Am not a deep learner, I study only at surface and if I feel the idea is worth it – then I do go for it.

Total digital payment transactions volume increases from 2,071 crore in FY 2017-18 to 13,462 crore in FY 2022-23 at a CAGR of 45 per cent: MoS Finance

Digital payments transactions reach 11,660 crore in current Financial year as on 11.12.2023

| Financial Year | Volume (in crore) |

|---|---|

| 2017-18 | 2,071 |

| 2018-19 | 3,134 |

| 2019-20 | 4,572 |

| 2020-21 | 5,554 |

| 2021-22 | 8,839 |

| 2022-23 | 13,462 |

| 2023-24 (Till 11th Dec) | 11,660 |

Credits :

- In 2017, UPI recorded a YoY growth of 900%, processing over 100 million transactions worth INR 67 billion.

- In 2018, the YoY growth was 246% with transactions worth over INR 1.5 trillion processed.

- In 2019, the YoY growth was 67% with transactions worth over INR 2.9 trillion processed.

- In 2020, UPI recorded an YoY growth of 63% with transactions worth over INR 4.3 trillion processed in December 2020.

- In 2021, the YoY growth was 72% with over 1.49 billion transactions worth INR 5.6 trillion processed in June 2021[5].

- At the end of the calendar year 2022, UPI’s total transaction value stood at INR 125.95 trillion, up 1.75 X year-on-year (YoY), as per the NPCI. Interestingly, the total UPI transaction value accounted for nearly 86% of India’s GDP in FY22[8].

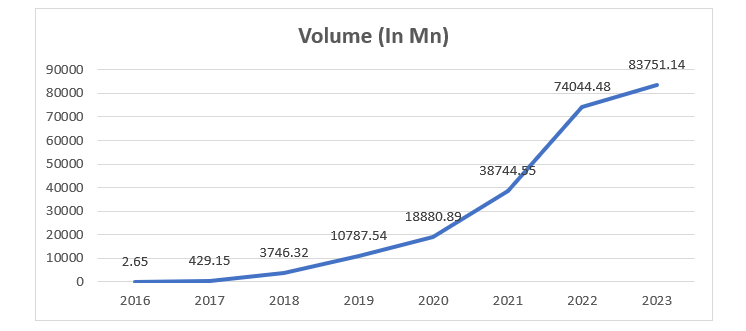

- At the end of the calendar year 2023, UPI’s total transaction volume stands on 83.75 Billion.

