My notes on Pricol:

Source: screener.in

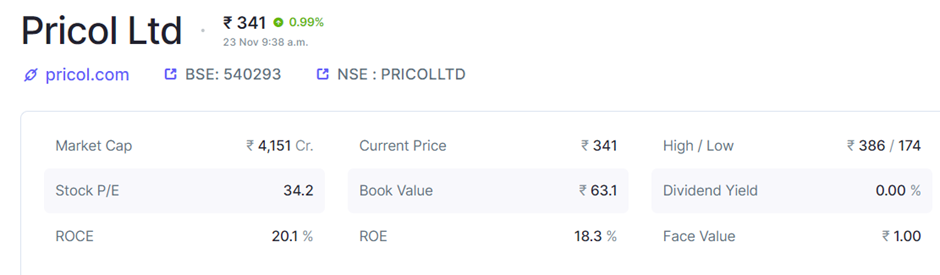

Summary rationale: Pricol was on my radar for last 6 months but now with about 12% correction I became interested. Price corrected post soft Q2 24 results. However, management continues to guide ~4,000 crore revenues by FY26 and some margin improvement (~200bps over next two years). Back of envelope calculation showcases about 35% revenue CAGR and profit growth well above it. LTM PE is 34 which means company is available at 1PEG*. I find companies less than 2PEG attractive.

*PEG: PE (price to earning multiple) to growth ratio.

DIS systems used to be in 200-300 rs for per vehicle now they are priced at 1200 per vehicle (2-wheeler). With increased digitisation and more sophistication these products are likely to go in 2000-2500 rs range over the next three years, as per the management.

Other triggers:

- Company has entered 4-wheeler market very recently with Tata Nexon models, previously they could not due to some anticompetitive agreements. If they can garner more share in 4-wheelers then it shall provide huge upside to the company.

- Increasing EV penetration results in high value per vehicle and higher margins.

- Beyond FY26 companies’ new product initiatives (Telematics, Battery management systems Micro Motors and Robotics and Artificial Intelligence based processes and equipment) through JVs will start bearing fruit and that will provide additional kicker beyond FY26.

- Ownership battle between promoter group and Minda Corp (15.7% stake) shall keep prices supported. Minda corp has reached out to competition commission to increase its stake in the company to ~25%.

Right to win:

- Over 50% markets share (in value terms) in 2 wheelers (2W), 70% market share in CVs and 50% market share in tractors.

- 8 of 10 2W EV models are served by Pricol

- Entry barrier for competition is moderate to high as auto ancillaries take about 2-3 years for product approval and another 6 to 12 months for production. In addition, products are customised for each model.

Risks:

- Tech disruption

- EV adoption slowdown

Products: Pricol makes driver information system (65% of revenues) and actuation, control and fluid management system (35% of revenues).

Source: Pricol Q2 24 presentation

Customers:

Company caters to all major 2wheeler, 3wheeler, commercial vehicles, tractors manufactures

Source: Pricol Q2 24 presentation

Competitor: Minda Corp

Thanks

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

| Subscribe To Our Free Newsletter |