Recent analysis

Fundamental analysis

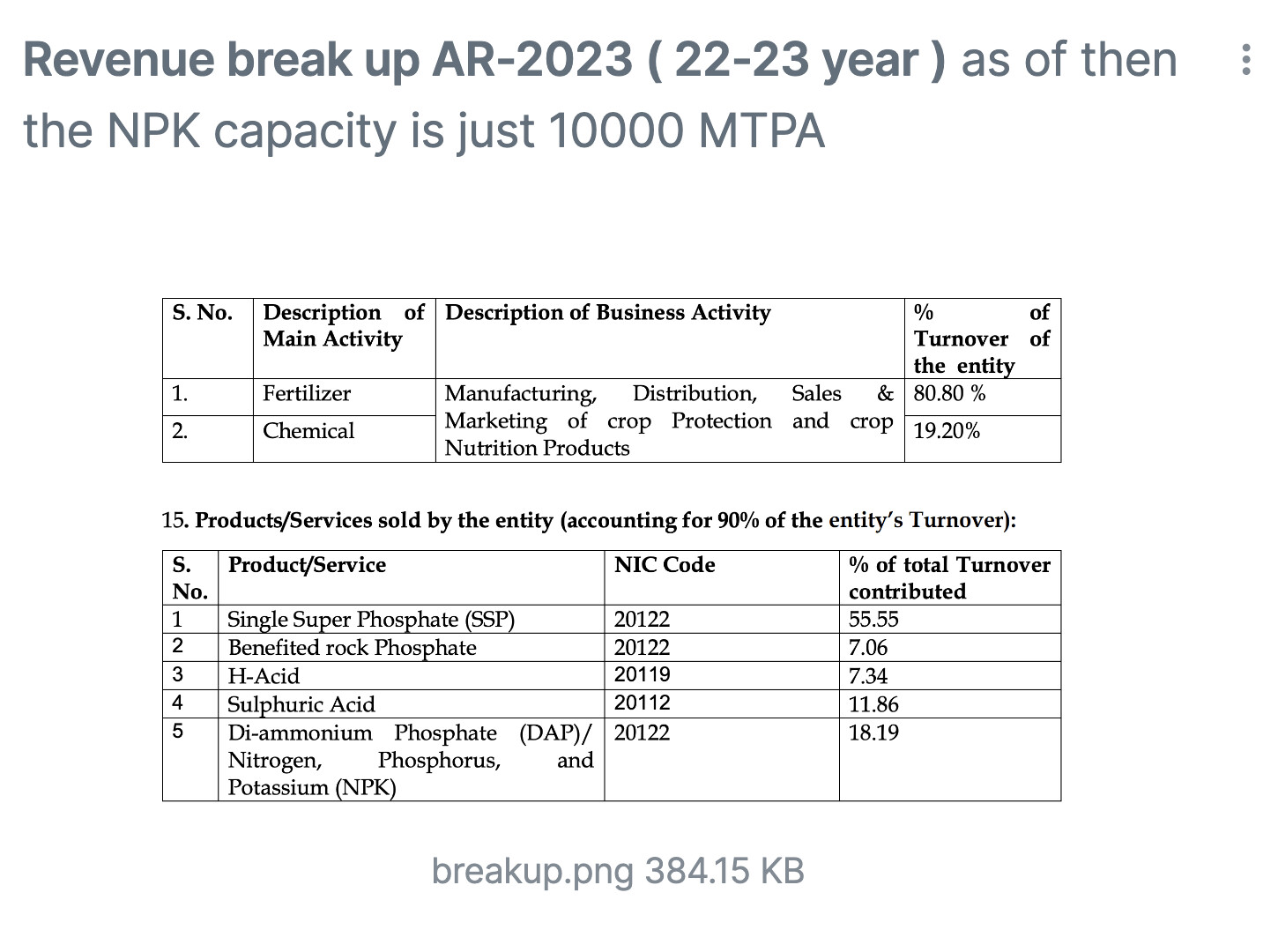

Last year revenue break up

.

.

Revenue Growth factors

.

