Points from DRHP:

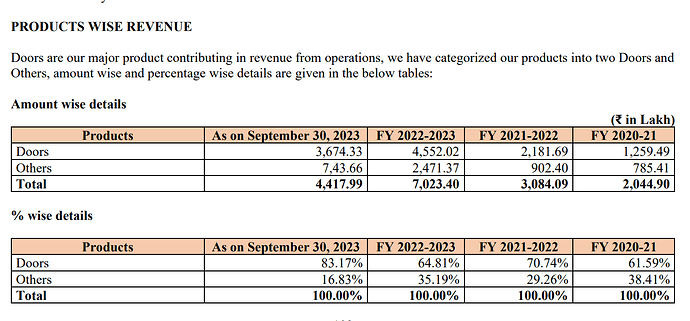

- Sales Structure:

As per the latest sales bifurcation, it looks they are moving completely to manufacturing.

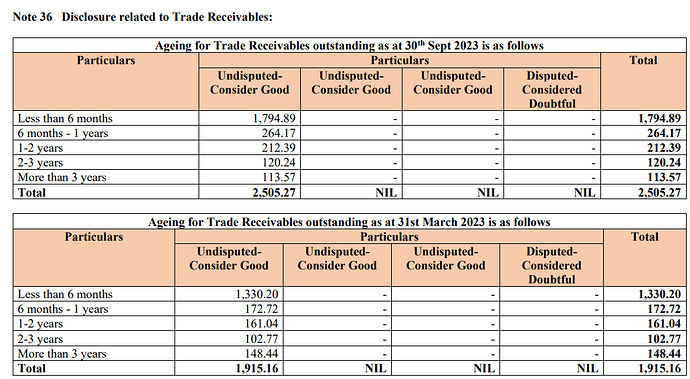

- Receivables Ageing:

In absolute terms, things are mixed but overall age is increasing.

-

Product bifurcation:

Supporting point number 1, company is prioritizing manufacturing of doors.

