I think that is the nature of most businesses in this sector. However, I see Laurus to be a bit more aggressive in moving up the ladder and trying new things. If I look for the next Pfizer kind of companies in India, Laurus definitely comes in the radar.

The main concern is the cash burn in these activities. In that, I see two major streams of capital deployment:

-

Business model / product mix changes, requiring constant influx of capital, which can be expected and should be seen alongside the growth rate of company. I see Laurus having a good leg of growth coming ahead.

Their focus in CDMO is actually good. However, CDMO being a lumpy business can bring down the biz performance during lean period. Nevertheless, this is a good & necessary long term plan to match competition - Capex initiatives yielding fruition → This I am much keen to follow up since it has a twin benefit of improved revenue and margins (operational leverage). As per the mgmt, the demand looks good and inventory destocking should be over. So, there is a high likelihood that volume & capacity utilisation starts going up. Unless it does, we can’t expect the margins to move to a healthy level as mgmt mentions.

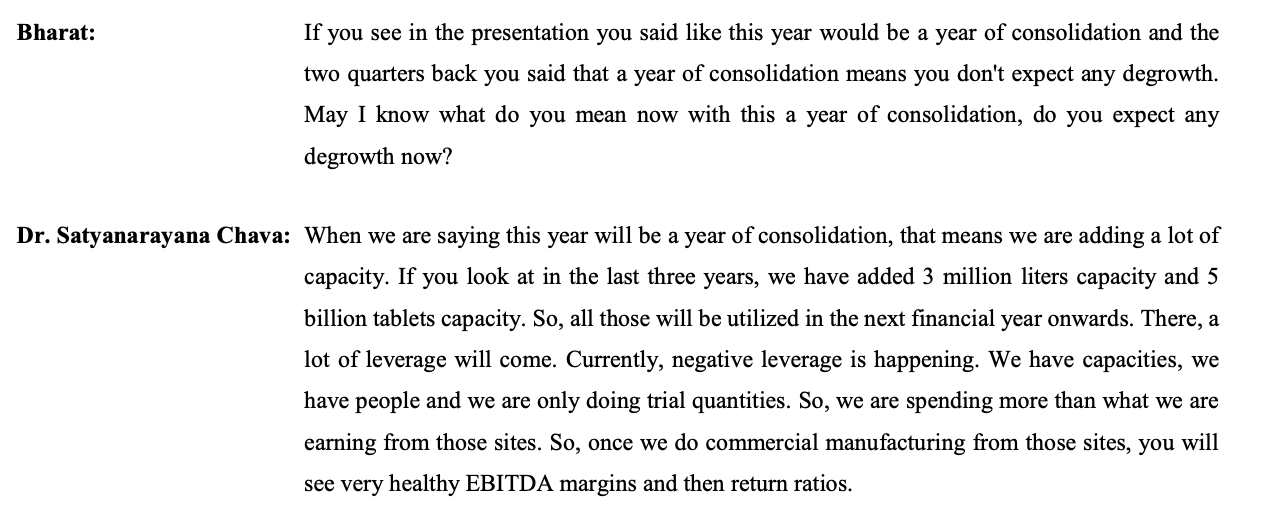

Snippet from earnings call below:

| Subscribe To Our Free Newsletter |