Been a busy few months. Definitely some froth in smallcap space; hard to find long term ideas where the risk-reward is better than the banks. Following changes made to the portfolio:

Additions:

-

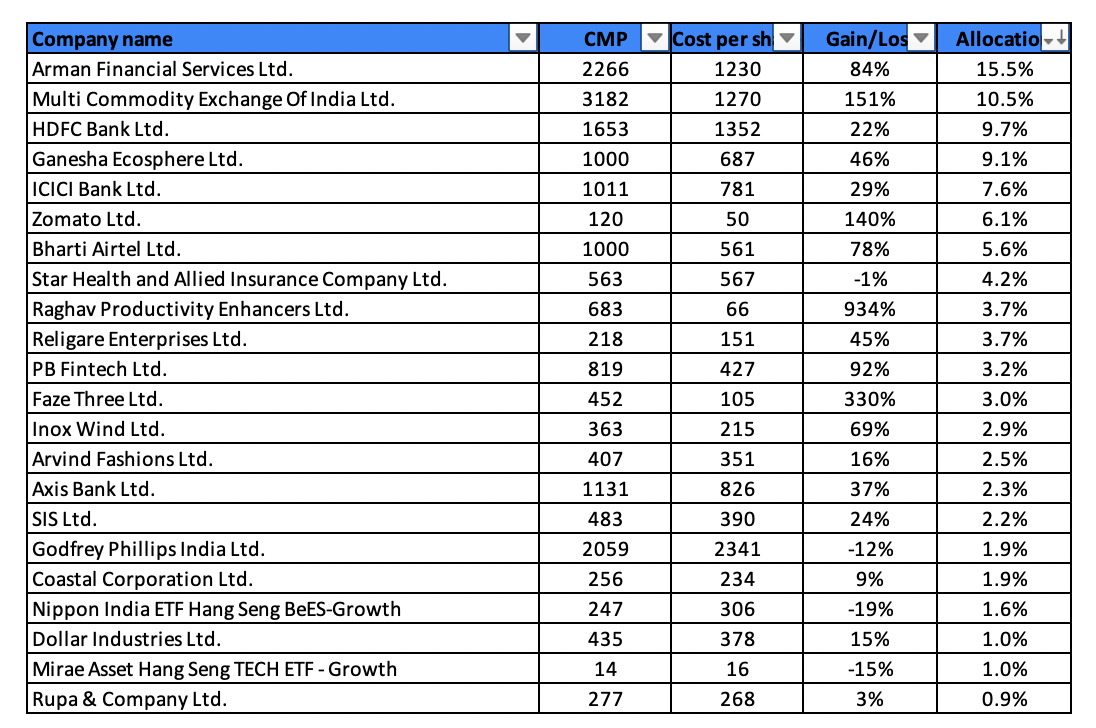

Arvind Fashions: Bought this back post the Sephora sale and relatively splendid quarterly results (compared to peers). Same thesis as posted earlier in the thread Yash Portfolio Feedback – #16 by yrm91. 3 out of 5 brands that the company now operate are splendid and hugely profitable while the other 2 are a work-in-progress. Since the time I exited, the company has also done fantastic work on the Working Capital side. I expect 12-15% revenue growth here and think fair value is >2x P/S (even including minority stakes) vs 1.2x today.

-

Bought Inox Wind: Cyclical Turnaround bet. The wind energy has gone through a horrific 5-6 years which started with a few regulatory changes and aggressive bidding on the part of power developers. This has also led to industry consolidation; only those players who could support the companies could survive. Wind power capacity addition slowed from 4GW to <2GW over the last 5 years. In the recent past, govt has put more emphasis on the wind power sector. Number of initiatives such as 1) 10 GW annual project tendering commitments, 2) Pooled power tariffs, 3) Hybrid Policy & 4) Green Open Access are expected to lead to a revival of the industry. I expect capacity additions to grow 3-4x in the next 3 years. By FY27, Inox Wind could be executing ~1GW of projects annually. This would translate to revenues of 7500cr and EBITDA of ~1000 cr plus the stake in the asset light O&M subsidiary. These numbers could translate into a M.Cap of 20-30k cr by FY27 for the consol entity.

-

Added Godfrey Phillips: Credit @harsh.beria93 for this one. A low risk medium term opportunity. Company is a beneficiary of the Russia-Ukraine war which has re-oriented trade toward India. Bulk of the revenue growth of the company is due to exports which have scaled 3x in the last 2 years. Domestic high margin business has also recovered smartly from Covid. Good place to park money while I look for new ideas.

Sells:

- Indiamart: Was shocked at the supplier additions number in the quarter gone by. They were the result of both higher attrition and lower gross additions. The lower gross addition is especially concerning given the large investment the company made on the distribution side in the last 18 months. These could still be temporary aberrations based on recent prike hikes. However, I prefer to wait on the sidelines to confirm that. Long term value creation here has to come from volume growth and any data points that put a doubt to that is a big blow to the thesis. Supplier additions recovering to 5k would cause me to relook again.

General thoughts: A lot of positions are now starting to slip into sell territory on account of valuations where expected returns fall below 10%. These are Raghav Productivity, Faze Three, even Inox Wind and MCX post the large rallies. On the flipside I am struggling to find many pockets of opportunity other than the large banks. Rural economy related stocks is an area that I have started looking at. General pessimism can be seen here which is reflected in the stock prices. Inflationary pressures easing as well as election related short term income boost could see a rural recovery in the next year. Some bit can already be seen in rising 2W volumes. However, there are a lot of discretionary consumption stocks in this universe: underwear companies (already owned), apparel companies (VMart), rural focussed FMCG companies (Bajaj Consumer, Emami), tractor companies, etc that are available at reasonable valuations.

| Subscribe To Our Free Newsletter |