I don’t think “P/E of 16.5 X and an EV / EBIDTA of 7.7 X” is the right way to look at it. Since the company has already announced its plans to exit the overseas businesses, these investments should be looked upon as Assets Held For Sale. And so Time Technoplast should be valued on Standalone earnings, plus some value added for continuing subsidiaries such as TPL Plastech and the battery business.

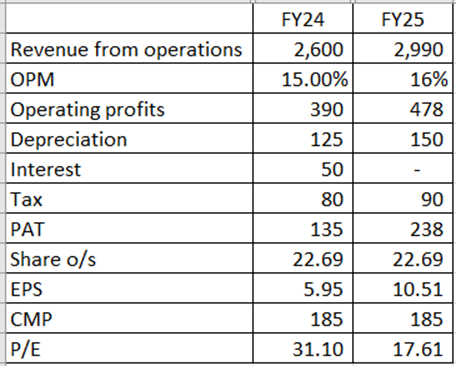

Using Standalone earnings, a crude back-of-the-envelope calculation for FY24 suggests Time Technoplast may make something like Rs.2600 crore revenues and Rs.135 crore PAT, which gives an EPS of Rs.5.95 and a P/E of around 31 X. Benchmark P/E range for this group can be considered as 16 – 22 X based on where peer group companies trade.

The bigger jump in TTL’s numbers will come in FY25 when – if all goes as per plan – margins will improve further, debt can come down to zero or near zero and EPS can breach Rs. 10 plus. At this level, current P/E comes to 18 X which is in line with the sector benchmark.

Rough estimates (Standalone):

(Disc.: Holding)

| Subscribe To Our Free Newsletter |