After Spending Good Time Here’s My Take

Industry Overview

The global flexible packaging market, which accounts for more than 60% of the total packaging market is expected to grow at a CAGR of 4.8% from $ 249 Billion in 2022 to $ 316 Billion in 2027.

Indian BOPP Industry has been growing at almost double of the India’s GDP growth rate over long term

As per a report from Grand View Research, the global speciality chemicals market size was estimated to be $ 616.2 Billion in 2022 and expected to grow to $ 641.5 Billion in 2023. Additionally, the industry is expected to grow at a CAGR of 5.1% to reach $ 914.4 Billion by 20307.

As per KPMG, the Indian speciality chemicals market represents 22% of the country’s chemicals and petrochemicals market with a valuation of $ 32 Billion. With the industry expected to grow at a CAGR of 12% from 2020 – 2025.

The Masterbatch market was estimated to be valued at $ 11.1 Billion in 2020 and projected to grow at a CAGR of 5.1% leading up to 2025 with an estimated valuation of $ 14.3 Billion. Synthetic Paper – Durable alternate to paper. Global market 100kMT (India 6k MT) – immense potential to grow.

The Indian pet care market may be smaller compared to the global market, valued at ₹ 5,100 Crore and it is growing rapidly with a projected annual growth of 25% from 2023 to 2027

Company Profile

Established in 1981, Cosmo Films Ltd.is the pioneer of BOPP Films Industry in India. Promoted by Mr. Ashok Jaipuria, the company is also the largest BOPP film exporter from India.

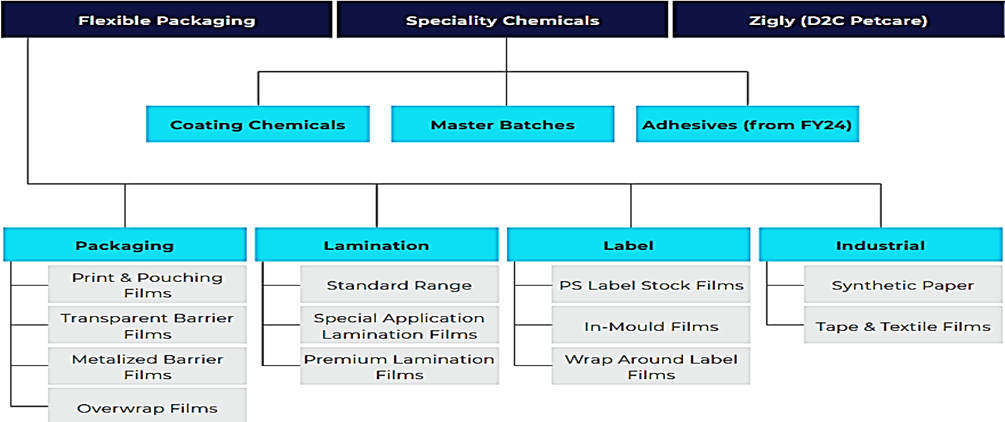

Cosmo Films Limited produces specialty films for use in labelling, lamination, and packaging. The films that it offers are cast polypropylene (CPP), biaxially oriented polypropylene (BOPP), and soon to be available, biaxially oriented polyethylene terephthalate (BOPET).

Cosmo First has expanded its portfolio to include Cosmo Speciality Chemicals having three vertical – master batch, coating chemical and adhesive and Zigly, a pet care brand that offers a full range of services and products for pets.

Company serves to 100+ countries and has 2 R&D labs with most sophisticated equipment and instruments, one in India & another one in USA.

