My notes on Ami Organics:

Source: screener.in

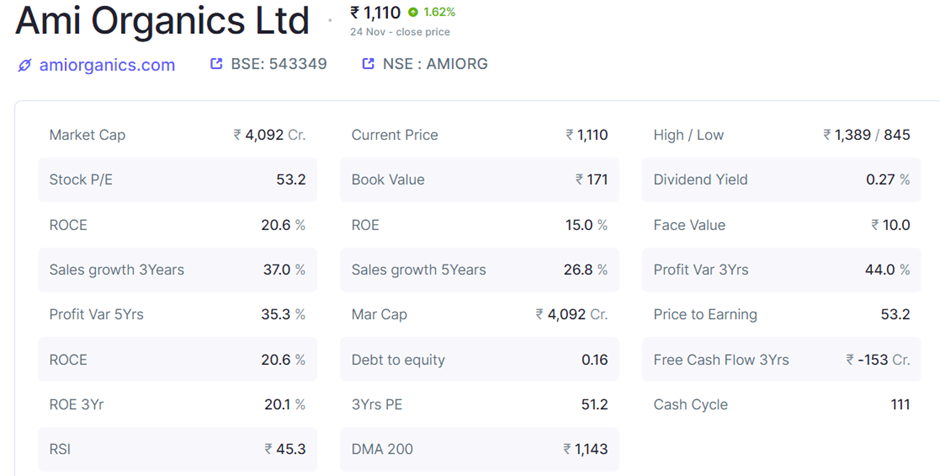

Summary rationale: I bought Ami Organics Ltd’s (AOL) just last week (24th November) making it over 5% of my portfolio. On the face of it stock looked expensive at over 50PE, however given the growth opportunities and its presence in sunrise industry (EVs and semiconductors) it looks reasonably priced.

My thesis on AOL is mainly based on three key opportunities:

- Long-term contracts with Fermion for 3 key molecules. One of the molecules Darolutamide used in Nubeqa is likely to have peak sales of over USD3 billion. AOL is the exclusive supplier for intermediates used in Darolutamide (an anti-cancerous drug) for a long-term basis. A back of the envelope calculation puts this opportunity to about 1200 crores* annually by 2030 if fully serviced by AOL. The patent for this drug expires in 2030. If we assume even other 2 molecules are as large then opportunity seems huge.

*Assuming cost of intermediate accounts for 5%. The cost of Acetaminophen which is used in paracetamol tablets like Dolo 650 is about 15%.

-

Electrolyte additives: AOL has developed electrolyte additives which are used in lithium batteries to increase the life of the batteries. Market size for this is estimated to be over USD1 billion and likely to double to USD2 billion in the next 3 to 4 years. AOL aims to garner 10% of this market which puts its revenue potential to about 1600 crores annually by end of 2030.

-

Semi-conductor chemicals business: AOL recently in Q2 FY24 acquired 55% stake in Baba Fine Chemicals (Baba) which is semiconductor chemicals. AOL aims to take Baba’s revenue to over 200 crores by FY25. This is a high margin business with EBITDA margins in 40% range vs. current AOL business in 20% range.

In addition to above, AOL continues to launch large market size products like UV absorber, and has maintained that further contracts with Fermion are in the discussions. All the new products are likely to support margins and operating leverage is likely to result in margins in 25% vicinity from current range of 20%. Currently margins are somewhat depressed as the company integrated Gujarat Organics plants over the last two years which exhibited very low margins.

I have modelled two scenarios

Opportunity based:

and,

Capex and management guidance-based scenario

In above two scenarios my worst return expectation by FY28 is likely to be 20% CAGR in scenario 2 (capex and management guidance based) with PE derating to 30. While best return expectation is likely to be at 43% CAGR in opportunity-based scenario with re-rating to 60 PE.

Right to win:

- Only company outside China to have developed Electrolyte additives

- 50-90% global market share in key molecules

- Chronic Therapy focus: ~90%

- Majorly backward integrated to Basic Chemical level

- Strong customer relationships with customers with relations lasting over a decade

- Diversified across pharma, agro, semi-conductors and electrolytes

Though some of the risks to above estimates are mitigated by first mover (outside China) advantage, exclusive agreements and India cost advantage, we still need to account for below risks:

- Regulatory risks related to Pharma Intermediates business – FDA related issues

- Product obsolescence – if a new and much more effective medicine becomes available then the expected opportunity of Fermion contract may not play out. It may similarly impact company’s existing products and pipeline.

- Competition – Electrolyte additive opportunity may not fully fructify if another competitor is able to replicate same outside of China

- EV adoption slow down

- Concentration risks – top 10 customers account for 58% of revenues.

Customers:

Company caters to major domestic and overseas MNCs.

Source: AOL Q2 24 presentation

Peers: Divis Lab (APIs), Neogen and Neuland.

Thanks

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

| Subscribe To Our Free Newsletter |