Relooking at some of the key statistics from BSE for the quarter ended December 2023:

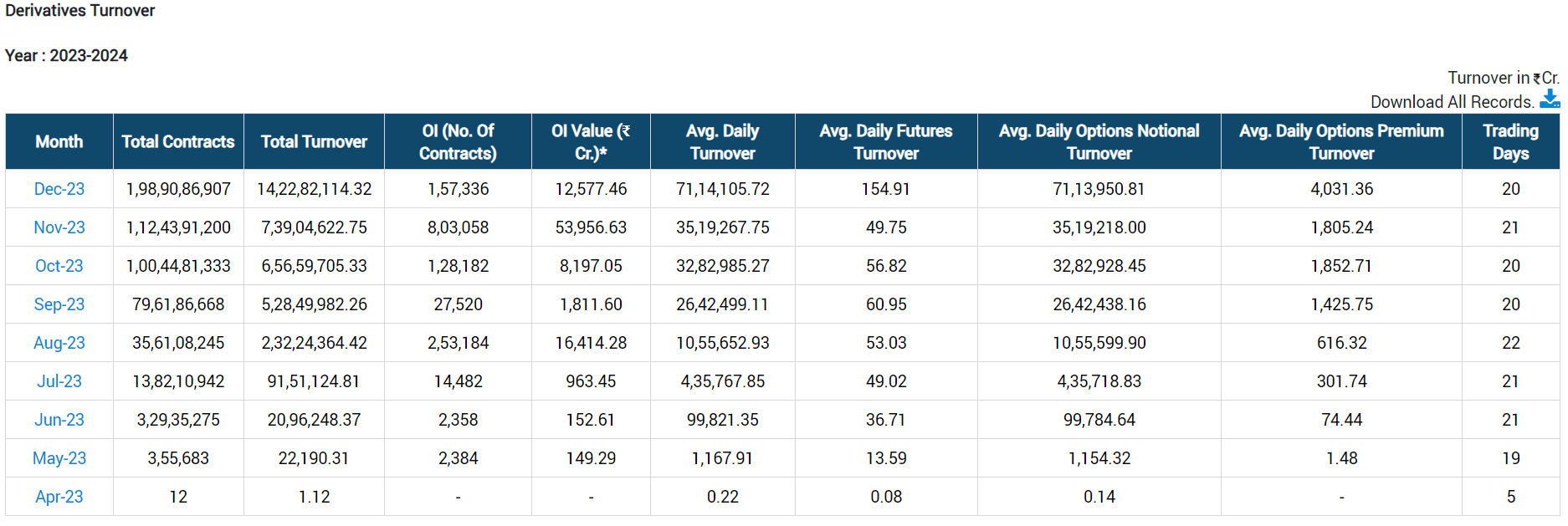

Derivatives:

The numbers are growing at a brisk pace irrespective of significant change to charges from 1st of November. Market participants apatite for trading in Sensex and Bankex derivatives are growing week after week. While the tired pricing structure makes it difficult to arrive at the expected revenue for the quarter, my rough estimate of revenue from this segment is that it should exceed Rs. 15 Crore for the quarter (assuming average realization per crore of delivery trade to be Rs. 1500).

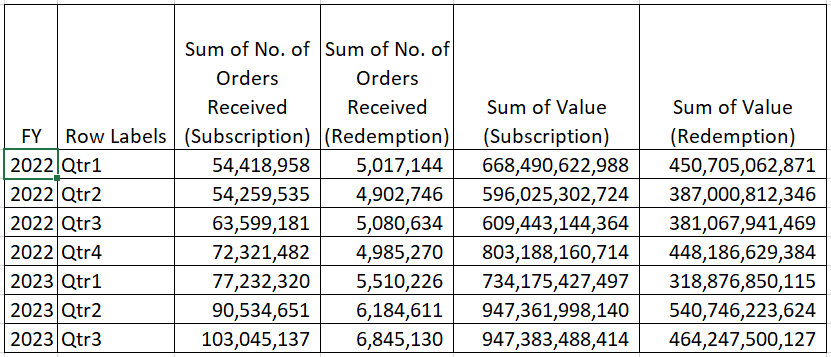

Star Mutual Fund:

The subscription orders grew by about 14% as compared to Q2 2023 and by 62% compared to same quarter PY. The revenue from this segment will grow in line with volume.

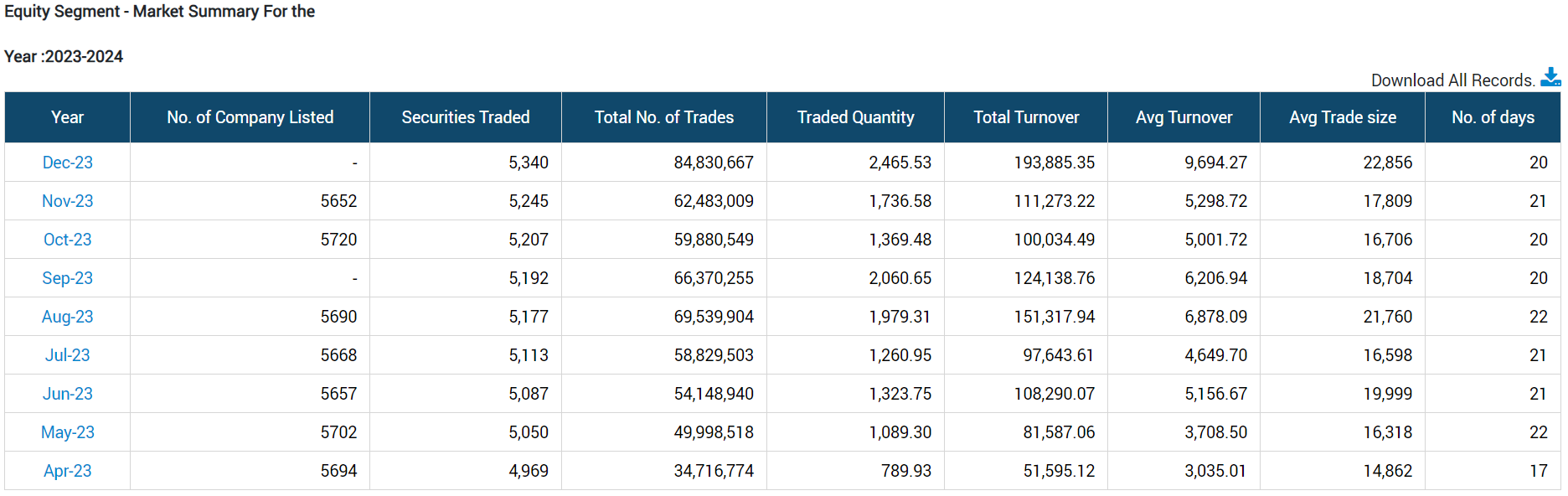

Cash segment:

The segment seems to have got a rub-off from the robust growth in derivatives resulting in a 6% growth in number of trades as compared to Q2 2023. The revenue growth should be robust.

IPO Market:

The number of new companies listed on BSE during the quarter broadly remained same as last quarter and accordingly the revenue from the segment should be stable when compared to Q2 of this FY.

Other observations:

- Buyback that was announced during the previous quarter failed due to lack of participation on account of sudden spike in share price during the current quarter.

- Commodity and Currency markets are not really showing any real momentum.

Overall I expect the results for the current quarter to be the best one from the time BSE got listed. Let’s wait for fine prints and management commentary once the results are published.

AJ

Disclaimer: Remain invested. Views are biased.

| Subscribe To Our Free Newsletter |