Kama holding

Earlier I ignored the SRF but now I think I have got few answers and also destocking seems to be bottoming out.

My answers

- Even after the patent is expired, innovator have process patent through SRF like companies which can keep the molecule margin high for 3-4 years more.

- The fluropolymer Capex is just near to 500 Cr and it has got delayed though they seem hopeful as per recent management meet. It is less than 20 percent of the capex. Then downside due to capex addition is limited.

- Size of the opportunity is looks high now as they seem to have entered the pharma custom synthesis which is huge.

Industry structure

Refrigent cagr – 7.9(fortune business) and 5% bloomberg

Flurochemicals – 5%

Fluropolymers – 5.2(fortune business)

Nearly 30 percent revenue is contract based whose margin are non fluctuating

Debt

Debt is Low and manageable

Growth

Huge capex majorly in custom synthesis and chemicals

Dividend opportunity will be high in Kama holdings

Product mix change towards high margin and stable margin products like agrochemicals custom synthesis and chemicals

Rerating

Chances of rerating is high as promoter needs to earn money and hence kama holdings discount will narrow

Margin expansion

Not there in short term as capacity is being commissioned(3 – 4 years)

Tailwinds

Capex and more than doubling of net block. (Long term)

Entry into floropolymers(Long)

Entry into pharma cms(long)

PI industries receivable has increased with good sales in Q2 FY24 and SRF has delayed the shipment. Q3 might be better as SRF has more stringent revenue recognition than PI industries(short)

After the inventory destocking stops, it margin might revert as its chemicals product are not too much dependent upon china. (Medium)

Moat

Patents in agrochemicals

Cow lost advantage in refrigerant

Negatives

Industry growth is single digit

Not sure when old agrochemicals molecule will expire(Process patent is there after the patent gets expire)

Not sure whether the process is PFOS free(yes it is as per the management meet notes)

Gujurat florochemicals have capitive mines but SRF does not have it, therefore may face margin pressure from Gujurat flourochemicals in flouropolymers. China has stopped procuring the fluorspar from their mines and hence it bring it on equal playing fields.

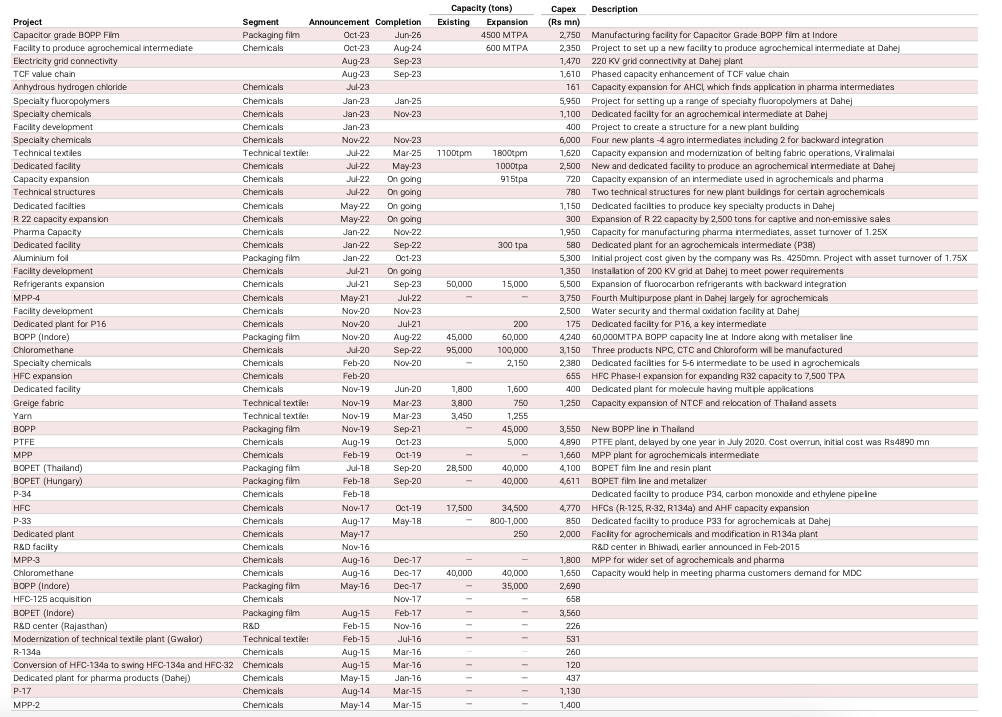

Upcoming Capex and past capex

Source Kotak

| Subscribe To Our Free Newsletter |