Q2 FY24 Concall Notes

Introduction and Current Scenario

- Slow NHAI tendering until September ’23 due to prolonged monsoon.

- Recent acceleration in bidding process and internal changes.

- Anticipation of increased bidding activity in the next 4-5 months.

Diversification Strategy

- Focus on diversifying orders in various sectors.

- Opportunities identified in railways, metro, and water sectors.

Railway Sector Opportunities

- Participation in the Amrit Bharat Railway Station Scheme for station revitalization.

- Bidding for railway projects totaling Rs. 1000 crores, with plans for additional bids in FY23-24.

- Exploration of opportunities in the metro sector, both elevated and underground projects.

Water Sector

- Slow awarding in the water sector during the initial six months.

- Expectation of momentum in the coming months.

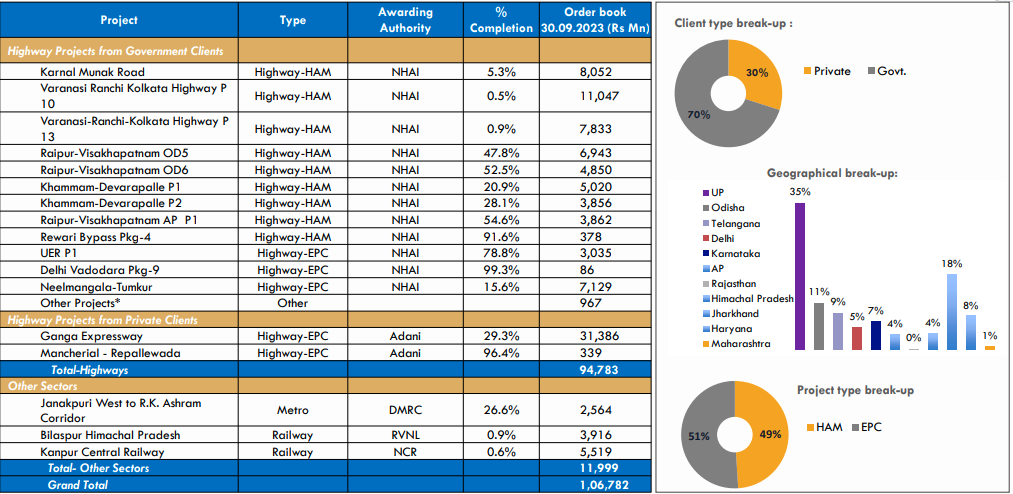

Order Book and Presence

- Order book at Rs. 10,678 crores, spanning 11 states.

- EPC segment constitutes 51%, while HAM segment comprises 49% of the total projects.

Operational Highlights – EPC Projects

- Ganga Expressway at 29.3% completion.

- Delhi UER projects at 78.8% financial progress, expected to complete by December ’23.

- Neelmangala-Tumkur NHAI project at 15.6% completion.

HAM Projects Progress

- Raipur-Visakhapatnam packages progressing well, expecting completion by June ’24.

- Khammam-Devarapalle Project at 28.1% completion.

- Rewari Bypass project to be monetized in the second tranche.

Railway and Metro Project Updates

- Progress in DMRC Metro project at 26.6% completion.

- Appointed date received for RVNL Rail Project.

- LOA received for Kanpur Railway Station Project, with machine mobilization completed.

Other Updates for H1 FY24

- PCOD for Mancherial Project received on July 26, ’23.

- Final sanction for Varanasi-Ranchi-Kolkata packages 10 and 13 received from HDFC and Axis.

| Financial Highlights | H1 FY24 | Q2 FY24 |

|---|---|---|

| Standalone | ||

| Overall Revenue | Rs. 2140.8 crores (+17.8% YoY) | Rs. 869.5 crores (+15.6% YoY) |

| EBITDA | Rs. 343.2 crores (16% margin) | Rs. 138.4 crores |

| PAT | Rs. 180 crores (8.4% margin) | Rs. 61.7 crores (7.1% margin) |

| Consolidated | ||

| Consolidated Revenue | Rs. 2305.7 crores (+21.2% YoY) | Rs. 954.5 crores (+20% YoY) |

| Consolidated EBITDA | Rs. 500.9 crores (21.7% margin) | Rs. 220.2 crores |

| Consolidated PAT | Rs. 246.5 crores (10.7% margin) | Rs. 96.1 crores (10.1% margin) |

Strategic Move: Sale of 4 HAM Projects

-

Agreement:

- Signed share purchase agreement with Highway Infrastructures Trust (backed by KKR).

