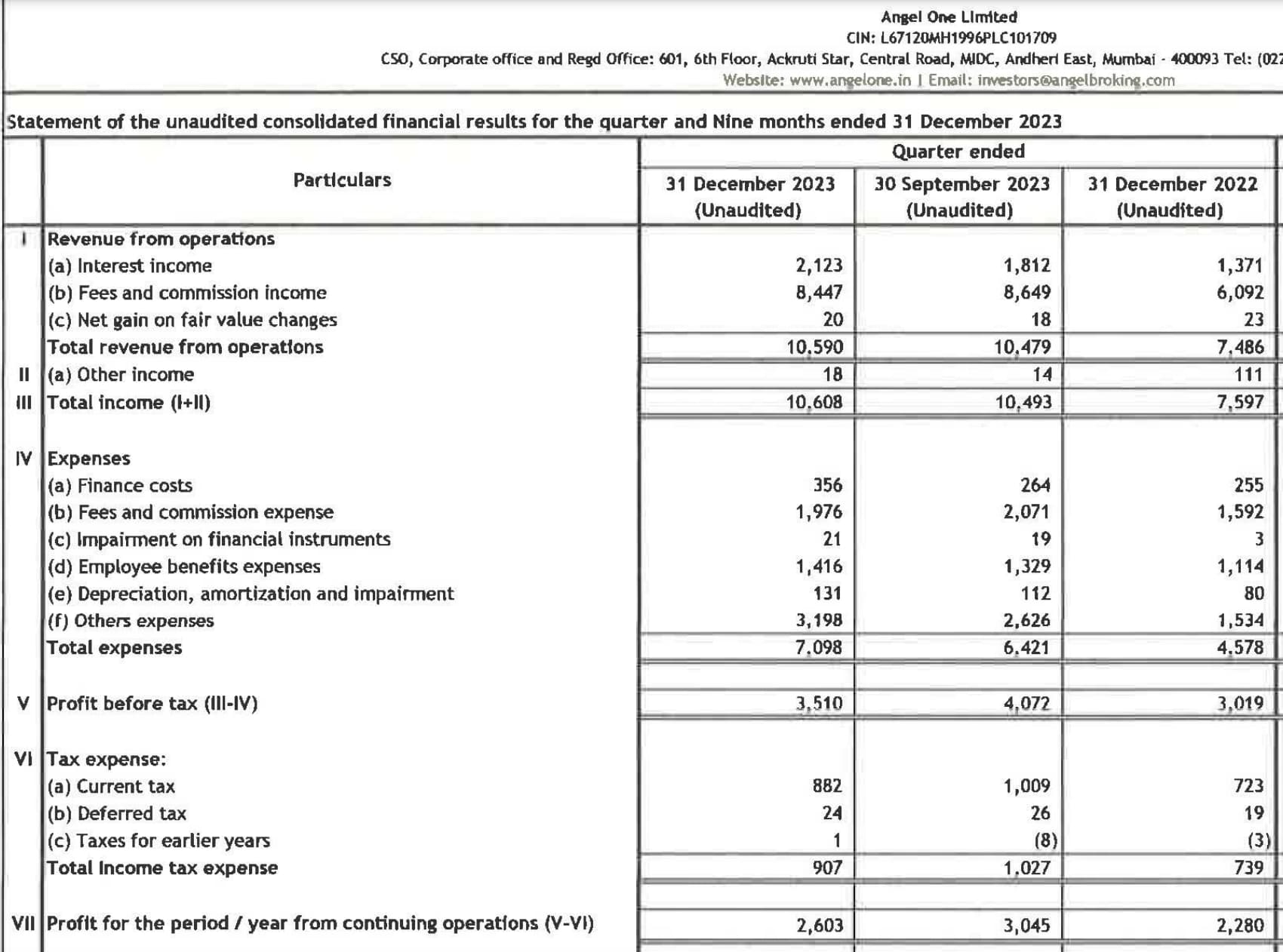

Angelo One Q3 results are released yesterday. There is good revenue growth QOQ and YoY.

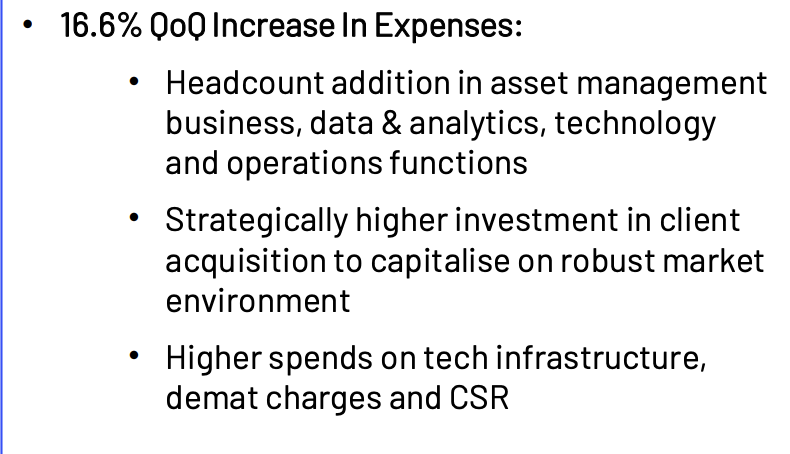

But the PBT is lower QoQ due to other expenses which were higher QoQ by 16%. Look at snapshot below from investor presentations

While this is ignored by some investors as the expenses are related to business growth, not every investor (short, medium and longterm) may look at it the same way. My thoughts below

- While some of these expenses are a one time hit, it is not same for all expenses

- The cost coming from headcount addition would be recurring. It most probably would go up in future as the employee salary and onboarding expenses increases

- Some of tech expenses could be there for few quarters as the co keeps on investing in starting/ setting up adjacent busineses

- Launch and promoting the AMC businesses (and all other businesses) would need front ended costs which the co would spend in next 2 years (just my estimate)

- The AMC business could be loss making for first few quarters until the ramp up happens

- There are better chances for the co to exhibit good revenue growth aided by new businesses. But as these new businesses would be loss making for few quarters, this may negate the profit growth in Broking business

- The co would face some challenges in showing good profits (unless one does SOTP) for upcoming quarters (I’d say 2 years)

The above mentioined points may lead to Time correction (may be price correction as well) in near future.

Disc: Just sharing my thought. Not a recommendation to buy or sell. Please do you own due diligence. Exited in personal PF but holdings in family PF

| Subscribe To Our Free Newsletter |