Affle – Q2 FY’24

Affle’s Q2 numbers are out, this post is my take on the results. I would love to hear all of your opinions on the same.

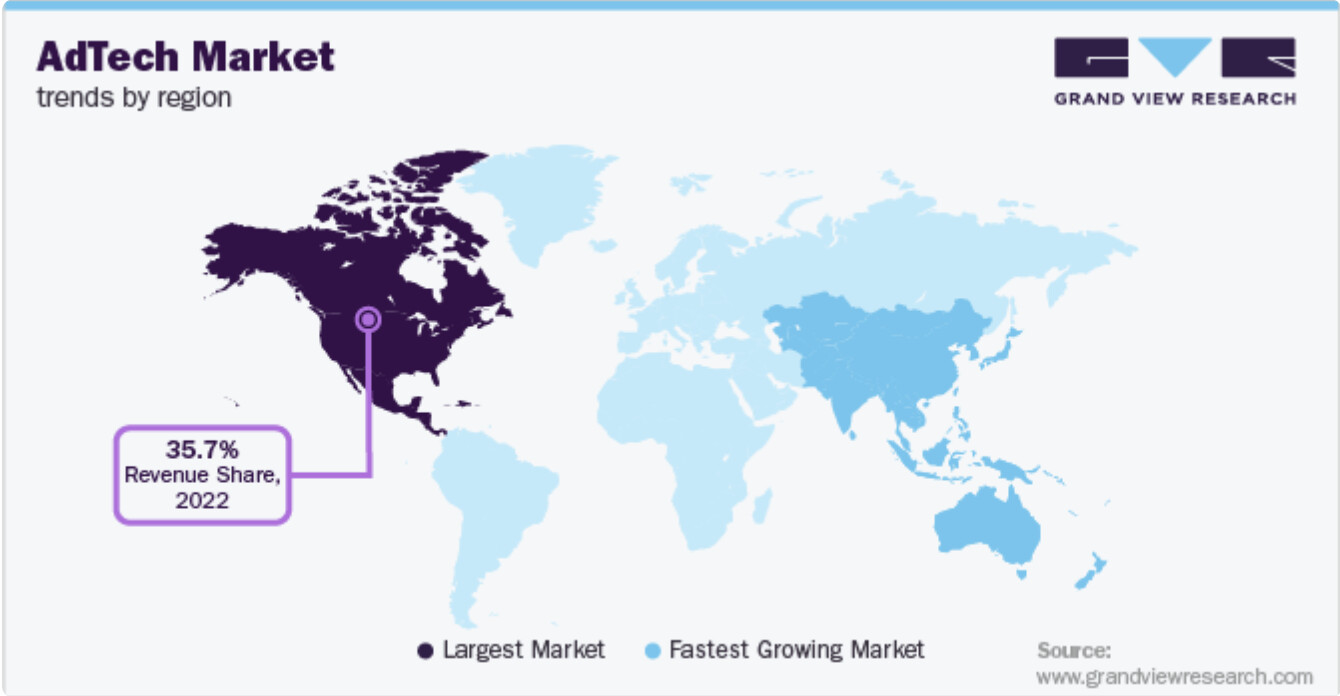

AdTech industry prospects (India):

-

India’s consumer market ranks among the world’s fastest growing.

-

According to Statista, the Indian adTech market is growing at a 15% CAGR over the next 3-5 years. Mobile ads account for the largest share of the Indian AdTech market. The share of ad spends on mobile devices across India is around 75-78% of the total digital media expenditure by 2023.

-

As of 2023, India boasts over 1.2 billion internet users, securing its position as the second-largest online market globally, trailing only China.

-

Programmatic Advertising – By 2024, an estimated 90 percent of all online ad expenditure will be channelled into programmatic advertising. This meteoric rise underscores advertisers’ growing confidence in programmatic strategies to effectively connect with their target audiences.

-

The advent of widespread 5G networks will unlock fresh avenues for immersive advertising experiences, characterized by seamless connectivity and accelerated data speeds.

-

Globally, the AdTech market is expected to grow at a 14% CAGR over the next 7 years. The mobile advertising segment is anticipated to progress at the fastest CAGR of 15.7%.

Sectoral conclusion:

Affle is very well placed in a growth focused sector. An important point to note: Affle is highly focused on the fastest growing markets globally. Although several of the numbers I have spoken above are primarily for India, it is important to note that India accounts for about 30% of Affle’s revenue. Remaining 70% of revenue comes from other international markets (Southeast Asia (SEA), Middle East and Africa (MEA), North America, Latin America (LATAM), Europe, Japan, Korea and Australia). Only half the world is online with US/UK at ~80% smartphone penetration and Emerging Markets trailing with much lower levels of smartphone penetration. That’s perfect!