- Involves the sale of 4 HAM projects, a significant move for the company.

-

Transaction Progress:

- NHAI and lender approval secured for the first tranche of 3 SPVs.

- All conditions met for successful closure; expected in November ’23.

-

Financial Outlook:

- Confident in achieving expected numbers with a (+20%) revenue upside.

- Aiming for order inflow with Rs. 5000-6000 crores from road and diversified sectors.

-

Future Initiatives:

- Preparing for new projects, analyzing costs, and engaging with solar and metro sector clients.

- Focus on operational efficiency and execution capabilities.

-

Digital Transformation:

- Prioritizing digital transformation for automation in operations.

- Aiming for enhanced financial indicators through a transparent real-time working environment.

Order Inflow Concerns and Projections:

-

Initial Projections:

- Original expectation for the year was around Rs. 9000 crores order inflow.

-

Current Outlook:

- Current projection lowered to Rs. 5000-6000 crores due to slow progress.

- Factors influencing the decrease include state elections and delayed RFQ results.

-

Reasons for Confidence:

- Anticipated acceleration in NHAI projects, aligning with Gati Shakti initiatives.

- Optimistic about achieving a minimum of 3000-plus kilometers awarded in the next four months.

-

Future Initiatives:

- Diversification into metro and railway projects bidding with a potential of Rs. 8000 crores.

- Analysis and engagement in solar and metro sectors for new opportunities.

Compensation and Future Order Inflow:

-

Compensation for Shortfall:

- Confident in compensating for the current year’s shortfall in the next fiscal year.

- Expected addition of Rs. 10,000-12,000 crores from Quarter 2 onwards in FY25.

Revenue Growth and Segmentation:

-

Current Year’s Revenue Growth:

- Current projection for revenue growth is 20% compared to the initial 25%.

- On track with the annual report’s revenue target of Rs. 5400 crores for the year.

-

Segment-wise Breakdown:

- Revenue segmentation remains consistent with earlier projections.

- Major contributions from Ganga Expressway, six HAM projects, and diversified sectors like metro and railways.

Increase in Unbilled Revenue:

-

Ganga Expressway Projects:

- Milestone payments not aligned with physical progress.

- Unbilled portion around Rs. 150-200 crores due to the 2-3% gap in physical and financial progress.

- Continuity in unbilled status due to monthly milestone completion.

-

NHAI and SPV Projects:

- NHAI projects, especially in UER, facing similar milestone payment challenges.

- SPV projects experiencing an increase due to project execution initiation.

- Unbilled amounts likely to stabilize around Rs. 500 crores by Quarter 3.

- Old NHAI and MoRTH projects with receivables and claims causing unbilled figures.

Confidence in NHAI Ordering:

-

Strong NHAI Bidding Pipeline:

- NHAI holds a robust bidding pipeline.

- As of March ’23, approximately Rs. 60,000 crores worth of projects were expected to be awarded.

- Delayed due to certain reasons, NHAI plans to award Rs. 40,000 crores by the end of the year.

- Anticipating the awarding of around 2500-3000 kilometers from the current bidding pipeline.

Revenue Guidance and Inflow:

-

Current Fiscal Year (2023-24):

- FY24 Revenue Guidance: Targeted revenue of Rs. 5,400 crores.

- FY25 Revenue Expectation: Anticipating revenue in the range of Rs. 6,000 to Rs. 6,200 crores.

-

Future Revenue Growth:

- FY25: Expected to complete existing projects, anticipating revenue from existing order backlog to be around Rs. 5,500 crores.

- Order Backlog: Rs. 10,600 crores.

- Targeting to add new orders in the range of Rs. 5,000 to 6,000 crores.

Margin Guidance:

- Expected Margin: 15.5% to 16%.

Impact of Construction Ban in Delhi NCR:

- UER 1 and Metro projects expected to have minimal impact.

