Hi Nikhil,

Thanks for sharing the visit note.

The DRHP is a very good read to understand the fragrances and flavors industry.

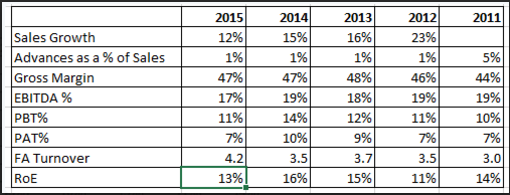

The easy part first. Numbers.

As we can see from the stability in gross margins, it’s a pretty good business. I think with increase in capacity utilization, there is a possibility of NPMs going up. But given that the volume growth is at 10-13%, not sure if we can see a big jump in operating leverage.

Market share looks great. Do you have any idea if this is based on production or sales? Usually, this is an approximation of sales, but I have heard that Nielsen also does based on production, especially in a predominantly B2B biz like SH Kelkar.

One thing which really stood out for me in the DRHP was below, and wanted to check if you have any insights/can check with the management/IR as you already visited them:

Why did Blackstone choose an unfavorable CCPS conversion (and that too as recently as October 5th)? What was given in return for this unfavorable dilution?

Of course, as with all IPOs, valuations are a bit expensive. But am happy such good businesses are listing in the secondary markets.

Disc: Not applying in IPO

| Subscribe To Our Free Newsletter |