Results – Q2 FY’24

Summary (consolidated):

-

Sales: 431Cr (+21% YoY)

-

Net profit: 69Cr (+13.5% YoY)

-

OPM: 20% (Stable margins)

-

Shareholding pattern changes:

FII: -0.3%

Public: -0.4%

DII: +0.7%

On the face of it, the results look stable. Why isn’t the price reacting? Let’s dig in slightly deeper:

-

CPCu statistics: For those who are new, a “Converted User” is someone who will see an ad but they also take some decisive action like a purchase, an app download or an app launch. Affle generates 90 per cent of its revenues through cost per converted user (CPCu) model in which the company charges for an advertisement only if the user gets converted. Hence 400Cr out of the 431Cr in revenue is from the CPCU model this quarter. Here is what’s interesting: the growth in the number of converted users has slowed down in FY’24. Q2 FY’22 to Q2 FY’23 saw a growth of 33% but Q2 FY’23 to Q2’FY24 saw a growth of only 13% (Probably due to global slowdown in international economies). Despite this, they were able to maintain a revenue growth of 21% YoY! How? The key is the Average CPCU. It has increased by 9% YoY from last year to Rs 55.6. This might look very subtle but this is probably the most overlooked characteristic of a consistent performer – pricing power! Affle is constantly moving closer to premium segment customers. They defend their pricing by offering more premium products to their clients

-

PAT growth: PAT growth is around 14% YOY, although management has always guided for 20% bottom line growth. Some of the underlying reasons are listed below. But whatever said, this is not at par with the guidance, and I’ll discuss the impact in the valuation section below.

-

Gaming sector pullback: There was a pullback of about Rs 11Cr this quarter due to regulatory changes towards applicability of GST within the online gaming industry in India. Gaming is one of the verticals under their ‘EFGH categories’. However the management seems to be confident that they can offset this pullback from the other high growth categories. A notable point here is that gaming has been a positive vertical for the company in the international markets. The Indian gaming sector is what has taken a slight hit, and we will need to wait for the coming quarters to hear the management’s updates on the matter. The management calls this a “one-off” event and should ease out in the next quarters. Some people might have questions about one of their acquisitions: YouAppi, a gaming focused programmatic mobile app marketing platform, works with mobile gaming app companies across the globe. Please note that YouAppi is primarily contributing to top line numbers from developed markets and not much in India.

-

Fintech sector slowdown: Another 14Cr of pullback from the Fintech vertical primarily due to high interest rates in the economy. Since interest rates are cyclical this should improve in the coming quarters with inflation coming under control and quantitative easing taking presence.

-

Fundraiser details: Affle recently raised Rs 750Cr by the allocation of preferential shares. Preference shares allow an investor to own a stake at the issuing company with a condition that whenever the company decides to pay dividends, the holders of the preference shares will be the first to be paid. But the question to ask is what will we do with the 750Cr coming in + 500Cr already in cash balance. The management aims to use this on AI development. They plan to utilise this capital over the next 4 years. Hence, adjusted ROCE won’t improve/deteriorate anytime soon. That’s not very encouraging in my opinion.

-

Increase in other expenses: Management has clarified this to be for the acquisition of YouAppi and increase marketing activities around the festive season.

-

Other important timelines: Samsung India development and integration Phase-3 to be completed within this year itself.

Valuation:

-

If you’re reading this post then you probably also know that Affle is definitely an expensive performer. Today, it commands a PE of around 50, which used to be a whopping 150+ a couple years back. So let’s all agree that there has been a PE re-rating for the company. But why? It all has to do with the growth numbers in the snippet below. Back when it commanded a 150+ PE, Affle was experiencing unsustainable revenue growth rates of 100%+ YoY. But the growth rates have now reached a sustainable range of around 15-20% YoY with the management guiding for around 20% PAT growth rate. With this information, here are a few numbers that paint a false picture:

Don’t look at 5 year compounded growth rates

Don’t look at 5 year median PE

Don’t look at 5 year ROCE and ROE

Affle’s management themselves don’t guide for such growth rates anymore, and as retail investors, don’t blindly look at historical returns!

-

What about its overall financial performance? I’d call it a solid stable performance. The Piotroski score agrees with the numbers as well assigning a 8/9 score for Affle which is outstanding.

-

So what’s a reasonable PE multiple to assign with an expectation of 20% PAT growth? I like to use PEG as a good measure for this. In my opinion, being as conservative as possible, on the lower end I would assign a PE of 35 and on the higher end a PE of 50. Hence, in my opinion I would not consider Affle to be undervalued as of now. I would say it’s somewhat fairly valued, but there can still be room for correction if the numbers continue to miss the guidance. These numbers are backed up with some calculations in the next point.

-

Why is the price falling? Well, look a couple quarters forward. The management is guiding for Rs 1800 Cr in profit. If we assume a stable 20% EBIDTA margin, Affle should end the year with about Rs 300 Cr in net profit. Divide that with the number of outstanding shares, that should give us an EPS of around Rs 22.5. As discussed earlier, assuming a fair PE of around 45, an approximate fair price would be 45 X 22.5 = Rs 1012. It suggests that the market is assigning a fair PE of around 45 based on the management’s guidance, which is not tough to expect.

I hope this helps, I would love to hear everyone’s opinions on the same.

| Subscribe To Our Free Newsletter |