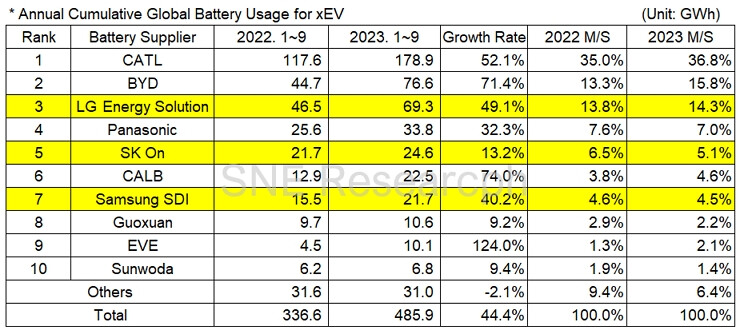

Key Players in Lithium-Ion Cell Space

Lithium-Ion Cell Space is dominated by Chinese and South Korean Players.

CATL (China); BYD (China); LG Energy Solutions (South Korea); Panasonic (Japan); SK Innovation (SK On) (South Korea); CALB (China); Samsung SDI (South Korea); Gotion (Guoxuan) (China); EVE Energy (China); Sunwoda (China)

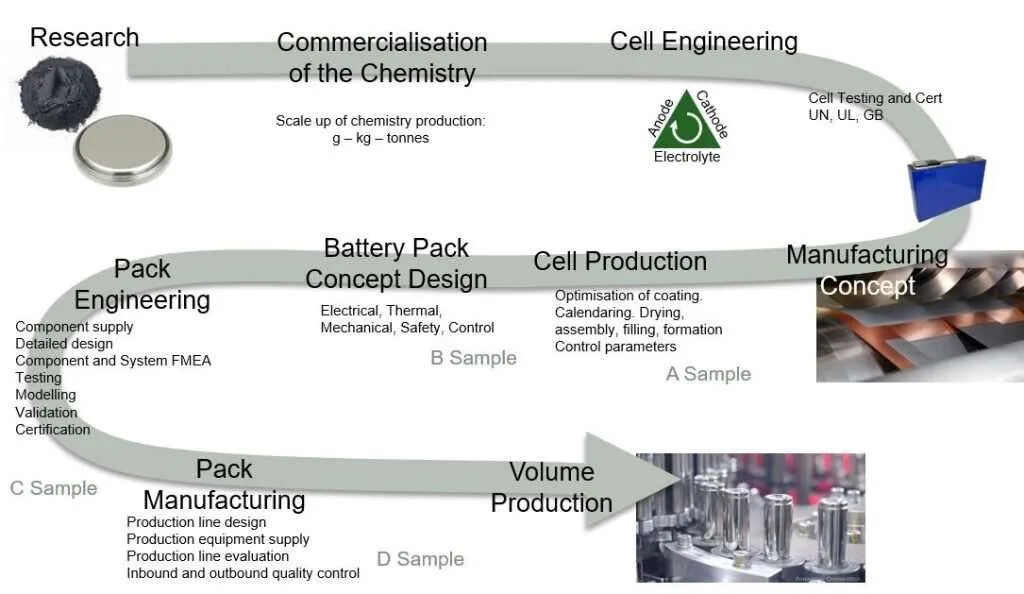

Cell Development process – A sample to D Sample

- A Sample and B Sample can be produced from Manufacturer’s Pilot Plant facility

- C and D samples have to be produced from the actual production line

- The timeline is typically 6-12 months to move from one Sample to next before being qualified by the Auto OEM.

- It is a long and tedious process.

Things to Note

Lithium-Ion Cell GigaFactories are very tough to scale up

- Even Panasonic with several decades of experience in batteries space, including in lithium-ion batteries struggled to scale up their first large scale gigafactory in Nevada US

- Panasonic Started Construction for the factory in January 2015, with Production starting in January 2017.

- Panasonic first achieved profitability from their Nevada plant in 2021.

- Basically, it took them 4 years to reach the desired scale and yield from the Plant. Note that this is the plant that supplies Tesla.

- There are more such examples. SK Innovation’s Battery business is yet to break even. They are operating since 2017. Again this is mainly due to plant yield issues.

- Scaling/Ramping up the plant to optimum level of capacity is tough.

