Nice write up. The few points from my side:

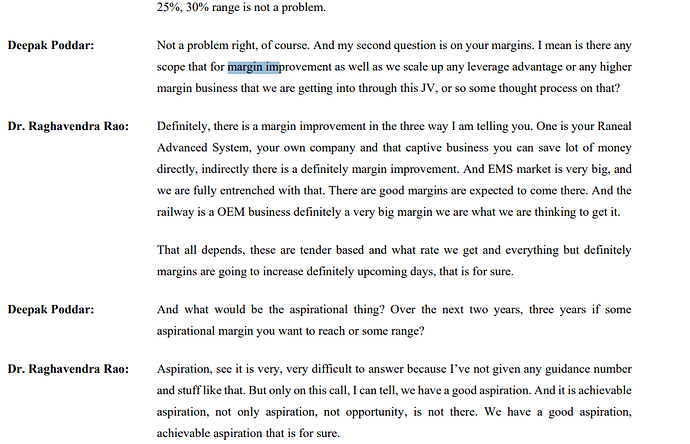

- Still OPM is between 6-7 % due to EMS nature of business. It appears a volume play as of now. In Last Con-Call there was discussion on margin expansion-

Company hopes that once backward integration happens ( Manufacturing PCB by Subsidiary Renal Advanced System) there would be improvement in margin. But, company is not quantifying it.

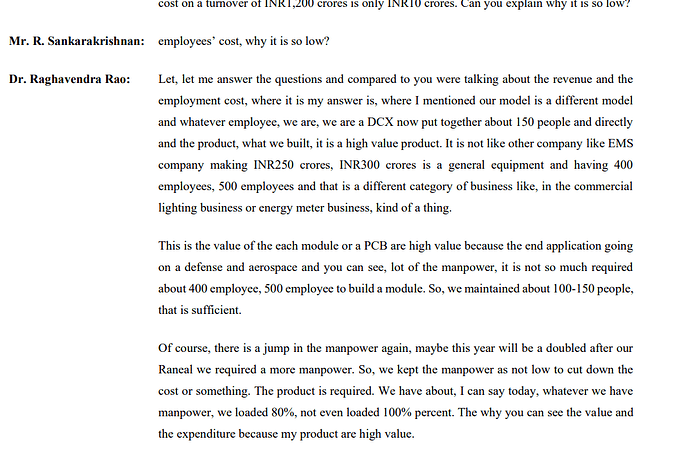

- Employee cost is very low. Approx. 1% of Sales. In May 29, 2023 Con call the issue was raised by investor as below:

As per management company uses hig value products, so employee requirement is low. But, after going through different con-calls it appears that they are not in highly technical field. They are basically in integration and in assemly and now they have started making high value PCBs which they were integrating.

- There is shrinkage in order book of the company. After Q4 Fy 23 it was Rs 1700 Cr. After Q2 FY 24 it is Rs1260 Cr. Although management is quite confident and some they are expecting orders in some more programs.

Over all it appears a decent play and value migration may also happen, as company delivers result, enters in JVs and acquire technologies.

Disclosure: Not invested

Disclaimer : I may be wrong in my analysis, I am neitehr SEBI registered analyst nor subject expert. Please do your own due dliligence.

| Subscribe To Our Free Newsletter |