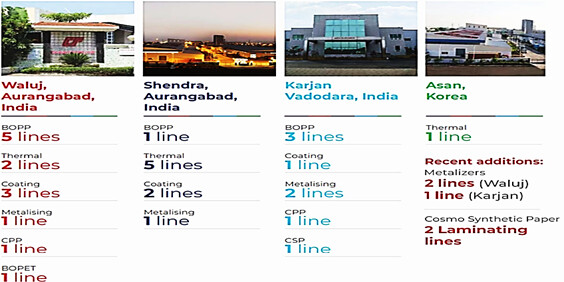

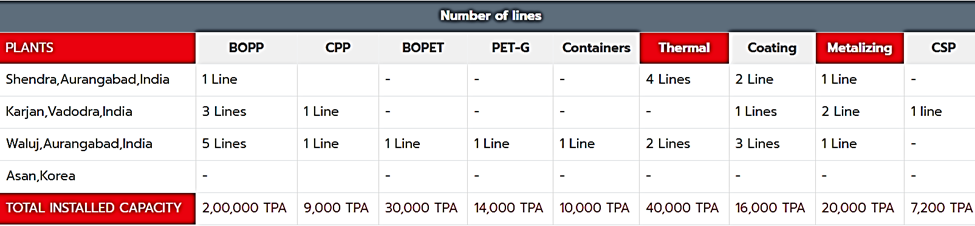

The Company has 4 state of the art manufacturing facilities – out of which 3 are located in India and 1 in Korea. The total installed capacity is as follows:

Why Fall?

-

Supply overhang and margin compressed across the industry leads to correction in the earnings

-

During FY23, the BOPP & BOPET industry faced excess supply due to bunching of several new production lines. Although demand continues to grow, the bunching of supply caused a margin drop and impacted the whole industry.

-

Currently India BOPP production capability is estimated at approx. 850k MT per annum. India domestic BOPP consumption is approx. 650k MT per annum and remaining is broadly exported.

-

Inventory loss

-

Fall in Volume More than Expected

Why We Are Studying?

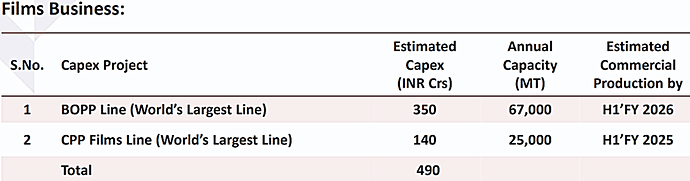

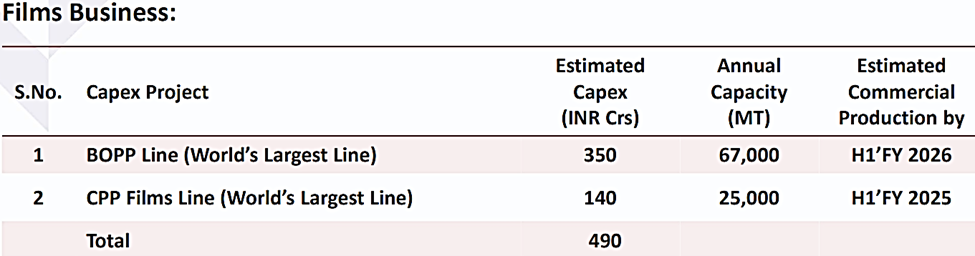

- Taking into account all four assets—BOPP, CPP, metallizer, and a PET sheet line—the company intends to spend about Rs. 490 Cr on CAPEX over the next two years, primarily on BOPP and CPP lines. total amount of all four is the CAPEX that company have committed.

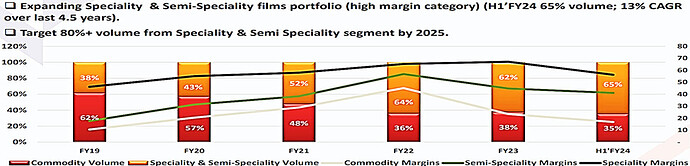

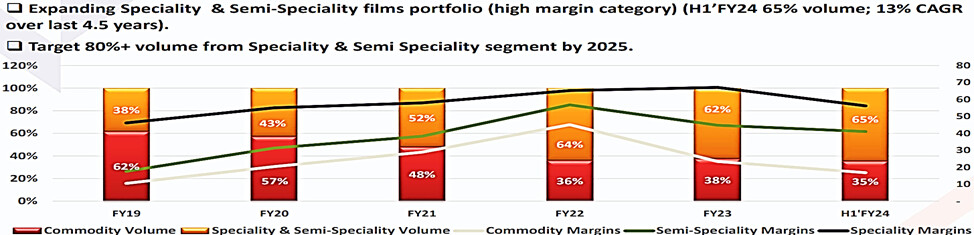

- By the end of the year 2025 the company hopes to Attain 80% of its volume from specialty products (currently at 65%), which will have an incremental impact of 2.5% to 3% to our EBITDA.

