The company had a very tough time in the past 8 to 9 quarters. As far as input costs are concerned, I don’t think the situation could get any worse than it is. The only silver lining could be that there were no issues in offtake by OMCs. Broken rice prices started moving up first followed by the power prices. After the coal prices came down there was some respite in power prices. But then broken rice prices started going through the roof. Then, the company was able to procure rice from FCI at a fixed price but with Govt stopping supply of rice Globus had to buy rice and maize from the market.

Even in such adverse market conditions, Globus was able to increase its quarterly sales from 382 cr in Sept’21 to 567 cr in Sept’23. However, the margins fell from 23 % to 7 %.

One of the major reasons for the fall in margins is raw material prices. Also, the increased contribution from the bulk segment is another factor. With newer capacities coming in the contribution from the bulk segment has significantly increased. Also, the company started investing in marketing for their prestige and IMFL division.

Demand for ethanol remained strong with prices revised multiple times by the OMCs.

The company sees the IMFL segment to be the growth driver for the company.

Company’s presence

The company has an IMIL presence in Rajasthan, Haryana, West Bengal, and Delhi. Globus dominates the Rajasthan market as far as value and value-plus segments are considered. They were able to further strengthen their market share which is now 35 % of the value segment and 61 % in the value plus segment. The company has plans to foray into one new state in IMIL. However, they have not disclosed which state it is. Doesn’t have plans to move into the IMIL business in Jharkhand and Orissa. Must be UP.

The company has not been able to gain any major market share in West Bengal. The company has blamed the route to market for this.

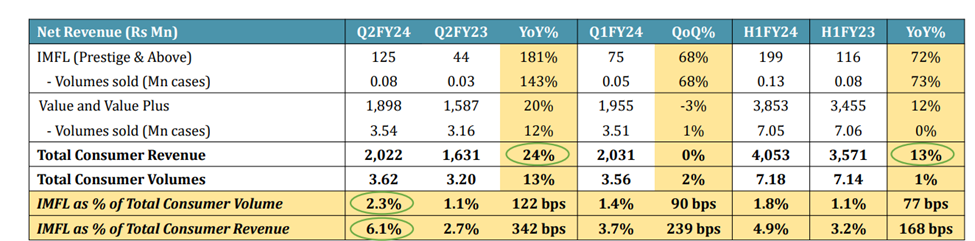

IMFL revenue is currently 6.1 % of the consumer revenue

They have a presence in Delhi, West Bengal, Haryana, Uttar Pradesh, and Punjab. They entered Uttar Pradesh and Punjab in the last year. Have plans to enter Rajasthan in Q3 and Jharkhand in Q4. I am very positive about the company’s foray into Rajasthan. The company has a very good presence in the state for a very long time. However, the company has mentioned that the distribution and marketing required for IMFL and the value segment are very different.

As per the management, it may take 3 years for the IMFL business to stabilize in a state. Marketing of a brand is not going to be easy.

Debt and other metrics

Debt has increased significantly over the last year with the company increasing its capacity aggressively.

Debt increased significantly to 291 crores in March’ 23 from 180 crores in March’22, which further increased to 352 crores in Sept’23. However, the company mentioned that they reduced the debt by 37 crores in last quarter. It seems that debt repayment is something the company will focus on going forward. The good thing is the cost of debt is close to 4 % which is keeping the interest costs at the levels we see now.

Trade receivables and inventories have also made a huge quantum jump, which could be due to higher contributions from ethanol sales. The effect of this is offset partially by the increase in trade payables. Going forward inventory days may go up as the company informed that they may start stocking up raw materials in the season from next year onwards. The working capital and conversion cycle may get extended due to this.

Capacity Expansion

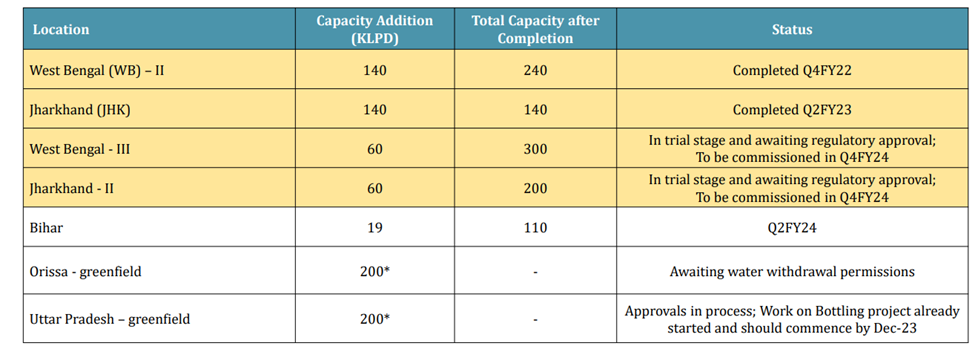

An additional capacity of 120 KLPD will be onstream in Q424. The bottling plant is expected to commence in Dec-23. The bottling plant seemed to be of strategic importance in bringing down the costs of consumer business.

The company expects margins to start increasing from Q424. With the Kharif crop season, the availability of rice may increase bringing some respite to prices. However, as per forecasts, the rice crop is expected to be lesser than last year even though the area under paddy cultivation is slightly higher than what it was last year.

| Subscribe To Our Free Newsletter |