-

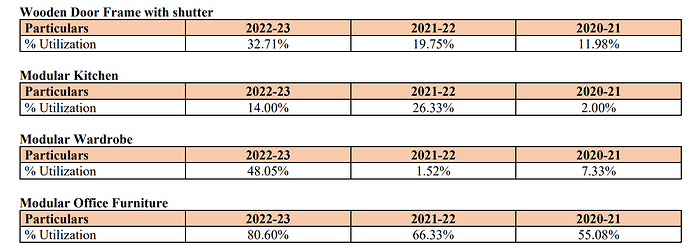

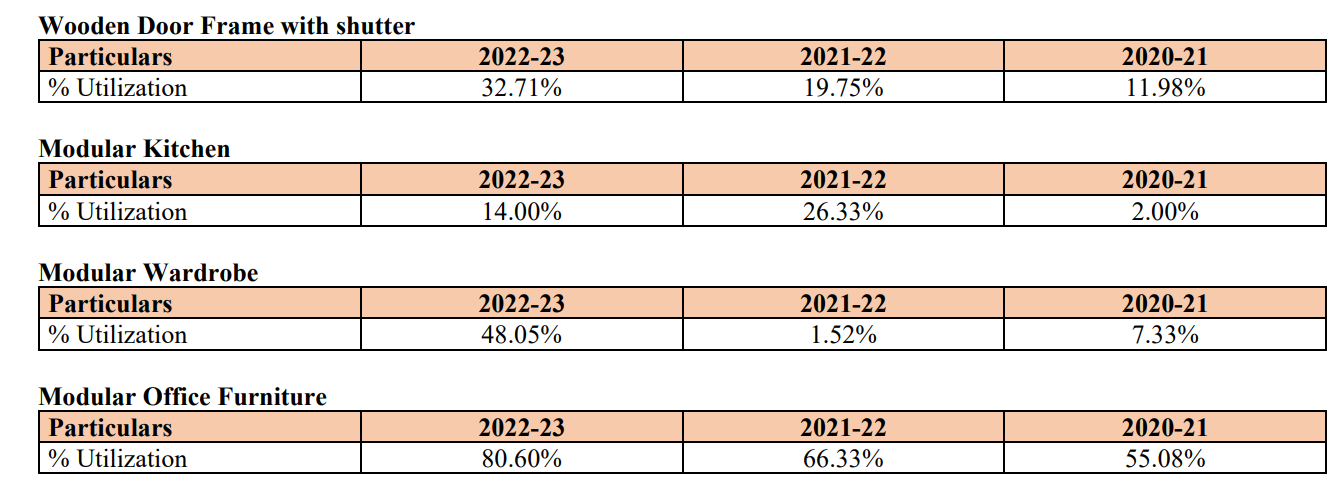

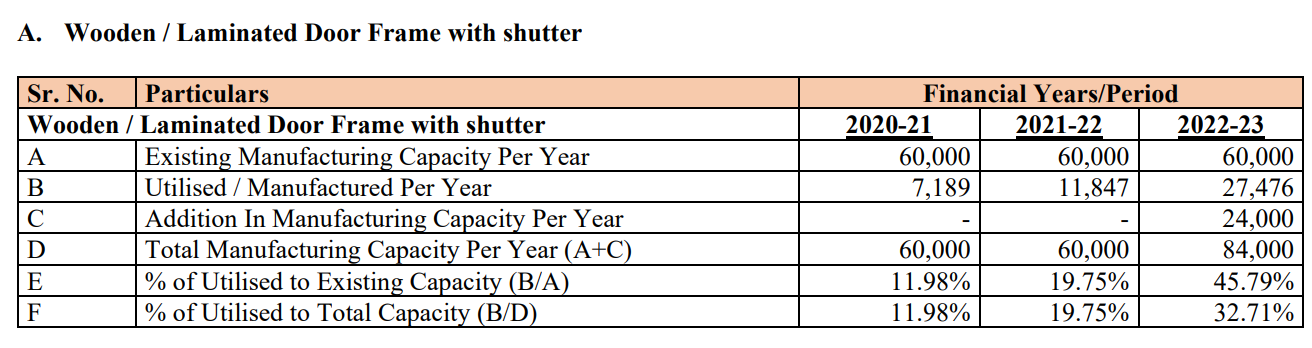

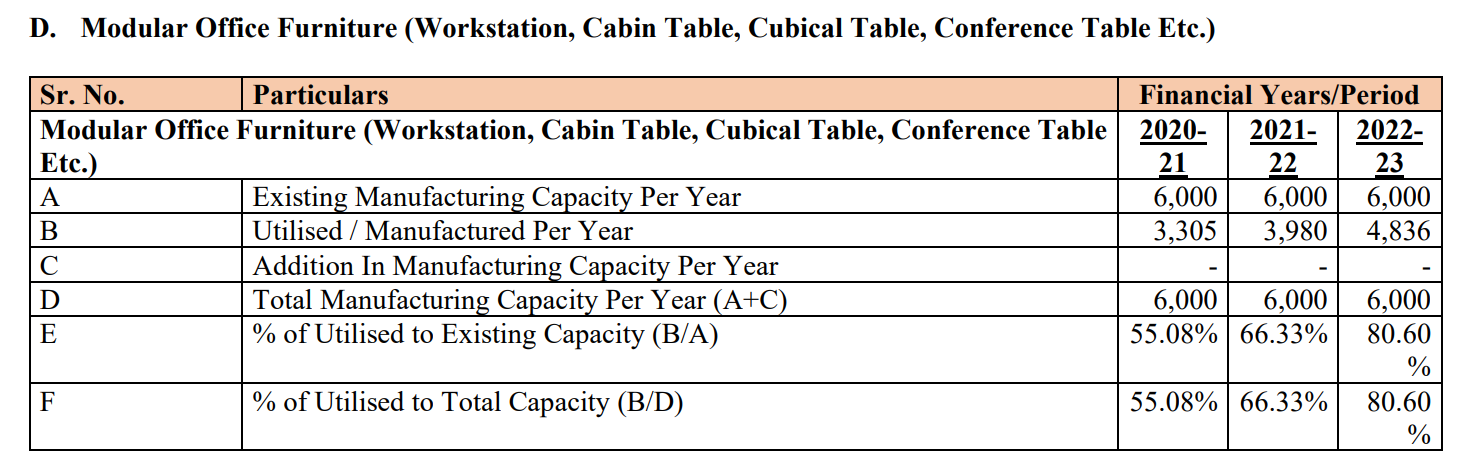

Capacity Utilization:

Somewhat of erratic utilization in Modular Kitchen and Wardrobe.