- The Batteries have to go through stringent quality checks as there are safety issues to monitor. A small defect can lead to fires and huge provisions. (for example look at LG Energy Solutions and GM’s Bolt recall issue)

Also, there have not been many new entrants/Start-ups in the Cell space. There are so few that we can list them out:

- New Entrants in Europe – Northvolt, Verkor, Freyr, Morrow (None of them have started production yet)

- New Entrants in North America – Our Next Energy, Quantumscape, Solid Power (Again none of them have started production)

China has huge edge with them being highly capital efficient (wth Government Incentives)

The Chinese companies are most efficient helped by Government incentives. Capital Intensity for Chinese companies especially leaders like CATL is $35-$50m/GWh of capacity in China. In US, Europe Capital intensity is more the 2x. US plants >100m/GWh (for examples look at any of the recent announcements by Lg Energy Solutions/ SK Innovation in US). For Amara Raja too Capital Intensity is around $71m/GWh using current exchange rates.

What this does is Chinese companies keep building capacity even without firm contracts in place. They operate at much lower plant utilisations. Being cost competitive with Chinese players globally is tough.

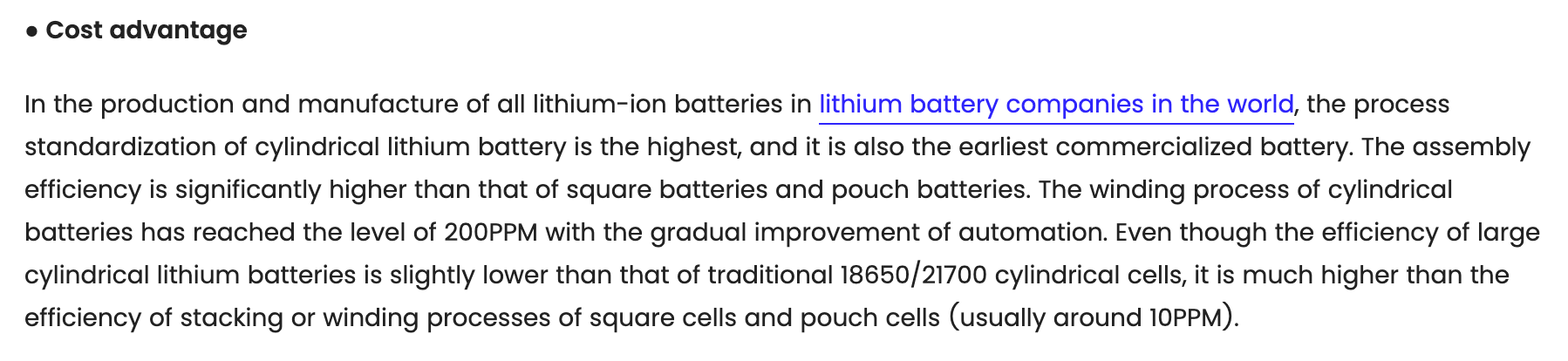

Why ARE&M’s Decision to go for Cylindrical Batteries 21700 format is good

- Basically Cylindrical Cells/Batteries are easier to mass produce compared to other forms (pouch and Prismatic) See below

Car OEM’s and their Partners

In-House Cell Manufacturing

- Tesla

- BYD

- VW (Through PowerCo Subsidiary)

Other Large OEM’s

- Mercedes – No in-house manufacturing

- Stellantis – JV plants with Samsung SDI and LGES (so partially in-house)

- BMW – No in house manufacturing – Long Term contacts with – CATL, EVE Energy, AESC, Northvolt (confirmed), SVOLT (Rumoured)

- GM – JV with LGES (Ultium) and Samsung SDI (so partially in-house)

- Ford – JV with SK Innovation (so partially in-house)

- Hyundai – JV with LGES and SK Innovation (so partially in-house)

- Toyota – Are building their own plants and have JV with Panasonic called Prime Planet Energy Solutions (partially in-house). Has contracts with LGES too

For India

- Tata – Has plans for in-house manufacturing, currently key partner is China’s Gotion

- Mahindra – Not aware of in-house manufacturing plans. Currently key partner is LGES

- Hyundai – Key partners are SK Innovation and LGES

Challenges for ARE&M

-

Scaling up is a challenge

-

Technology challenge – Already companies are moving to 46-Series cylindrical cells (Tesla, BMW) Also the space is very fluid in terms of new technology coming up. Things like new Cathode chemistry (Manganese based – LMFP) or silicon anode. They need to move with the market or their product might not remain relevant. Lot of focus on Fast charging now with CATL’s Shenxing battery launch.

-

Getting contracts from OEM’s to ensure plants are utilized.

-

Also, need to note that the batteries are unique for every OEM. So they cannot be interchanged. Losing a contract/non renewal of a contract is a big dent as new contracts again need to go through the qualification process.

| Subscribe To Our Free Newsletter |