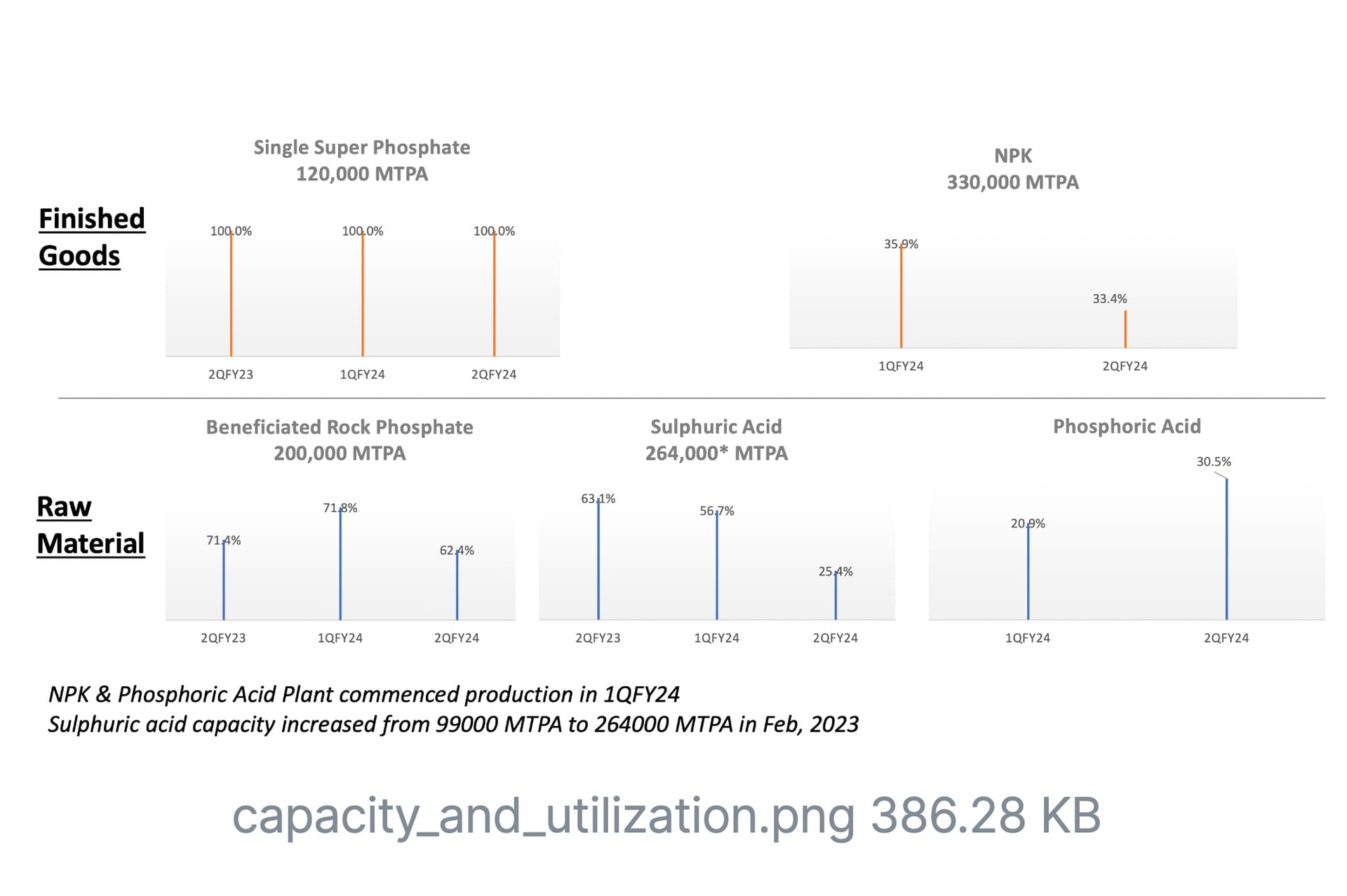

The NPK/DPT utilisation levels far from full (33% ) if increased to 80% the profit will increase 100 CR annually which is a minimum rough estimate

Cost production : 18000 / ton

Selling price : 25000 / ton

(Rs. 25,000/ton – Rs. 18,000/ton) * 300,000 MT * (80% utilization) = Rs. 168 crore

.

Last quarter profit at ( 19 crores )

.

Macro economic factors

1.Russia resumes fertilizer trade with United States, ends discounts prices ( discount wast 80$ per MT ) to India ( Which will reduce imports to india, Currently Krishana does’t have any export business )

2.Union Cabinet approves NPK fertiliser subsidy for 2023-24 rabi season ( There won’t be any drop in demand and price reduction at least until the 2024 election, Currently NPK is sold at 1350 MRP per 50KG which is fixed price)