- Company with diversified businesses with target 20% CAGR topline growth in next 3 years coupled with commensurate return growth

- The Speciality Chemical subsidiary has got good initial response with its Packaging and Lamination adhesives and shall scale up the same in a phased manner from H2, FY24. Many of these new business initiatives post higher capacity utilization in the next 3-4 quarters will drive growth.

- The company has restructured its operations in South Korea during Q2 of FY24 and is currently moving its extrusion coating plant from South Korea to India in an effort to reduce costs. As a result, INR 3 crores in one-time restructuring expenses had an impact on the consolidated results, which would give the profit in the coming quarters.

Business Model

Cosmo First Ltd. operates a diversified business model across three segments:

Company have B2B Model and Accounts 50% Export of overall Business

Work on Cost Plus Model, Thus does not cost Benefit from lower input Cost that is Volume and Operating Leverage can only help to grow the Company

Product Portfolio

Manufacturing

Revenue Split

Geographically-45% followed by Domestic 55%

Key Clientele

Pepsi, HUL, P&G, ITC & many more

Competitive Strength

- One of the top four players in the world for BOPP specialty films, second-largest player worldwide for thermal lamination films, and specialty label films the largest supplier worldwide in the field of industrial application films.

- when the market is good, company make a bit more money (2% – 3% more) than their competitors from value added products. But when the market is not so good, they can make even more (6% to 7% more) than peers.

- Company serves to 100+ countries 2 R&D labs with most sophisticated equipment and instruments, one in India & another one in USA.

- Capital Allocation History Sound

Future Outlook

-

The BOPP (10th) and CPP (commissioned by 2024) line projects are moving forward according to schedule. By March 2025, both lines will be the largest in the world in terms of production capacity , and they will gradually boost the company’s production capacity by almost 50%.

-

The company has also started metallization of capacitor film recently which shall serve the rapidly growing electronics industry in India with Cosmo’s capacity in Phase 1 shall be 600 mtpa by Q4 of this year & revenue will be close to 40-50 Cr

-

Company’s New Business of rigid Packaging (Initial 40 Cr Investment) will add capacity in Phase 1 shall be 4,800 mtpa which should be able to generate between Rs.70 Cr to Rs.80 Cr of annual sales in nex 12-18 months.

-

Specialized Chemicals (scaling up in coming years) – Estimated INR 50 Cr Capex in next 3 years

-

Company with diversified businesses with target 20% CAGR topline growth in next 3 years coupled with commensurate return growth

-

D2C Pet Care businesses (19 nos. of experience centers as at Sept 2023 – plan to significantly increase to100+ in a couple of years beside online business)

Risk

- The margins, in near to medium term BOPP and BOPET margins are expected to remain subdued, more so for BOPET film due to an industry wide supply overhang .

- BOPET industry is very fragmented, and when prices rise, players often add large capacities, which lowers product realisations. Since raw material costs make up 60–65% of sales, profitability is also susceptible to fluctuations in raw material prices.

- Significantly higher than anticipated capital outflow for unrelated diversifications, abrupt moderation in profitability, delay in ramping up capacity, and additional debt-funded capital expenditures (including any cost overruns) all contribute to a weakening of the financial risk profile.

- Polypropylene which is key raw material for Production of films basically a derivates product and source from RIL, HPCL, OIL etc if any contradiction happens company may suffer

| Subscribe To Our Free Newsletter |