Regulatory inspections have become once again a major concern for Indian pharma companies. Marksans seems to be doing well on that front. There was a PADE inspection at Marksan’s Goa facility and had two observations. Seems like minor issues as the company mentioned in August concall. Also, the company has successful USFDA inspection at it Time caps facility without any observations and German health authorities also had an inspection of its Teva facility with no major observations.

The company has been able to improve its sales continuously over the past many quarters and is expected to continue to do so in the future with the new facility contributing.

Gross margins have also improved with freight and raw material prices coming down.

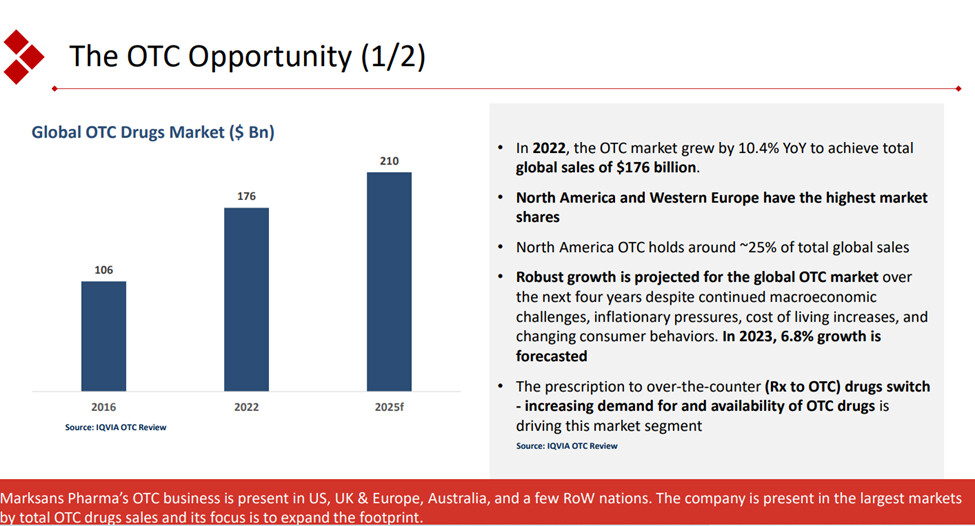

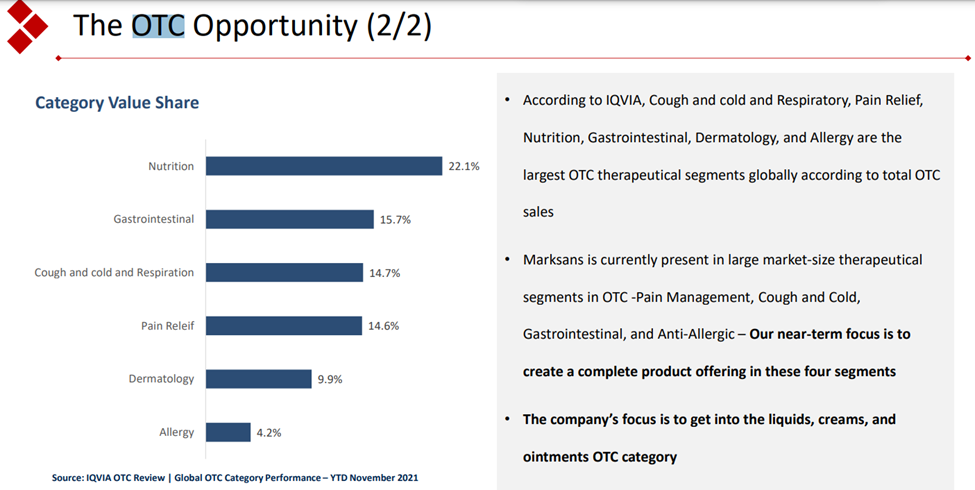

The company seems to be focussing on the OTC opportunity. OTC contributed 74 % of the revenue as of FY23. The company has illustrated the prospects of OTC pharma market in the presentation.

This focus of the company seems to be the differentiating factor for the company. The company so far has been able to capitalize on this Rx to OTC switch. The company is also planning to integrate backward to API for major molecules which could expand margins. They are yet to file DMF for these molecules. The deal for a frontline marketing pharma company in the EU still seems to be elusive. The company has a cash of 668 cr on the balance sheet. Would be interesting to see how they plan to utilise the funds.

Have plans to increase their R & D exp from 1.6 % of sales to 4 – 5 %.

| Subscribe To Our Free Newsletter |