Detailed Utilization:

The capacity utilization leaves much potential, at the same time raises questions for such low utilization levels and yet the company is planning for expansion (although the comparison also includes Covid period)

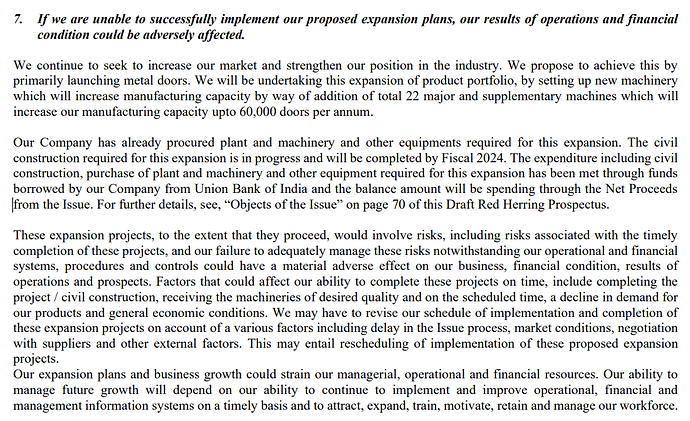

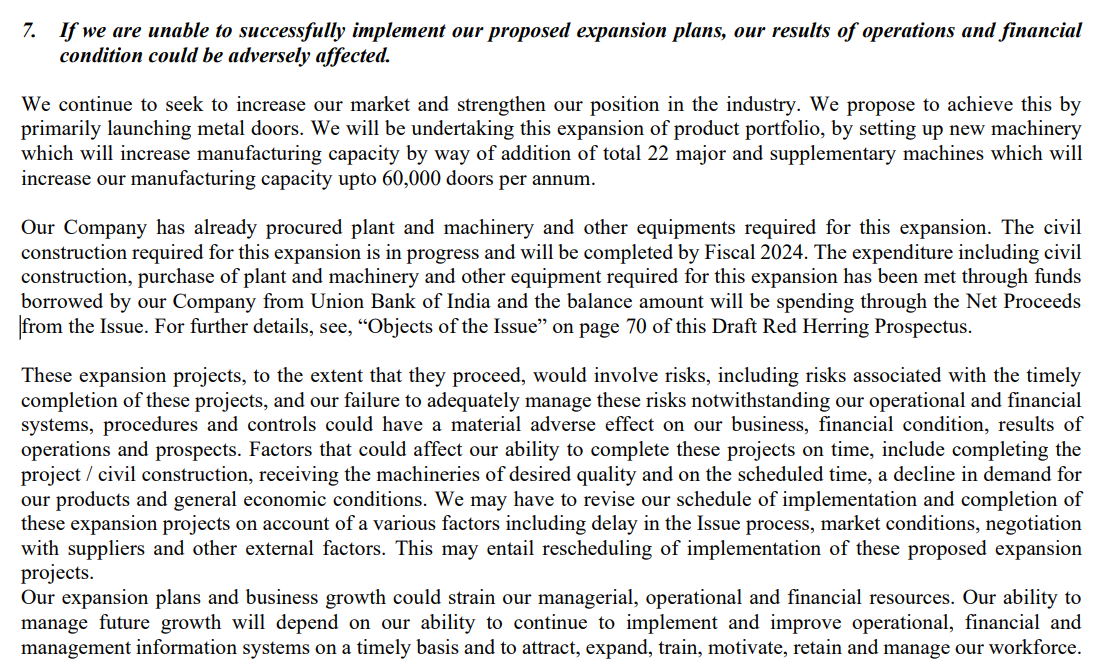

- New Product (Capital Expenditure through FPO):

Execution remains a crucial part here, but the point that valuations are slightly decent gives this a good look. The pricing of FPO matters a lot and the willingness of promoters to dilute their stake at a certain level remains a question.

The company doesn’t communicate much at exchange.

The increase in remuneration from this year in addition to high related party transactions are a thing to monitor.

On top of that, in FPO, the company didn’t reveal customer base. Order book was also absent. (mentioned in Credit Report)

| Subscribe To Our Free Newsletter |