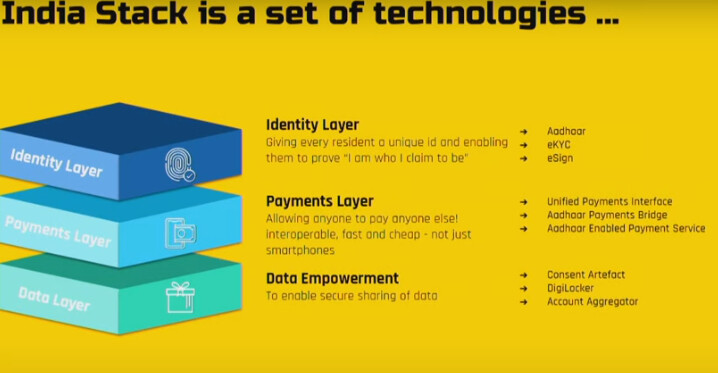

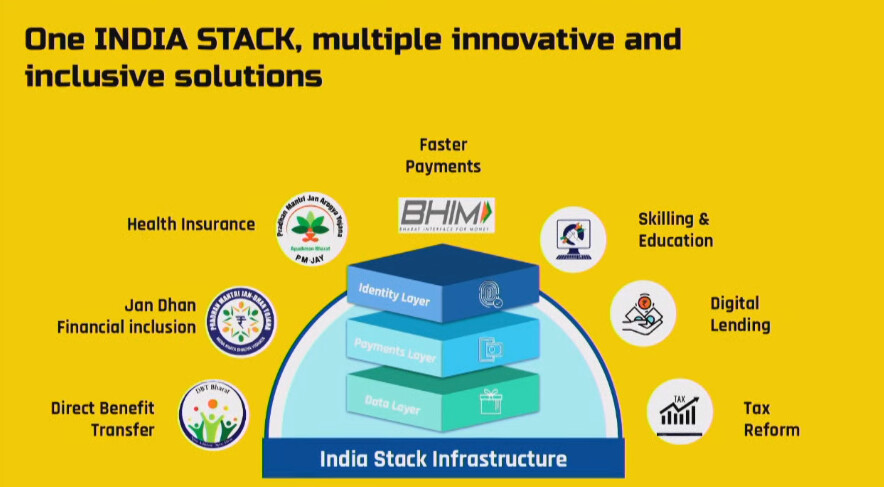

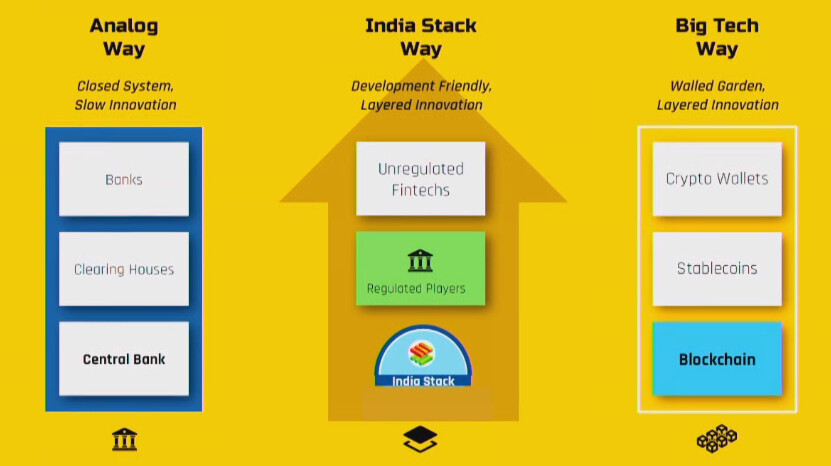

India is on a next leg of growth spurt – to account for this India has a Tech stack which is very well built and a brilliant way that has been put up.

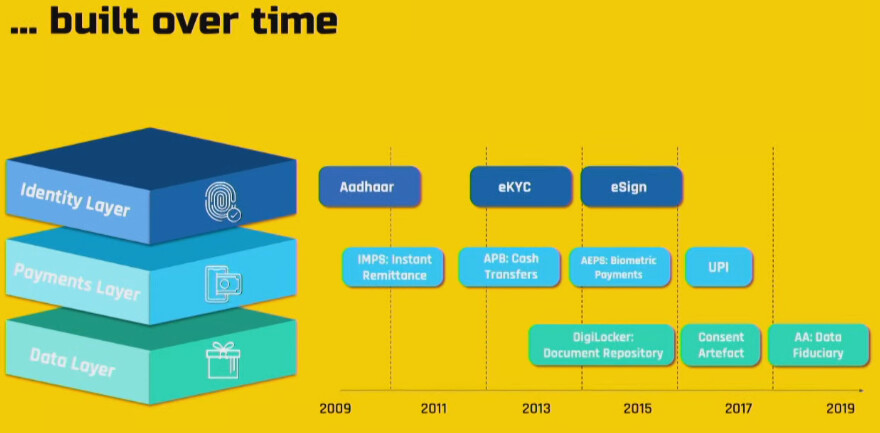

Now lets understand what happened from 2009 till now

Credits : https://www.youtube.com/watch?v=8PLEZmJ36y4&t=233s – Brilliant work done by Nandan Nilekani (Infosys) – thanks to him that we are much far ahead coming to the digital revolution

Why am saying all this?

1, If you know that we have a vey robust and a structured way of growth : tomorrow if anyone needs a loan – he/she can get it in minutes, by first giving their consent to the banks to authorize his/her aadhaar – get all details with respect to the credit score, credit profile etc etc and get loan approved immediate and loan amount transferred to Bank account.

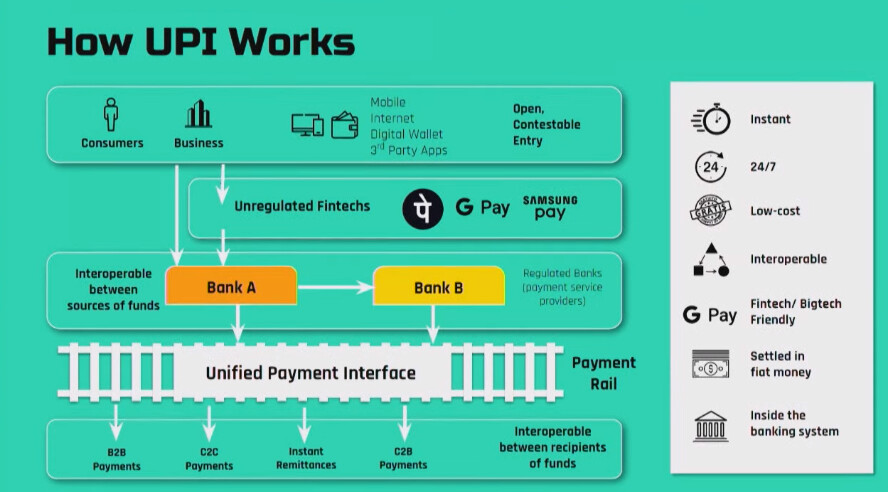

UPI has revolutionized the way that we work

Now more and more countries are planning to adopt the UPI system.

Everyone is talking about the consumer discretionary spending and so on and so forth.

From what I learned so far

- How much digital are we?

- What digital platforms that enables all these elements?

- Consumer Discretionary spending true but what platform? – ecommerce, merchant or elsewhere

- Which payment interface?

- What technology enables these?

If I consider Starbucks or Bigbasket

- Will you go out for coffee or would you like to shop from home

- What is the win win for both these parties here? – Its the payment interface

If payment interface then which?

- UPI

- Card

- Cash

- Online Web

Who are the companies that helps these?

- CC Avenuve

- Razorpay

- JustPay

- Paytm

- Phonepe

- Google Pay

Which area of basket they target

- Large Enterprise

- Medium

- Small

- Micro

One thing to note : No matter which way you go, the payment aggregators will benefit either if you shop from Starbucks on a weekends or Bigbasket on weekdays.

The business is cyclical but the payment need not be.-

Share your thoughts.

*

| Subscribe To Our Free Newsletter |