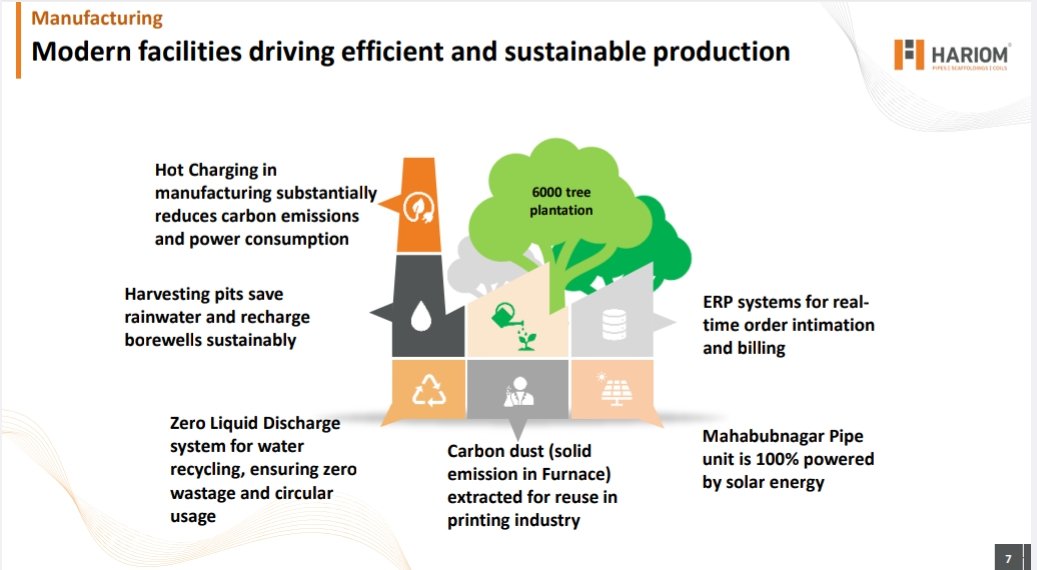

Modern & Sustainable use of technology for production

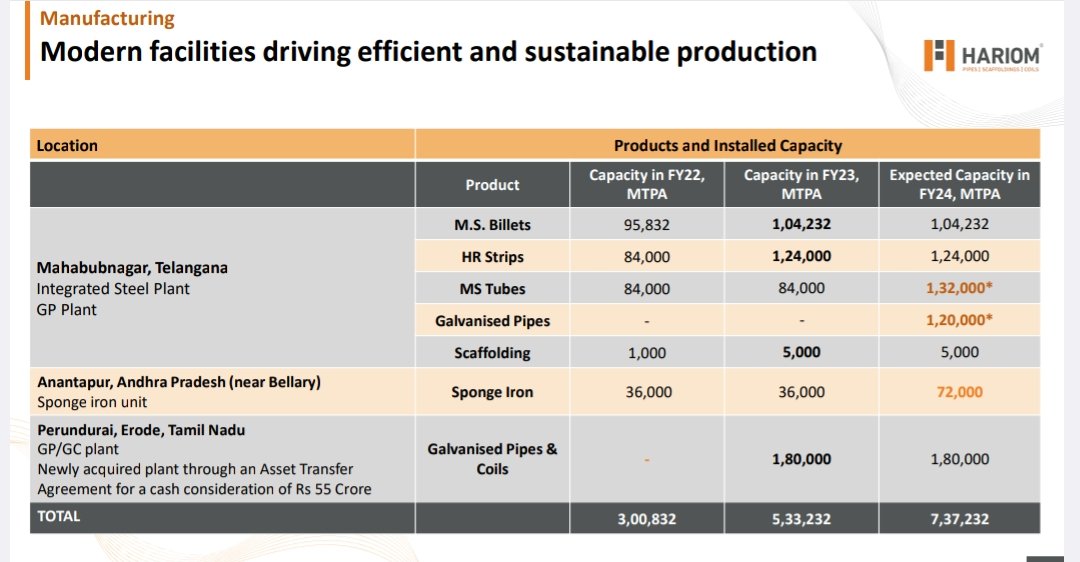

- Production Capacity

-Capacity expanded more than doubled from FY22 base thorough acquisition & capex

Hariom has:

