Gujarat State Petronet Limited – A business analysis

Background

As businesses go, this one is as simple as it gets. GSPL owns and operates gas pipelines and with about 2700 km of pipelines in 2023, it has the 2nd largest pipeline network in India after GAIL (16000 km).

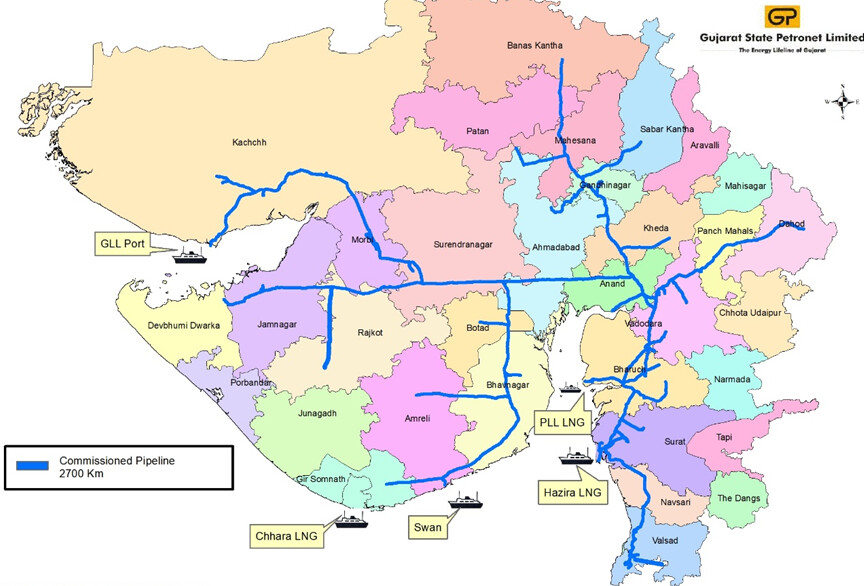

Practically all of India’s LNG is imported in Gujarat and a considerable amount of domestic gas production is also sourced through Gujarat. Furthermore, it is also the highest natural gas-consuming state, with around 40% of total domestic natural gas consumption in the country. All these factors translate into steady utilisation of GSPL’s natural gas transmission pipelines. See Figure 1 for details.

Figure 1: Gas pipeline network in Gujarat along with LNG re-gassing facilities.

GSPL is a pure natural gas transmission company operating on an open access basis; and it does not purchase or sell natural gas. Open access enables natural gas consumers to separately negotiate their natural gas supplies from several suppliers. Thus, there is no risk related to natural gas prices other than the fact that high prices might reduce demand.

The business has a moat in the sense that no one is going to come and build out a pipeline where you already have one (the right to build pipelines is based on a bidding process). Plus, you build out the pipeline in today’s Rupees and can use it for about 50 years (of course there is some maintenance capex), earning in future Rupees with no competition. One can’t raise the rates indiscriminately though since there are government regulations capping the same. Nevertheless, a simple, good business.

Business drivers

GSPL’s operating business is simple enough. What throws a spanner in the works though is that GSPL also owns:

-

54% of Gujarat Gas Limited (GGL): India’s largest city gas distribution player with presence spread across 44 Districts in the State of Gujarat, Punjab, Rajasthan, Haryana, Madhya Pradesh, Maharashtra and Union Territory of Dadra and Nagar Haveli. A Subsidiary

-

52% of GSPL India Gasnet Limited (GIGL) for development of Mehsana – Bhatinda and Bhatinda -Gurdaspur Pipeline Projects**.** A Joint Venture.

-

52% of GSPL India Transco Limited (GITL) for development of Mallavaram – Bhopal – Bhilwara – Vijaipur Pipeline Project. A Joint Venture

-

27.05% of Sabarmati Gas Limited. An Associate

-

27.05% of Guj Info Petro Limited. An Associate : Too small so just ignored in the analysis.

GSPL’s operating business:

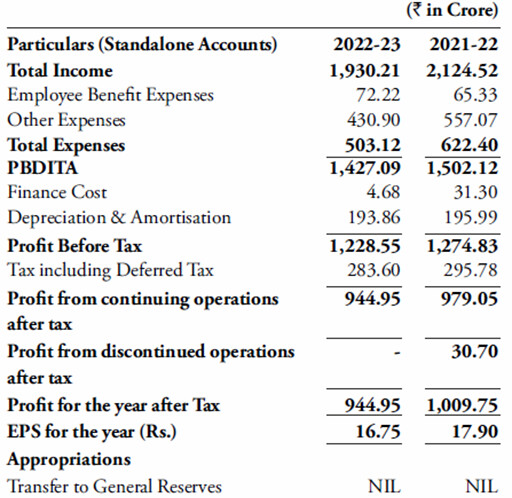

The operating business makes INR 9440 million a year and its maintenance capex is about INR 2000 million (Depreciation and Amortization). Table 1 shows details.

