@Aditya_Mittal Thanks for asking this question, I was also doubtful of their margin sustaining after Q4 FY23 result.

I don’t think there will be mean reversion to 15-20% as their product mix has changed. The operating margin in case of human NCE is more than 40 percent in peers. Check Suven for the example.

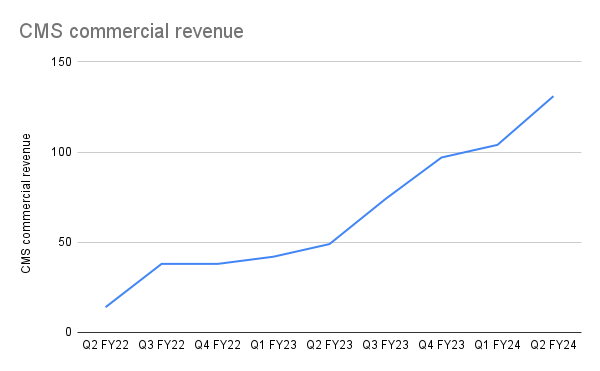

Considering 45 percent margin for the CMS business and 15 margin for their other business, the weighted average of margin comes out to be nearly 31 percent which is what they have attained.

It can obviously drop to 25 – 26 percent for some quarters going forward(as there is some economies of scale playing out) but it will definitely revert back to more than 30 percent once the share of the CMS business increases further and remain above a certain level.

Its revenue from the commercialised molecule from the CMS business is increasing QoQ for some time now. Hence product mix change is here to stay.

The volatility in the CMS business revenue is mostly due to the developmental molecule revenue which fluctuate on QoQ basis.

There can still be some quarters of the volatile earnings(which obviously is a buying opportunity) but as the share of commercialised molecule CMS business increases, the volatility in revenue will decrease going forward.

Other than this I think the KarXT optionality is not baked into the price currently.

Ex of KarXT optionality the valuation of the Neuland might seem on the higher side for some folks but with the KarXT optionality playing out, we are up for the surprise.

Disclosure: Please do your own research, I have a track record for being wrong.

| Subscribe To Our Free Newsletter |