I have been hoping that price dips a bit more and I can buy more. The last time I bought was in Feb 2022, so its been a while. Every few years, PI sees a 30% price drop and I try to buy each time that happens.

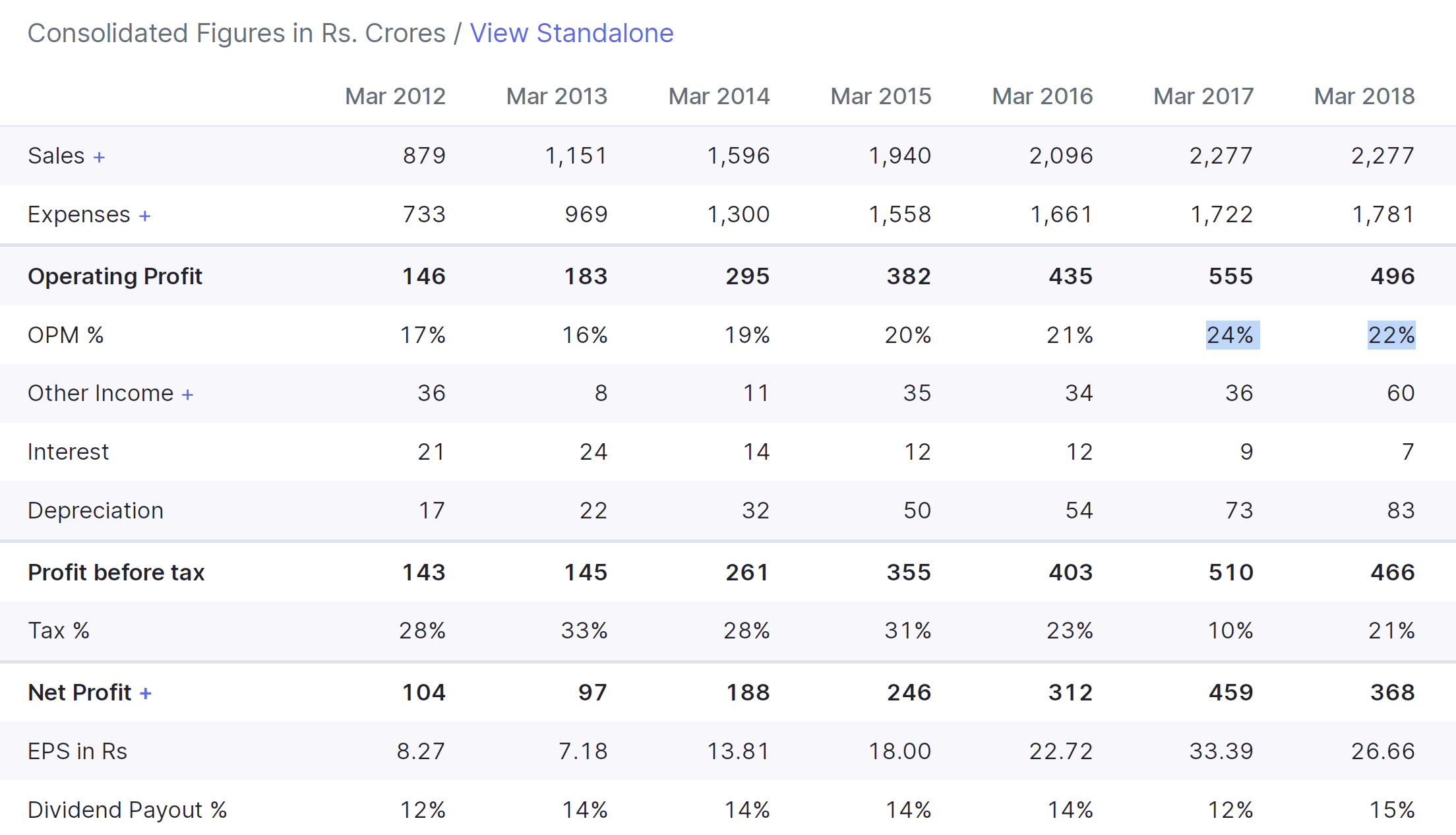

Coming to pyroxasulfone, broker reports suggest that it contributes 45-50% of their CSM business which brings in a concentration risk. The last time this happened was in FY17, where pyro was a large part of their CSM business. As a result, their FY18 nos were quite muted and stock also underperformed for a couple of years.

The key difference this time is they have a much larger product basket, which management is hoping can fill the void (if demand for pyro stagnates). Their CSM product basket has increased from 10 at that time to 20-25 now. Also, pharma is a growth driver and is higher gross margin compared to agchem CSM. I actually feel more bullish about their future prospects now, than in 2022 when I had last bought.

Much higher growth, Dharmaj is growing at 25-30% vs Dhanuka growing at 10-12%. On business front, Dhanuka is probably the best managed domestic agchem co.

| Subscribe To Our Free Newsletter |