Table 1: Income statement of GSPL’s operating business

GGL – Gujarat Gas Limited

7000 million of the profit of GGL stays within GGL (non-controlling interest) and the rest is attributed to GSPL so about 8000 million. Table 2 shows details. This is a good business to own – high ROIC of around 30% and moated!

Table 2: Financial statements of GGL

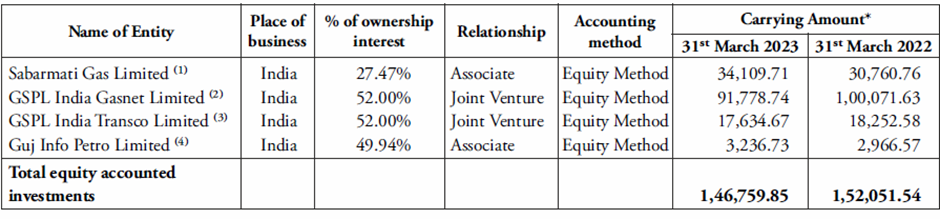

The joint ventures and the associate

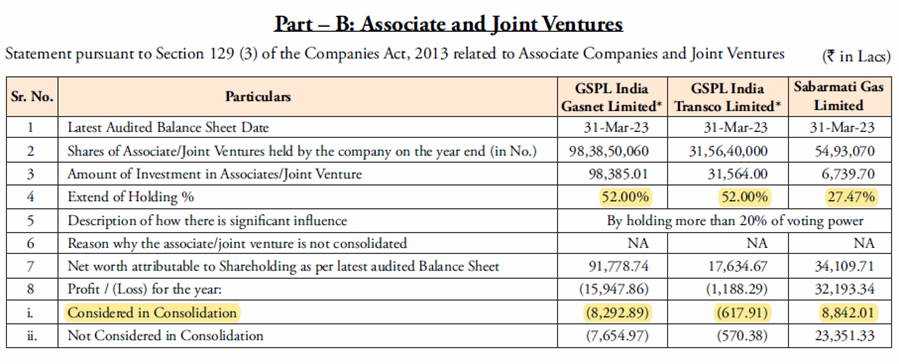

Basically, the profit of the Sabarmati cancels out the losses of GSPL and GIGL, so net-net, you can just ignore these on the income statement. See Table 3 for details. This does not mean that they don’t have value in the balance sheet though, so let’s look into that now.

Table 3: Key financials of associate and joint ventures.

According to the annual report of 2023, 1254 km of the pipeline are operational (Figure 2). Some parts in Punjab are still to be built because of farmer’s protests etc. The capacity is supposed to be 30 MMSCMD (link here) but, according to the annual report 2023, only 1242.26 MMSCM of natural gas was delivered during the year (divide by 365 to see per day figures and that the utilization is barely 10%). Likely this is because the pipeline was operational only in 2022 and demand centers still need to ramp up. Also note that this project had a delay of about 8-10 years – it was expected to be completed in 2014.

Originally GIGL was to build the pipeline from Punjab to Jammu as well but that will now be built by IOL. Someday that will get completed and it’s a tailwind for GIGL as more gas will flow through its pipelines to Punjab.

Figure 2: Map of the GIGL pipeline

In GITL, the initial section of 365 Kms Pipeline and associated facilities from Andhra Pradesh to Telangana is in operations since the November 2019 (Figure 3). GITL transported 586 MMSCM of gas in FY 2022-23 registering significant growth of over 32% over previous year volumes (444 MMSCM).

The capacity is supposed to be 54-78 MMSCMD (link here). Again, this was supposed to be completed in 2014 but still something like 1500 km remains to be developed (right part of Figure 3).

Figure 3: The GITL pipelines. Left = completed; Right = Under development.

Just as comparison, GSPL has transported 9253 MMSCM of gas during the Financial Year 2022-23 while GIGL and GITL together transported only around 1800 MMSCM. There is a lot of room for growth!

As can be seen from Table 3, with about 880 million in profit to GSPL, it is small and can be ignored.

Analysis of Financial Statements

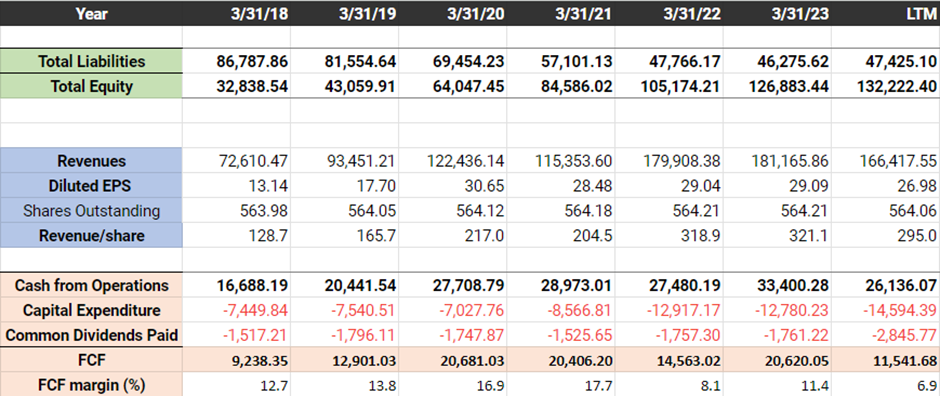

Table 1: Key metrics from financial statements in millions INR over the past five years.

