I tried to check this statement out from the CEO and he does seem to have a point. I was quite surprised by the vast gap in the way Workiva is valued on the NYSE and between the Iris valuation here. Just for context:-

- Workiva (Workiva | Software for ESG, Audit & Risk and Financial Reporting) is valued at ~5.1 Bn USD today, whilst guidance for FY 23 revenue is ~USD 627-628 million

This means that Workiva is being valued at >8x sales, 1 year forward, more in line with SAAS company Rategain (~10x sales). Even after the recent run-up, Iris is still quoting at 3.2x sales.

Big differences : Iris is profitable whilst Workiva is loss making. Iris is miniscule as compared to the established Workiva though.

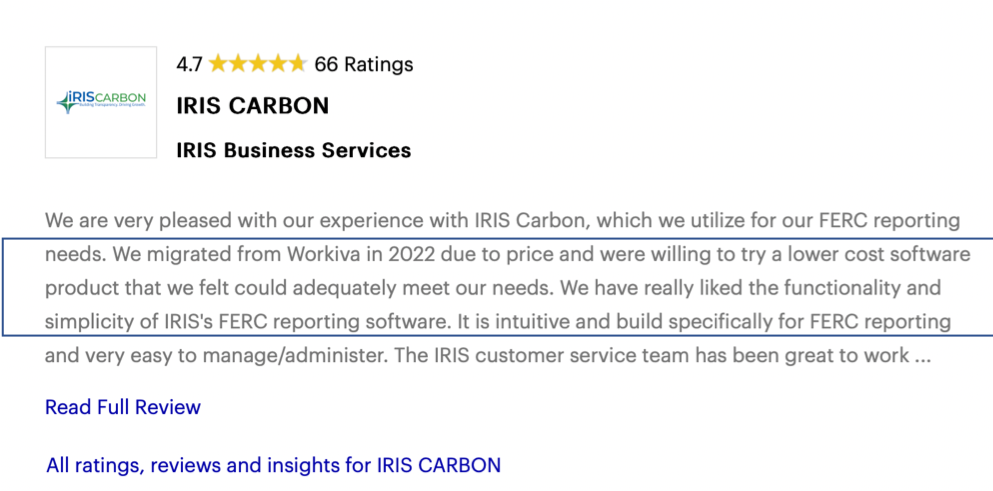

- Workiva is a giant in the business, but still growing fast. This does show that the TAM could be large for Iris, and at the same time, competition is strong. Could Iris be the price competitive Indian alternative? I found this review especially interesting

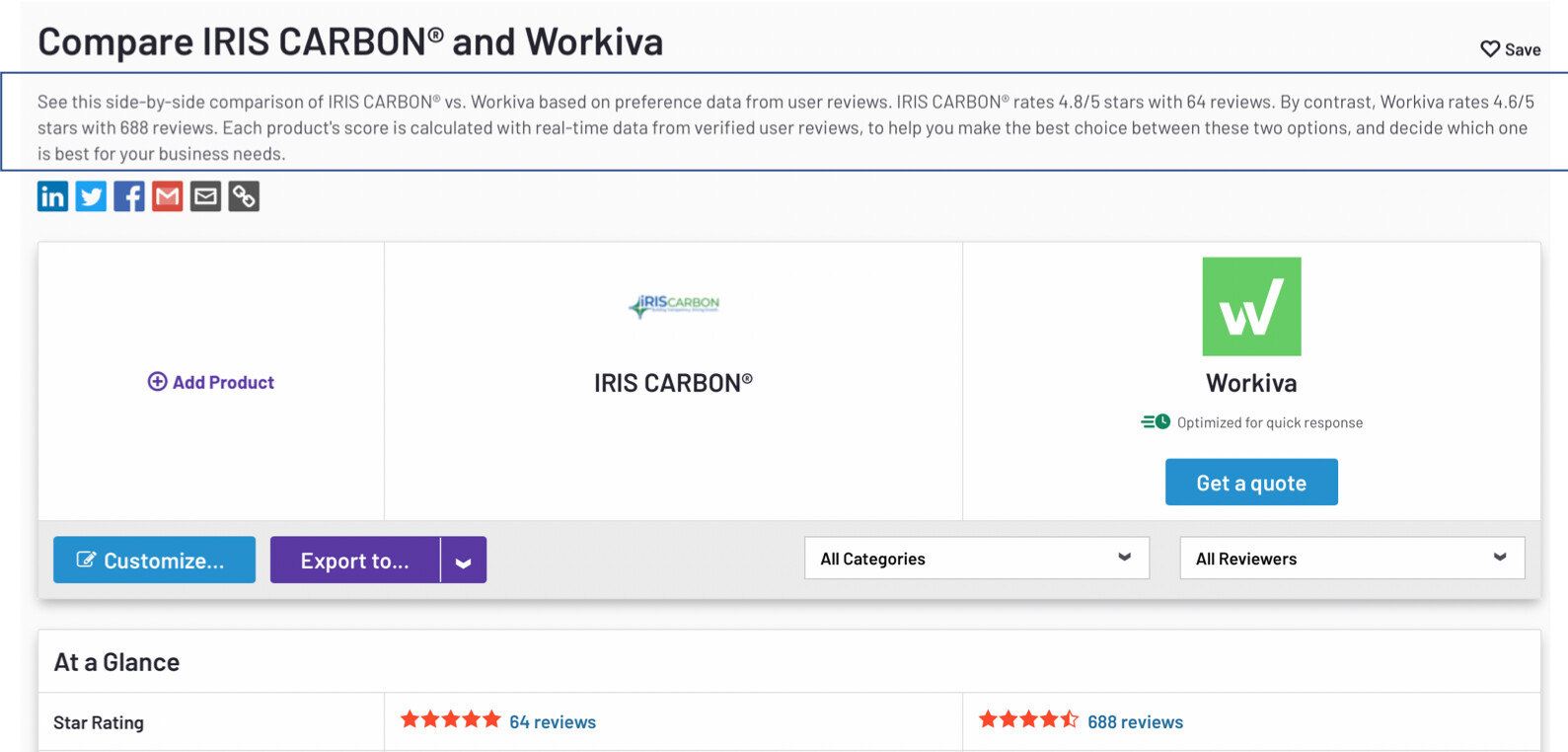

- Iris Carbon has some really good ratings on G2review which looks promising, at 4.8 is slightly better than Workiva at 4.6. But we need to understand that Workiva has a much wider review base, and also I have a feeling could be the better product being so much larger in terms of revenue.

Disclosure : I am invested in self and family accounts and am biased. I have made transactions in the stock in the last 30 days. I am not a SEBI registered advisor, not an expert and this is not investment advice.

| Subscribe To Our Free Newsletter |