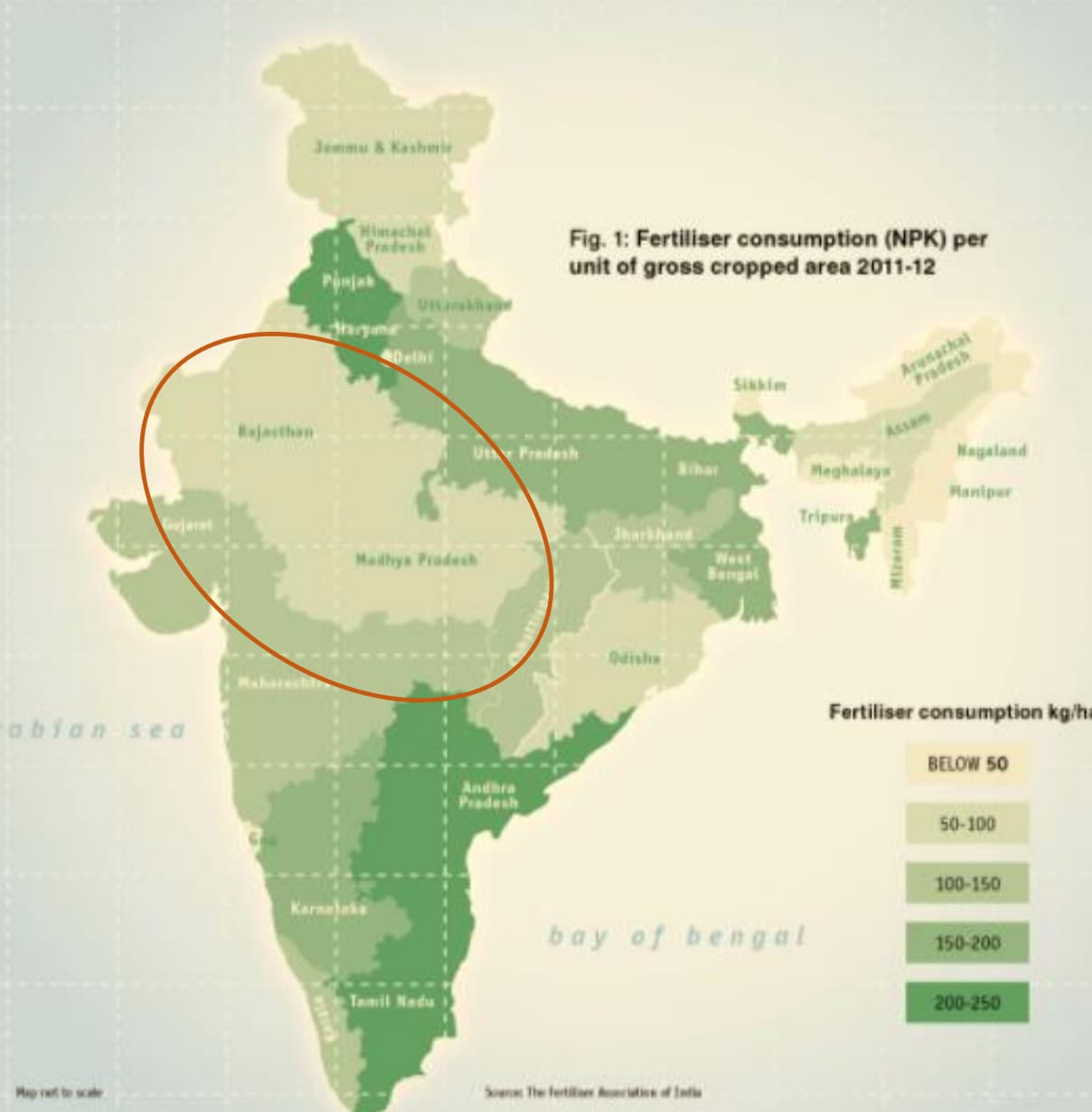

3. Fertilizer consumption in their major operating regions is very low ( as of 2022 ) there is room for growth there

.

Non-determinable Positive factors

Lot of insider trade activities by promoters ( Buying from market )

OSTWAL PHOSCHEM ( INDIA) LIMITED => Increased ownership From 64% to 65.43%

.

Nirmala Realinfrastructure Pvt Ltd bought 0.5% ( 5 crores )** at average price around 225 between past 5 months ( Owned by son of ostwal group). They have sold their significant amout of shares madhya bharat agro company,

RAJENDRA PRASAD OSTWAL => director of Nirmala Realinfrastructure Pvt Ltd ( Increased From 200 shares to 8900 shares)

.

NITU JAIN => ( mentioned as ostwal Group director in linkedin, but not sure ) ( increased from 5000 – 18000 => 30 lacks )

EKTA JAIN => Increased from (60000 to 66000 )

Pankaj Ostwal => son of ostwal group ( increased from 5000 shares to 8500 ) avg price 230

Ashok Kumar Parakh => from ( Increased from 5000 – 9000 shares ) at 225 price

Possible Negative factors

1.Adverse impact of any regulatory/policy change ( reduction in subsidy will lead to lower demand ). ( Reduction in MRP price of fertilisers, fixed at 1350 for NPK )

2.Raw materials are imported from JORDON for Rock Phosphate with long term agreement ( Any geo political factors will affect import )

.

Technical analysis

Trading at higher than 5Y Median of 25 PE, Currently trading at 33 PE ( Based on recent quarter EPS trading at 18 PE )

On balance volume is steadily growing

.

Disclosure : Not invested,

| Subscribe To Our Free Newsletter |