- Special permissions anticipated due to the high priority and monitoring by PMO.

- Pollution department likely to grant relaxation for these projects.

Arbitration Claims:

- No significant arbitration claims against NHAI or any government body.

- Small claim of Rs. 10 crores with Agra Development Authority; Rs. 6 crores already provided.

- Consolation in progress for four NHAI projects completed in 2018, amounting to Rs. 22 crores.

Segment-wise Revenue Breakup for Q2 FY24:

- Ganga Expressway (Adani Project – Mancherial): Rs. 290 crores

- NHAI EPC: Rs. 188 crores

- SPVs: Rs. 303 crores

- Metro and Railway: Approximately Rs. 52 crores

Railway Projects Margins:

- Bidding margin for railway projects is set at approximately 14%.

Competitive Scenario:

- HAM: Moderate competition with 7 to 10 bidders.

- EPC: More aggressive with 20 to 25 bidders.

Diversification Projects Margins:

- Diversified sector projects (e.g., water, metro) margins range from 12% to 15%.

Revenue Composition:

- Targeting at least 10% of total turnover from metro and railway projects this year.

- Aiming for 20% of total order execution by 2025 and 25% by 2026 from diversified sectors.

Depreciation Increase:

- Increase in depreciation due to the addition of new assets, particularly shuttering.

- Expected to continue throughout the year.

- Shuttering depreciates faster, impacting the overall depreciation cost.

- Anticipated depreciation and interest costs to remain similar to the previous year, with a slight increase of about 0.25%.

Execution Timeline:

- Highway Projects: Approximately 24 to 36 months.

- Railway Projects (e.g., Kanpur Railway Station, RVNL): Ranges from 30 to 36 months.

- Metro Projects: Typically completed in about 30 months.

- Water Projects: Execution timeline extends to around 36 months.

PAT Margin Analysis:

- Recent Decline: Standalone PAT margin affected by a rise in interest costs.

- Asset Monetization Impact: Anticipated improvement in PAT margin due to asset monetization of HAM projects.

- Finance Costs: Expected to be in a similar range as previous years, around 1.25% of total turnover.

- Employee Costs: All-time high due to project mobilization, but anticipated to normalize.

Future Outlook:

- PAT Margin Improvement: Confidence in the PAT margin returning to earlier levels, potentially around 8.6%.

- Finance Costs Management: Efforts to maintain finance costs within the historical range.

- Mobilization Impact: Employee costs expected to stabilize as execution catches up.

Ganga Expressway Impact:

- Acknowledgment of the concern regarding the eventual completion of the sizable Ganga Expressway project.

- Capability and Qualification: Successful completion of significant elevated portions in projects like UER at Delhi and Gurgaon Sohna positions the company for bidding on large-sized projects.

- Future Prospects: Exploration of opportunities in high-magnitude projects, including high-speed network corridors for railways and tunnel projects through joint ventures and alliances.

Order Inflows Analysis:

- Bidding Activities: Participation in several bids; however, loss of projects due to unmet margin expectations.

- Expected Momentum: Anticipation of an increase in momentum and order inflows from November onward.

- Market Share Loss Explanation: Loss of projects with unsatisfactory margins; optimistic about the upcoming months.

Bidding Activities Overview:

-

Road Sector Bids:

- Submitted bids for 6 road sector projects.

- Bidding on the Chambal Expressway project.

-

Railway Sector Bids:

- Expressed interest in railway projects, estimating opportunities worth around 8,000 crores.

- Shared ongoing bids in the state of Chhattisgarh; results pending.

Diversification Strategy:

-

Metro Projects:

- Qualification for metro projects achieved through recent project completions.

- Expectations of bidding for metro projects, independent of railway opportunities.

-

Tunnel Opportunities:

- Exploring tunnel opportunities in Northeast states, including Himachal Pradesh, in collaboration with DRO.

-

Joint Ventures and Alliances:

- Existing Orders: Solely secured all current orders without joint ventures.

- Future Prospects: Consideration of joint ventures for projects where 100% qualification is challenging (e.g., water projects, large-scale metro).

| Subscribe To Our Free Newsletter |