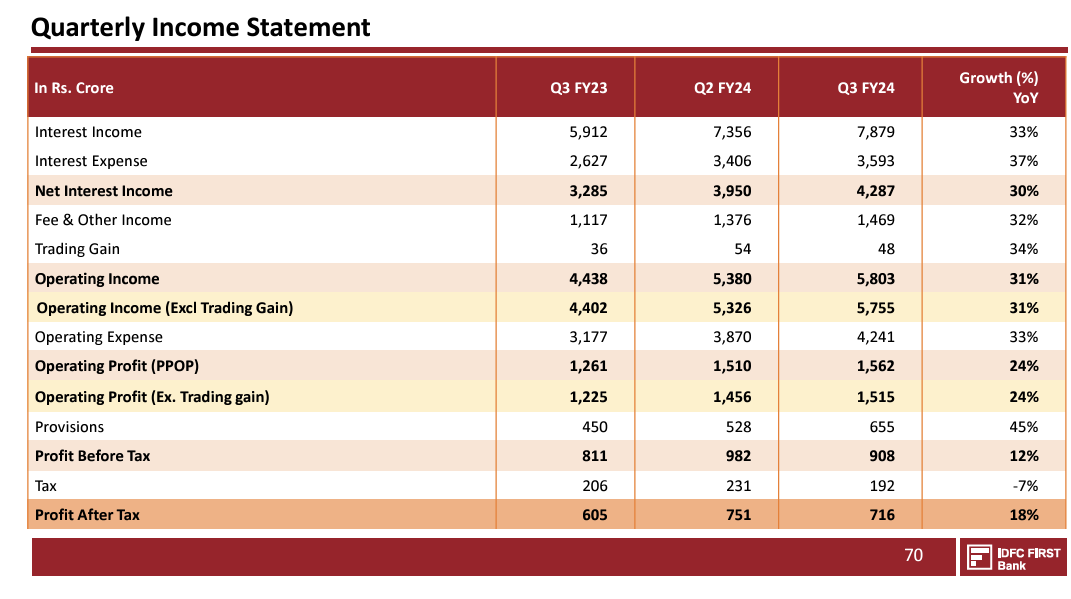

Bank’s NII has grown at 30% YoY, PPOP has grown at 24%.

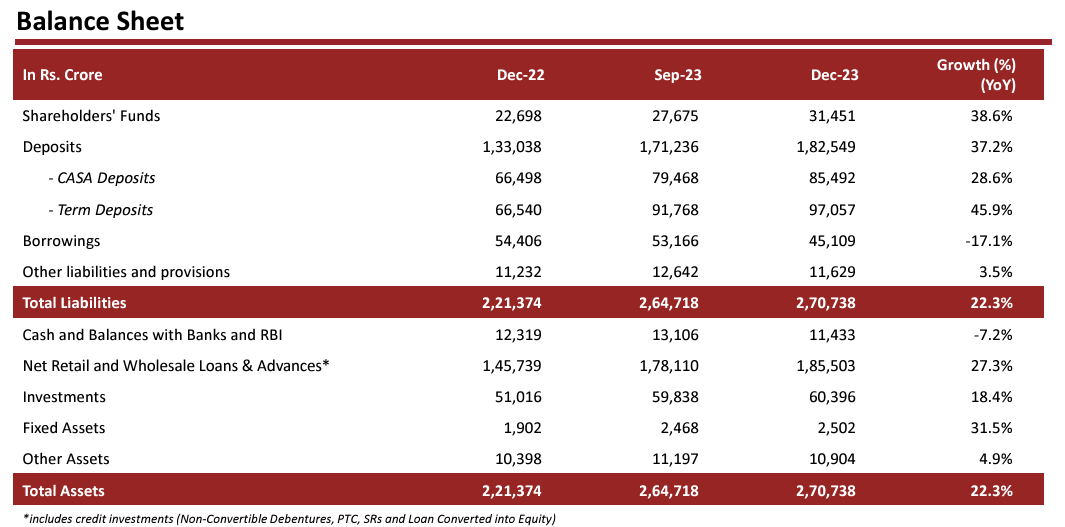

Deposits have grown at 37.2%.

I don’t find any other major bank which has given such an operational performance in this quarter. The only issue with this result is high provisions (which mgmt has explained as Aging related matric) and high Cost to Income ratio (not a new issue).

While the bank has changed quiet a lot, many shareholders want mgmt to show improvement every quarter. I don’t think that works in any company. Bank has already moved from sub 5% RoE to 10%+ RoE. The management has now guided for 17-18% RoE in next 5 years. As a shareholder, this is already very aggressive guidance.

If they even achieve 15% RoE while doubling the Asset book, we are talking about a bank with Book value of 60K+ crores in next 4-5 years. Currently, the bank itself is worth 62K crores. If bank even gets a PB ratio of 2.5 by 2029 (how much will you give to a bank growing at 20% with 15% RoE), we are talking about 2.5x return in 5 years. It means 20%+ returns over next 5 years.

I am surprised that even though bank has shown no operational issues, still people are writing obituaries for the bank as if management is found to be involved in some fraud.

A weak quarter only leads to weak hands giving stocks to strong hands. In investing, only strong hands make profit. If the share falls 5-10% in next few weeks, I would suggest that it’s the best time to add.

| Subscribe To Our Free Newsletter |