The numbers from Table 1 are fantastic – high ROIC of 26%, equity, EPS, revenue, FCF growth rates all about 15%, low debt, dividend that is easily payable. Plus, the company is cheap at 10 times FCF.

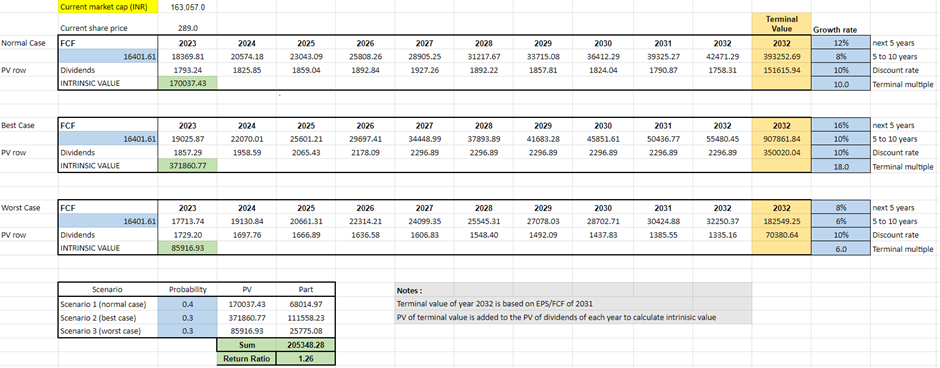

Table 2: A DCF valuation for normal, best case and worst-case scenarios using FCF as input.

Just valuing the company on FCF of 16000 million (which incidentally is the profit of the operations arm plus stake in Gujarat Gas limited) in a DCF shows that the company is fairly valued for a 10% return (normal case).

In this valuation, we are basically ignoring the joint ventures – GIGL and GITL since they contribute nothing to FCF as they are loss making. Someday they will be completed (GIGL likely will be fully operation in a year or two). GITL might take another 10 years, who knows! For instance, if GIGL and GITL each carry the same volumes as GSTL’s operational arm and are equally profitable then each should make approximately INR 10000 million (see Table 1), Since GSPL owns 52% of each, it would mean that GSPL’s profit would go from the current 9440 + 8000 (GIGL’s operations + GGL) to approximately 28,000 million which is six times PE on the current market cap of 163,000 million.

Of course, there are risks that the pipelines take too long, tying up capital although one could argue that even with long delays, the company had a great ROIC. GSPL is also liable for cost overruns so there is risk.

There is another weird thing going on considering that the Joint Ventures are accounted for with the Equity Method of accounting which means that any losses they suffer are subtracted out from the original carrying amount (i.e., equity invested in the JVs) in the book value on the balance sheet. This is why GIGL and GITL are reducing book value of GSPL if they lose money – see Table 4 from 2022 to 2023. A reduction in book value by a 1000 million (just GIGL and GITL) would reduce equity by less than 1% a year considering that equity is 132,000 million. Over a few years, it does add up so likely the book value is understated. Currently it is Rs 176/share.

The reverse happens when the JV’s are profitable – i.e., the book value increases.

Table 4: Accounting via equity method for joint ventures and associates (in lacs).

Investment thesis

What can I say – from a purely business perspective, a good growth rate for all metrics, high ROIC, book value gives a floor to the price.

From a pricing perspective, just the 54% stake in GGL is higher than the market cap of GSPL. You are buying the 2700 km pipelines of GSPL, the pipelines of the JVs for free. Of course, GGL can have a PE contraction, and this might change, so buy only if you like the core business.

Company news

Nothing much going on – in fact a criticism is that they don’t share too much about the business.

Catalyst

If this was not a government owned company and the management was smart, they could sell some GGL, and do buybacks. And create a strategy to either fully absorb the JVs as subsidiaries or spin them off. In that case there could be a 3-5x increase in price over a 5-year period. Alas, considering it is a state enterprise, these are unlikely to happen in a predictable way. So, there is no catalyst, even though value is there. Seth Klarman would probably not buy this. That does not mean it can’t double in a year – its just not possible to predict.

So, I would say, buy when it is cheap (whatever you find to be your margin of safety), perhaps nibble into it over time and hold on forever and wait for dividend increases which will come, maybe in 2 years, maybe in 10. I would not be surprised if 20 years from now, you can get a 25% dividend yield on current cost. Perhaps, consider selling the business only if it suddenly pops or if you find an equally good, predictable business that is a non-government entity.

| Subscribe To Our Free Newsletter |