-250+ Product specification

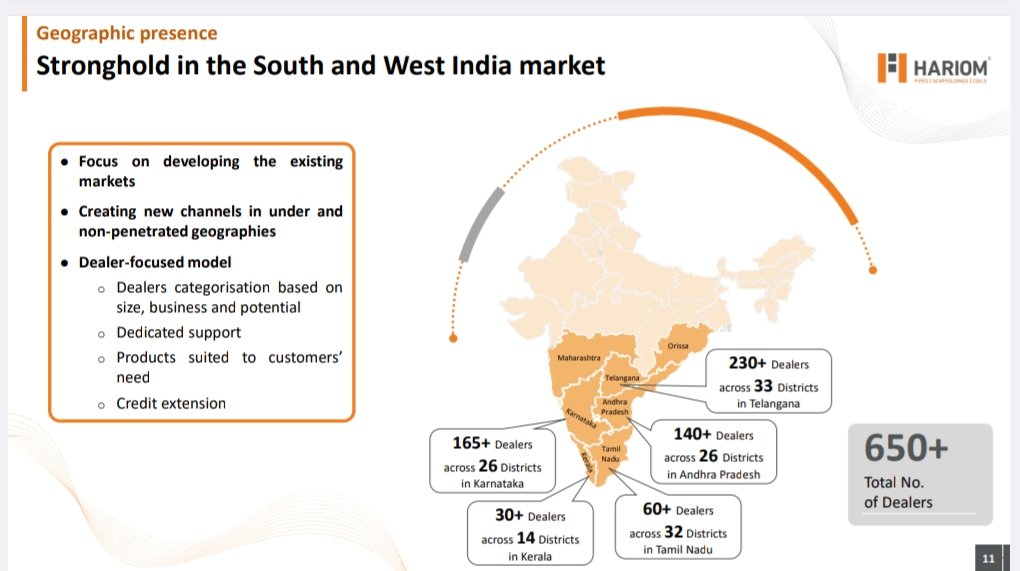

-1500+ Dealer network and POS

-Strong presence in South & West Market

-

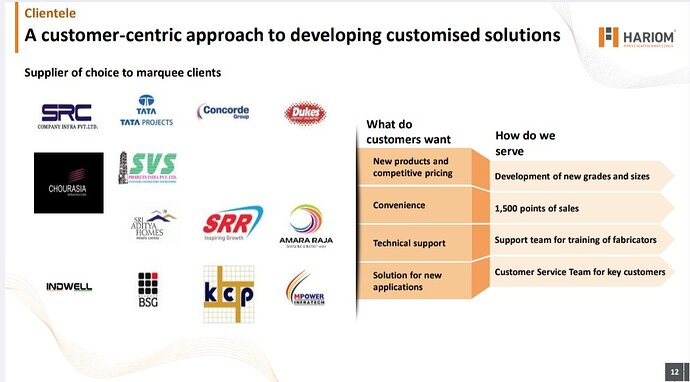

Customers:

-

Guidance:

-Goal to reach 2,500 Cr revenue by FY26

Achieve thorough:

-Improving product portfolio

-Grographical expansion

-Capex led growth

-Marketing & Branding

-Industry tailwinds

My look:

-Results look neutral to average in hindsight as CFO -ve, Borrowing up, no margin expansion, high dep & low pat growth but

Management is saying:

-Wait & give us 2-3 Quarter to stabilize & things will look much better after that

Also, all the long term triggers are intact

-Grographical expansion + Power cost flat + VAP mix improving + Industry cycle + sales growth + importing RM to improve GP Margin

All good… will wait & give time to Hariom to show their true growth…

No Recommendation

| Subscribe To Our Free Newsletter |